Target 2003 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2003 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

|

|

30

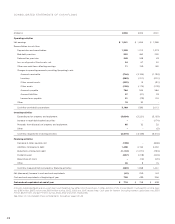

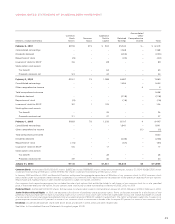

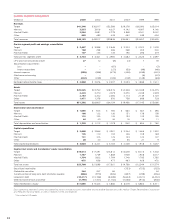

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Summary of Accounting Policies

Organization Target Corporation (the Corporation) is a general

merchandise retailer, comprised of three operating segments:

Target, Mervyn’s and Marshall Field’s. Our segments are primarily

determined by the nature of the products and services offered to

our guests. Target, an upscale discount chain located in 47 states,

contributed 86 percent of our 2003 total revenues. Mervyn’s, a

middle-market promotional department store located in 14 states

in the West, South and Midwest, contributed 7 percent of total

revenues. Marshall Field’s (including stores formerly named

Dayton’s and Hudson’s), a traditional department store located in

8 states in the upper Midwest, contributed 5 percent of total

revenues. Management measures segment performance based on

pre-tax segment profit, which includes credit card operations.

Credit card operations drive revenue growth at each segment and

are considered an integral component of our retail operations.

Business segment comparisons are presented on page 38.

Consolidation The financial statements include the balances of

the Corporation and its subsidiaries after elimination of material

intercompany balances and transactions. All material subsidiaries

are wholly owned.

Use of Estimates The preparation of our financial statements, in

conformity with accounting principles generally accepted in the

United States (GAAP), requires management to make estimates

and assumptions that affect the reported amounts in the financial

statements and accompanying notes. Actual results may differ

from those estimates.

Fiscal Year Our fiscal year ends on the Saturday nearest January 31.

Unless otherwise stated, references to years in this report relate

to fiscal years rather than to calendar years. Fiscal years 2003,

2002 and 2001 each consisted of 52 weeks.

Reclassifications Certain prior year amounts have been reclassified

to conform to the current year presentation.

Stock-based Compensation In 2003, we adopted Statement of

Financial Accounting Standards (SFAS) No. 123, “Accounting for

Stock-Based Compensation,” in accordance with the prospective

transition method prescribed in SFAS No. 148, “Accounting for

Stock-Based Compensation—Transition and Disclosure” and began

recognizing compensation expense for stock options granted

during the year. Compensation expense is reflected in selling,

general and administrative expenses. Prior to 2003, we accounted

for stock option awards under the intrinsic value method prescribed

in Accounting Principles Board (APB) No. 25, “Accounting for

Stock Issued to Employees” which resulted in no compensation

expense because the exercise price of the stock options was equal

to the fair market value of the underlying stock on the grant date.

The pro forma impact of accounting for those awards at fair value

is disclosed on page 35.

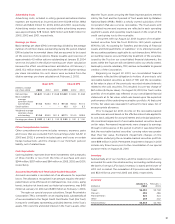

Revenues

Revenue from retail sales is recognized at the time of sale. Com-

missions earned on sales generated by leased departments are

included within sales and were $38 million in 2003, $33 million in

2002 and $37 million in 2001. Net credit card revenues are comprised

of finance charges and late fees from credit card holders, as well as

third-party merchant fees earned from the use of our Target Visa

credit card. Net credit card revenues are recognized according to the

contractual provisions of each applicable credit card agreement.

If an account is written-off, any uncollected finance charges or late

fees are recorded as a reduction of credit card revenue. The amount

of our retail sales charged to our credit cards was $5.3 billion,

$5.4 billion and $5.6 billion in 2003, 2002 and 2001, respectively. Prior

to August 22, 2001, net credit card revenues are net of the payments

made to holders of publicly held receivable-backed securities.

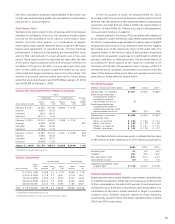

Consideration Received from Vendors

We collect vendor income primarily as a result of our promotional,

advertising and compliance programs. Promotional and advertising

allowances are intended to offset our costs of promoting and selling

the vendor’s merchandise in our stores and are recognized when we

incur the cost or complete the promotion. Under our compliance

programs, vendors are charged for merchandise shipments that do

not meet our requirements, such as late or incomplete shipments,

and we record these allowances when the violation occurs. Vendor

income either reduces our inventory costs or our operating expenses

based on the requirements of Emerging Issues Task Force (EITF)

Issue No. 02-16, “Accounting by a Customer (Including a Reseller) for

Certain Consideration Received from a Vendor” as discussed below.

In the first quarter of 2003, we adopted EITF No. 02-16. In

accordance with EITF No. 02-16, certain vendor income items have

been reclassified from operating expenses to inventory purchases

and recognized into income as the vendors’ merchandise is sold.

The guidance was applied on a prospective basis only as required

by EITF No. 02-16. This reclassification had no material impact on

sales, cash flows or financial position for any period, and had a

slight negative impact on net earnings.

In the fourth quarter of 2003, we adopted EITF No. 03-10,

“Application of Issue 02-16 by Resellers to Sales Incentives Offered

to Consumers by Manufacturers,” which amends EITF No. 02-16.

The adoption of EITF No. 03-10 did not have a material impact on

net earnings, cash flows or financial position. The requirements of

EITF No. 02-16 and EITF No. 03-10 are discussed in Management’s

Discussion and Analysis on pages 24-25.

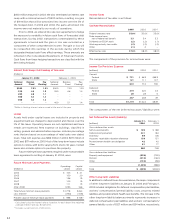

Buying and Occupancy Expenses

Buying expenses primarily consist of salaries and expenses incurred

by the Corporation’s merchandising operations, while our occupancy

expenses primarily consist of rent, depreciation, property taxes

and other operating costs of our retail and distribution facilities.

Buying and occupancy expenses classified in selling, general and

administrative expenses were $1.5 billion, $1.4 billion and $1.2 billion

in 2003, 2002 and 2001, respectively. In addition, we recorded

$1 billion, $934 million and $814 million of depreciation expense

for our retail and distribution facilities in 2003, 2002 and 2001,

respectively.