Target 2003 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2003 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

21

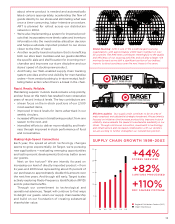

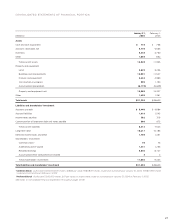

Fourth Quarter Pre-tax Segment Profit

and Percent Change from Prior Year

(millions) 2003 2002 2001

Target $1,380 18.5% $1,165 8.0% $1,078 20.9%

Mervyn’s 74 (0.3) 75 (42.9) 131 20.8

Marshall Field’s 59 15.6 51 (18.9) 63 (20.2)

Total $1,513 17.3% $1,291 1.4% $1,272 17.9%

LIFO provision 27 12 (8)

Interest expense (130) (154) (135)

Other (72) (36) (68)

Earnings

before taxes $1,338 $1,113 $1,061

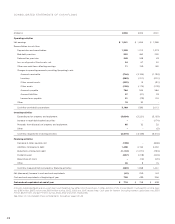

Critical Accounting Estimates

Our analysis of operations and financial condition are based upon

our consolidated financial statements, which have been prepared in

accordance with GAAP. The preparation of these financial statements

requires us to make estimates and assumptions that affect the

reported amounts of assets and liabilities at the date of the financial

statements, the reported amounts of revenues and expenses during

the reporting period and the related disclosures of contingent assets

and liabilities. In the Notes to Consolidated Financial Statements, we

describe our significant accounting policies used in the preparation

of the consolidated financial statements. We evaluate our estimates

on an ongoing basis. We base our estimates on historical experience

and on various other assumptions that we believe to be reasonable

under the circumstances. Actual results could differ from these

estimates under different assumptions or conditions.

The following items in our consolidated financial statements

require significant estimation or judgment:

Inventory and cost of sales We account for substantially all of our

inventory and the related cost of sales under the retail inventory

method using the LIFO basis. Under the retail inventory method,

inventory is stated at cost, which is determined by applying a cost-

to-retail ratio to each similar merchandise grouping’s ending retail

value. Since this inventory value is adjusted regularly to reflect

market conditions, our inventory methodology reflects the lower

of cost or market. We also reduce inventory for estimated losses

related to shortage, based upon historical losses verified by prior

physical inventory counts. Inventory also includes a LIFO provision

that is calculated based on inventory levels, markup rates and

internally generated retail price indices. Inventory is at risk of

obsolescence if economic conditions change, such as shifting

consumer demand, changing consumer credit markets, or increased

competition, even though substantially all of our inventory sells

in less than six months. Our vendor income and inventory are

described in the Notes to Consolidated Financial Statements on

pages 30 and 31, respectively.

Allowance for doubtful accounts When receivables are recorded,

an allowance for doubtful accounts in an amount equal to anticipated

future write-offs is recognized. The allowance includes provisions

for uncollectible finance charges and other credit fees. We estimate

future write-offs based on delinquencies, risk scores, aging trends,

industry risk trends and our historical experience. The allowance

for doubtful accounts was $419 million or 6.8 percent of year-end

receivables at January 31, 2004, compared to $399 million or

6.7 percent of year-end receivables at February 1, 2003. Management

believes that the allowance for doubtful accounts is adequate to

cover anticipated losses in our credit card accounts receivable under

current conditions; however, significant deterioration in any of the

factors mentioned above or in general economic conditions could

materially change these expectations. Our accounts receivable

and related allowance are described in the Notes to Consolidated

Financial Statements on page 31.

Pension and postretirement health care accounting We fund and

maintain three qualified defined benefit pension plans and maintain

certain related non-qualified plans as well. Our pension costs are

determined based on actuarial calculations using key assumptions

including our expected long-term rate of return on qualified plan

assets, discount rate and our estimate of future compensation

increases. We also maintain a postretirement health care plan for

certain retired employees. Postretirement health care costs are

calculated based on actuarial calculations using key assumptions

including a discount rate and health care cost trend rates. Our pension

and postretirement health care benefits are further described in

the Notes to Consolidated Financial Statements on pages 36-37.

Insurance/self-insurance We retain a portion of the risk related

to certain general liability, workers’ compensation, property loss

and employee medical and dental claims. Liabilities associated

with these losses are calculated for claims filed, and claims

incurred but not yet reported, at our estimate of their ultimate

cost, based upon analysis of historical data and actuarial estimates.

General liability and workers’ compensation liabilities are recorded

at our estimate of their net present value; other liabilities are not

discounted. Our expected loss accruals are based on estimates,

and while we believe the amounts accrued are adequate, the

ultimate loss may differ from the amounts provided. We maintain

stop-loss coverage to limit the exposure related to certain risks.

Income taxes We pay income taxes based on the tax statutes,

regulations and case law of the various jurisdictions in which we

operate. Our effective income tax rate was 37.8 percent, 38.2 percent

and 38.0 percent in 2003, 2002 and 2001, respectively. The income

tax provision includes estimates for certain unresolved matters in

dispute with state and federal tax authorities. Management

believes the resolution of such disputes will not have a material

impact on our financial statements. Our effective income tax rate

in 2004 is expected to be approximately 37.8 percent. Our income

taxes are further described in the Notes to Consolidated Financial

Statements on page 34.