Target 2003 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2003 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

24

Performance Objectives

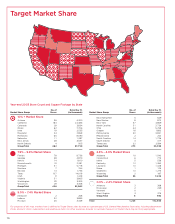

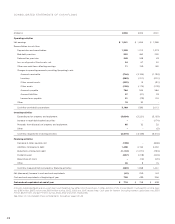

Shareholder Return

Our primary objective is to maximize

shareholder value over time through

a combination of share price appreci-

ation and dividend income while

maintaining a prudent and flexible

capital structure. Our total annualized

return to shareholders (including

reinvested dividends) over the last five

years averaged 4.2 percent, returning

about $123 for each $100 invested in

our stock at the beginning of this

period. The peer group we refer to in

the adjacent graph represents those

companies included in the S&P 500

Retailing and S&P 500 Food and Drug

Retailing Indices, and is the group we

refer to in our proxy statement.

Measuring Value Creation

We measure value creation internally using a form of Economic

Value Added (EVA), which we define as after-tax segment profit

less a capital charge for all investment employed. The capital

charge is an estimate of our after-tax cost of capital adjusted for

the age of our stores, recognizing that mature stores inherently

have higher returns than newly opened stores. We use a benchmark

of 9 percent for the estimated after-tax cost of capital invested in

our retail operations and a benchmark of 5 percent for capital

invested in our credit card operations, as a result of its ability to

support higher debt levels. We expect to continue to generate

returns in excess of these benchmarks, thereby producing EVA.

EVA is used to evaluate our performance and to guide capital

investment decisions. A significant portion of executive incentive

compensation is tied to the achievement of targeted levels of

annual EVA generation. We believe that managing our business

with a focus on EVA helps achieve our objective of average annual

earnings per share growth of 15 percent or more over time. Earnings

per share has grown at a compound annual rate of 15 percent over

the last five years.

New Accounting Pronouncements

2004 Adoptions

In January 2003, the Financial Accounting Standards Board issued

Interpretation No. 46, “Consolidation of Variable Interest Entities, an

interpretation of Accounting Research Bulletin No. 51” (FIN No. 46).

FIN No. 46 will be effective no later than the end of the first

reporting period that ends after March 15, 2004. FIN No. 46 requires

the consolidation of entities in which an enterprise absorbs a

majority of the entity’s expected losses, receives a majority of the

entity’s expected residual returns, or both, as a result of ownership,

contractual or other financial interest in the entity. Currently, entities

are generally consolidated by an enterprise when it has a controlling

financial interest through ownership of a majority voting interest in

the entity. We do not expect the adoption of FIN No. 46 to have a

material impact on our net earnings, cash flows or financial position.

2003 Adoptions

In the first quarter of 2003, we adopted EITF No. 02-16, “Accounting

by a Customer (Including a Reseller) for Certain Consideration

Received from a Vendor.” Under the new guidance, cash consider-

ation received from a vendor is presumed to be a reduction of the

prices of the vendor’s products or services and should be classified

as a reduction in cost of sales. If the cash consideration is for assets

or services delivered to the vendor, it should be characterized as

revenue. If the cash consideration is a reimbursement of costs

incurred to sell the vendor’s products, it should be characterized

as a reduction of that cost. This guidance had no material impact

on sales, cash flows or financial position for any period, and had

a slight negative impact on net earnings. Our accounting policy

regarding vendor income is discussed in the Notes to Consolidated

Financial Statements on page 30.

In the first quarter of 2003, we adopted SFAS No. 123,

“Accounting for Stock-Based Compensation,” in accordance with

the prospective transition method prescribed in SFAS No. 148,

“Accounting for Stock-Based Compensation — Transition and

Disclosure.” The fair value based method has been applied

prospectively to awards granted subsequent to February 1, 2003

(the last day of our 2002 fiscal year). The adoption of this method

increased compensation expense by less than $.01 per share in

2003. Our accounting policy regarding stock-based compensation

is discussed in the Notes to Consolidated Financial Statements

on page 30.

In the first quarter of 2003, we adopted SFAS No. 143,

“Accounting for Asset Retirement Obligations.” The adoption did

not have an impact on current year or previously reported net

earnings, cash flows or financial position.

In the first quarter of 2003, we adopted SFAS No. 146,

“Accounting for Costs Associated with Exit or Disposal Activities.”

SFAS No. 146 requires that a liability for a cost associated with an

exit or disposal activity be recognized when the liability is incurred

5 Year 10 Year

4%

–1%

2%

23%

11%

25

15

20

10

5

0

13%

Total Annualized

Return

Target

S&P 500

Peer group