Target 2003 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2003 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

19

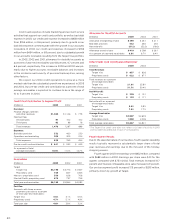

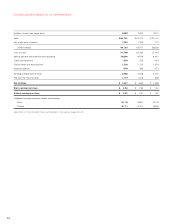

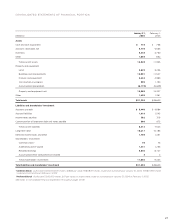

Pre-tax Segment Profit and as a Percent of Revenues

Pre-tax Segment Profit As a Percent of Revenues

(millions) 2003 2002 2001 2003 2002 2001

Target $3,467 $3,088 $2,546 8.4% 8.4% 7.8%

Mervyn’s 160 238 286 4.5 6.2 7.1

Marshall Field’s 107 135 133 4.1 5.0 4.8

Total pre-tax

segment

profit $3,734 $3,461 $2,965 7.9% 8.0% 7.5%

Securitization

adjustments:

Loss –– (67)

Interest

equivalent –– (27)

LIFO provision

credit/(expense) 27 12 (8)

Interest expense (559) (588) (473)

Other (242) (209) (183)

Earnings

before taxes $2,960 $2,676 $2,207

In 2001, the $67 million pre-tax loss related to the required adoption of a

new accounting standard applicable to securitized accounts receivable. The

$27 million interest equivalent represented payments accrued to holders of

sold securitized receivables prior to August 22, 2001 (discussed in detail in

the Notes to Consolidated Financial Statements under Accounts Receivable

and Receivable-backed Securities on page 31).

Interest Expense

In 2003, interest expense was $559 million, $29 million lower than

in 2002. The decrease was due to a lower average portfolio interest

rate and a smaller loss on debt called or repurchased, partially

offset by higher average debt outstanding. The average portfolio

interest rate in 2003 was 4.9 percent compared with 5.6 percent

in 2002. The $297 million of debt called or repurchased during

2003 resulted in a loss of $15 million (approximately $.01 per share)

and had an average interest rate of 7.8 percent and an average

remaining life of 20 years.

In 2002, interest expense was $588 million, $88 million higher

than the total of interest expense and interest equivalent in 2001.

The increase was due to higher average debt outstanding and a

greater loss on the early call or repurchase of debt, partially offset

by a lower average portfolio interest rate. The average portfolio

interest rate in 2002 was 5.6 percent compared with 6.4 percent

in 2001. (For analytical purposes, the amounts that represented

payments accrued to holders of sold securitized receivables prior

to August 22, 2001 were considered interest equivalent as discussed

in the Notes to Consolidated Financial Statements on page 31.

After that date, such payments constituted interest expense.) In

2002 and 2001, we incurred losses of $34 million ($.02 per share)

and $9 million (less than $.01 per share) from the early call or

repurchase of $266 million and $144 million of debt, respectively.

The debt called or repurchased had an average interest rate of

8.8 percent and 9.2 percent, respectively, and had an average

remaining life of 19 years and 7 years, respectively.

We adopted SFAS No. 145, “Rescission of FASB Statements

No. 4, 44 and 64, Amendment of FASB Statement No. 13 and

Technical Corrections” in the first quarter of 2002. Under SFAS

No. 145, gains and losses from the early extinguishment of debt are

required to be included in interest expense and are not reflected

as an extraordinary item. Prior year extraordinary items have been

reclassified to reflect this change. The adoption of SFAS No. 145

had no impact on net earnings, cash flows or financial position.

The requirements of SFAS No. 145 are discussed under New

Accounting Pronouncements on page 25.

Excluding the effect of any early call or repurchase of debt,

we expect interest expense in 2004 to remain essentially flat to

2003, as average debt outstanding and the average portfolio

interest rate are not expected to change significantly.

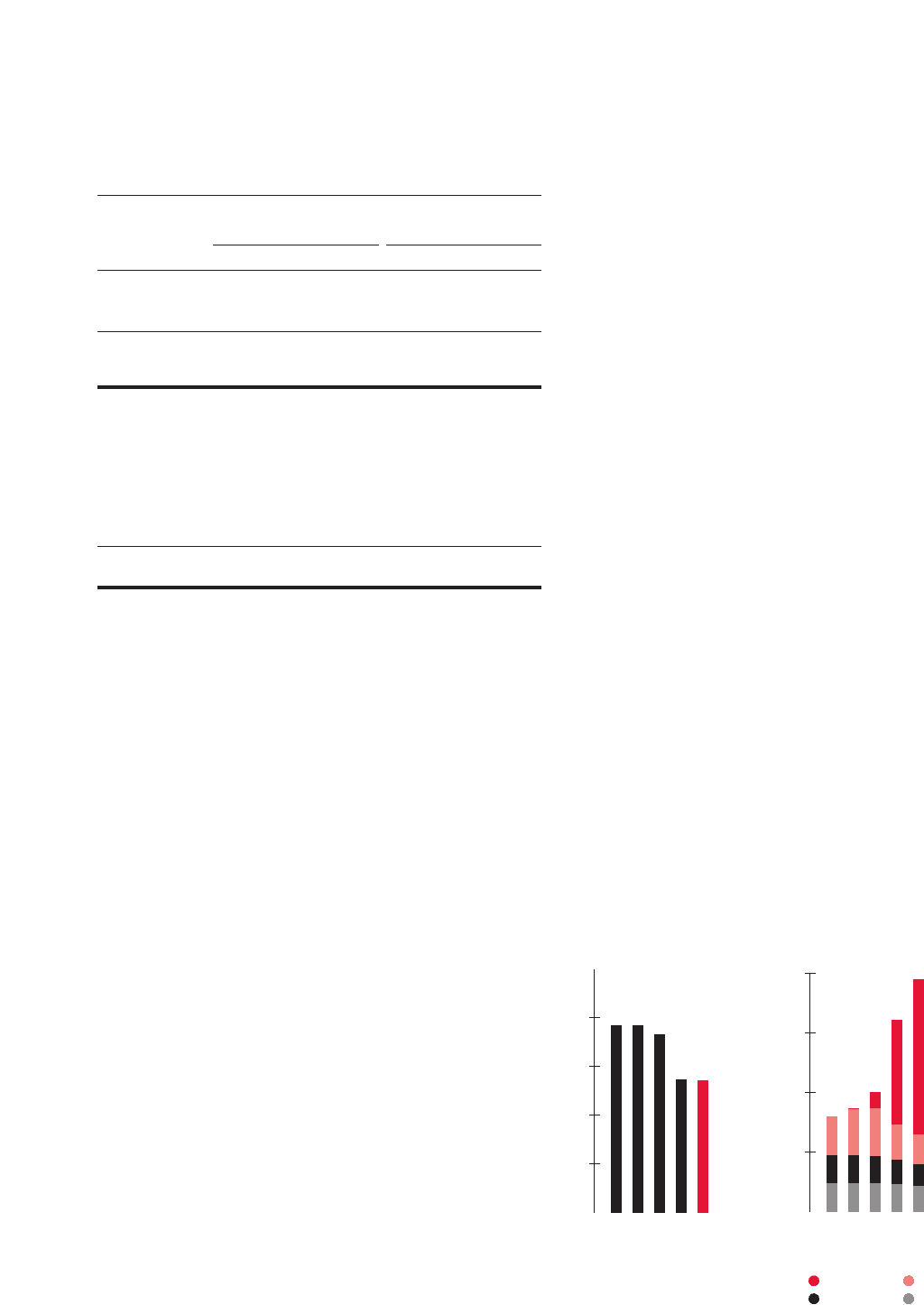

Credit Card Operations

Through our proprietary store-brand credit card programs, some

of which have been available for decades, and our Target Visa credit

card that was introduced nationally in 2001, we offer credit to

qualified guests in each of our business segments. Our credit card

programs strategically support our core retail operations and are

an integral component of each business segment. Our credit card

products support earnings growth by driving sales at our stores

and through improvements in our credit card financial performance.

Our credit card revenues are primarily derived from finance

charges, late fees and other revenues. Intracompany merchant fees

are fees charged to our retail operations on a basis similar to fees

charged by third-party credit card issuers. These fees are eliminated

in consolidation. Third-party merchant fees are paid to us by

merchants that have accepted the Target Visa credit card. In 2003,

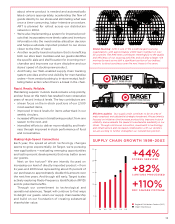

our credit card revenues increased to $1,479 million from $1,297

million, or 14 percent, due to continued growth in the Target Visa

credit card portfolio. In 2002, our credit card revenues increased

to $1,297 million from $899 million, or 44 percent, due primarily to

additional revenues earned from the Target Visa credit card portfolio.

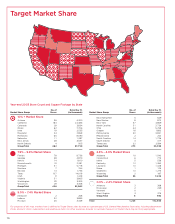

’99 ’00 ’01 ’02 ’03

15.4%

15.4%

14.7%

11.0%

10.9%

16

8

12

4

Credit Portfolio

Yield

’99 ’00 ’01 ’02 ’03

$4,500

$6,000

$3,000

$1,500

Average Receivables

(millions)

Target Visa Target Guest Card

Mervyn’s Marshall Field’s