Target 2003 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2003 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

|

|

32

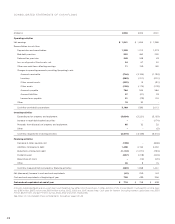

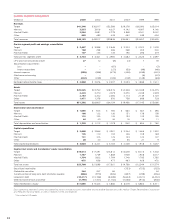

Property and Equipment

Property and equipment are recorded at cost, less accumulated

depreciation. Depreciation is computed using the straight-line

method over estimated useful lives. Depreciation expense for the

years 2003, 2002 and 2001 was $1,286 million, $1,183 million and

$1,049 million, respectively. Accelerated depreciation methods are

generally used for income tax purposes. Repair and maintenance

costs were $453 million, $416 million and $386 million in 2003,

2002 and 2001, respectively.

Estimated useful lives by major asset category are as follows:

Asset Life (in years)

Buildings and improvements 8 – 39

Fixtures and equipment 4 – 15

Computer hardware and software 4

We adopted SFAS No. 144, “Accounting for the Impairment

or Disposal of Long-Lived Assets” in the first quarter of 2002. In

accordance with this guidance, all long-lived assets are reviewed

when events or changes in circumstances indicate that the carrying

value of the asset may not be recoverable. The requirements of

SFAS No. 144 are discussed in Management’s Discussion and

Analysis on page 25.

We review most assets at the store level, which is the lowest

level of assets for which there are identifiable cash flows. The

carrying amount of the store assets is compared to the expected

undiscounted future cash flows to be generated by those assets

over the estimated remaining useful life of the primary asset. Cash

flows are projected for each store based upon historical results and

expectations. In cases where the expected future cash flows and

fair value are less than the carrying amount of the assets, those

stores are considered impaired and the assets are written down

to fair value. Fair value is based on appraisals or other reasonable

methods to estimate fair value. Impairment losses are included in

depreciation expense for held and used assets and included within

selling, general and administrative expense on assets classified

as held for sale. Our fixed asset impairment tests, performed in

accordance with the applicable accounting guidance, assumed each

of our segments would continue indefinitely. Changes in these

assumptions could impact the results of our analysis. In both 2003

and 2002, impairment losses resulted in a financial statement

impact of less than $.01 per share.

Goodwill and Intangible Assets

Goodwill and intangible assets are recorded within other long-term

assets at cost less accumulated amortization. Amortization is

computed on intangible assets with definite useful lives using the

straight-line method over estimated useful lives that range from

three to fifteen years. Amortization expense for the years 2003,

2002 and 2001 was $34 million, $29 million and $30 million,

respectively. At January 31, 2004 and February 1, 2003, net good-

will and intangible assets were $364 million and $376 million,

respectively. These assets included $155 million of goodwill and

intangible assets with indefinite useful lives in both years, principally

associated with Marshall Field’s and target.direct.

As required, we adopted SFAS No. 142, “Goodwill and Other

Intangible Assets,” during the first quarter of 2002. In 2003 and

2002, the adoption of this statement reduced annual amortization

expense by approximately $10 million (less than $.01 per share).

The requirements of SFAS No. 142 are discussed in Management’s

Discussion and Analysis on page 25.

Discounted cash flow models were used in determining fair

value for the purposes of the required annual goodwill impairment

analysis. Management used other market data to validate the

results of our analysis. No impairments were recorded in 2003,

2002 and 2001 as a result of the tests performed.

Other Long-term Assets

In addition to goodwill and intangible assets discussed above, the

major components of other long-term assets at January 31, 2004

included pre-funded pension benefits, investments, deferred

financing costs and derivatives. The increase in the long-term asset

balance is primarily due to pre-funded pension contributions of

$200 million partially offset by a $43 million reduction in the value

of derivative assets that were outstanding at year-end. Our pension

plan contributions are disclosed on page 36 and our derivative

transactions are discussed on pages 33-34.

Accounts Payable

Our accounting policy is to reduce accounts payable when checks

to vendors clear the bank from which they were drawn. Out-

standing checks included in accounts payable were $1,325 million

and $1,125 million at year-end 2003 and 2002, respectively.

Lines of Credit

At January 31, 2004, two committed credit agreements totaling

$1.6 billion were in place through a group of 26 banks at specified

rates. There were no balances outstanding at any time during 2003

or 2002 under these agreements.

Commitments and Contingencies

At January 31, 2004, our obligations included notes payable, notes

and debentures of $10,925 million (discussed in detail under Long-

term Debt and Notes Payable on page 33) and the present value

of capital and operating lease obligations of $158 million and $998

million, respectively (discussed in detail under Leases on page 34).

In addition, commitments for the purchase, construction, lease or

remodeling of real estate, facilities and equipment were approxi-

mately $545 million at year-end 2003. Royalty commitments of

approximately $80 million are due during the three-year period

ending in 2007. Throughout the year, we enter into various com-

mitments to purchase inventory. In addition to the accounts payable

reflected in our Statements of Financial Position on page 27, we had

commitments with various vendors for the purchase of inventory

as of January 31, 2004. These purchase commitments are cancelable

by their terms.