Target 2003 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2003 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

18

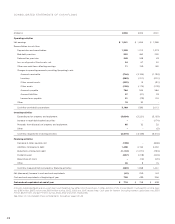

In 2003, our consolidated gross margin rate increased

0.5 percent to a rate of 32.0 percent primarily due to the adoption

of Emerging Issues Task Force (EITF) Issue No. 02-16 “Accounting

by a Customer (Including a Reseller) for Certain Consideration

Received from a Vendor.” The adoption resulted in a reclassification

of a portion of our vendor income from selling, general and

administrative expenses to cost of sales and had a slight negative

impact on net earnings as described in the Notes to Consolidated

Financial Statements on page 30.

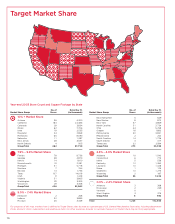

At Target, gross margin rate improved due to the vendor

income reclassification. Mervyn’s gross margin rate improvement

was primarily a result of the vendor income reclassification and

efforts to lower purchase costs through improved negotiating

programs that resulted in markup improvement, partially offset by

an increase in markdowns. Marshall Field’s gross margin rate

increased due to the vendor income reclassification and reductions

in purchase costs which resulted in markup improvement. These

improvements were partially offset by an increase in markdowns.

In 2002, our consolidated gross margin rate expanded by

almost a full percentage point to a rate of 31.5 percent from

30.6 percent. The growth is attributable to rate expansion at Target

and Mervyn’s, primarily due to reductions in purchase costs and

improvements in markup during the year. These increases were

partially offset by additional markdowns at Mervyn’s and Marshall

Field’s and the mix impact of growth at Target, our lowest gross

margin rate division.

Consolidated gross margin rate in 2004 is expected to be

approximately equal to 2003. Gross margin rate at Target is

expected to remain essentially even with that of 2003. We expect

modest gross margin rate expansion at both Mervyn’s and Marshall

Field’s to be offset by the mix impact of faster growth at Target,

our lowest gross margin rate division.

Selling, General and Administrative Expense Rate

Our selling, general and administrative (SG&A) expense rate

represents payroll, benefits, advertising, distribution, buying and

occupancy, start-up and other expenses as a percentage of sales.

SG&A expense excludes depreciation and amortization and expenses

associated with our credit card operations, which are reflected

separately in our Consolidated Results of Operations. In 2003,

approximately $78 million of vendor income was recorded as an

offset to SG&A expenses as it met the specific, incremental and

identifiable criteria of EITF No. 02-16. Approximately $294 million

and $272 million of vendor income was recorded as an offset to

SG&A expenses in 2002 and 2001, respectively. This vendor income

primarily represented advertising reimbursements.

In 2003, our SG&A expense rate increased to 22.9 percent

compared to 22.0 percent in 2002. Over half of this increase is

attributable to the reclassification of vendor income to cost of sales

from SG&A expenses as described in the Notes to Consolidated

Financial Statements on page 30. The remaining increase is

principally due to a lack of sales leverage at both Mervyn’s and

Marshall Field’s.

In 2002, our SG&A expense rate rose to 22.0 percent compared

to 21.6 percent in 2001 because certain items such as medical

expenses increased at a faster pace than sales. This effect was only

partially offset by the mix impact of growth at Target, our lowest

SG&A expense rate division.

In 2004, we expect our SG&A expense rate to increase

slightly from 2003, reflecting our belief that a number of expenses

will increase at a faster pace than sales. These include expenses

related to our defined benefit plans, insurance and stock options,

which we began expensing during 2003 under the prospective

transition method in accordance with Statement of Financial

Accounting Standards (SFAS) No. 148, “Accounting for Stock-

Based Compensation—Transition and Disclosure.” We expect the

effect of these increased expenses to be partially offset by the mix

impact of growth at Target, our lowest SG&A expense rate division.

Depreciation and Amortization

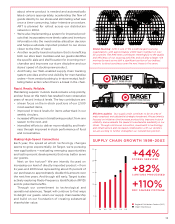

In 2003, depreciation and amortization increased 8.9 percent to

$1,320 million compared to 2002. In 2002, depreciation and

amortization increased 12.4 percent to $1,212 million compared to

2001. The increase in both years is primarily due to new store

growth at Target.

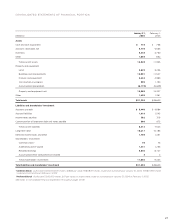

Pre-tax Segment Profit

Pre-tax segment profit is our core measure of profitability for the

three segments and is a required disclosure for segment reporting

under accounting principles generally accepted in the United

States (GAAP).

In 2003, pre-tax segment profit increased 7.9 percent to

$3,734 million, compared with $3,461 million in 2002. The increase

was driven by growth at Target, which produced 93 percent of

consolidated pre-tax segment profit. Mervyn’s and Marshall Field’s

experienced a decrease in pre-tax segment profit compared to 2002.

Pre-tax segment profit increased 16.7 percent in 2002 to

$3,461 million, compared with $2,965 million in 2001. The increase

was driven by growth at Target, which produced 89 percent of

consolidated pre-tax segment profit. Marshall Field’s pre-tax

segment profit in 2002 was essentially equal to 2001, while

Mervyn’s experienced a decline in pre-tax segment profit in 2002

compared to 2001.

A reconciliation of pre-tax segment profit to pre-tax earnings

follows. Our segment disclosures may not be consistent with

disclosures of other companies in the same line of business.