Target 2006 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2006 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

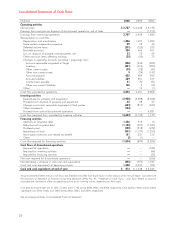

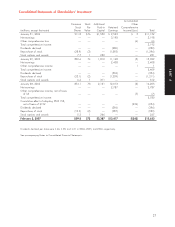

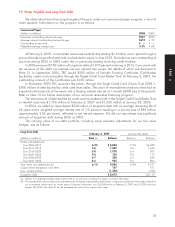

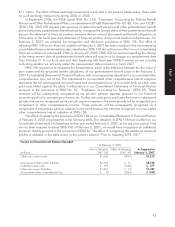

19. Notes Payable and Long-Term Debt

We obtain short-term financing throughout the year under our commercial paper program, a form of

notes payable. Information on this program is as follows:

Commercial Paper

(dollars in millions) 2006 2005

Maximum outstanding during the year $957 $994

Average amount outstanding during the year $273 $77

Outstanding at year-end $— $—

Weighted average interest rate 5.3% 4.0%

At February 3, 2007, a committed unsecured credit facility totaling $1.6 billion was in place through a

group of banks at specified rates and is scheduled to expire in June 2010. No balances were outstanding at

any time during 2006 or 2005 under this or previously existing revolving credit facilities.

In 2006 we issued $750 million of long-term debt at 5.875 percent maturing in 2016. Concurrent with

the issuance of this debt, we entered into two interest rate swaps, the details of which are disclosed in

Note 21. In September 2006, TRC issued $500 million of Variable Funding Certificates (Certificates)

backed by credit card receivables through the Target Credit Card Master Trust. At February 3, 2007, the

outstanding amount of the Certificates was $100 million.

In November 2005 TRC issued to the public, through the Target Credit Card Owner Trust 2005-1,

$900 million of debt backed by credit card receivables. This issue of receivable-backed securities had an

expected initial maturity of five years and a floating interest rate set at 1-month LIBOR plus 0.06 percent.

Refer to Note 10 for further description of our accounts receivable financing program.

The total amount of debt backed by credit card receivables held in the Target Credit Card Master Trust

or related trusts was $1,750 million at February 3, 2007 and $1,650 million at January 28, 2006.

In 2004, we called or repurchased $542 million of long-term debt with an average remaining life of

24 years and a weighted average interest rate of 7.0 percent, resulting in a pre-tax loss of $89 million

(approximately $.06 per share), reflected in net interest expense. We did not repurchase any significant

amount of long-term debt during 2006 or 2005.

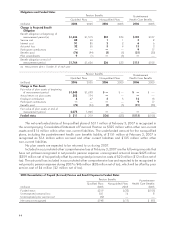

The carrying value of our debt portfolio, including swap valuation adjustments for our fair value

hedges, was as follows:

Long-Term Debt February 3, 2007 January 28, 2006

(dollars in millions) Rate (a) Balance Rate (a) Balance

Notes and debentures:

Due 2006-2010 6.2% $ 5,824 5.7% $6,480

Due 2011-2015 5.6 1,637 5.6 1,636

Due 2016-2020 5.8 1,078 6.4 307

Due 2021-2025 9.0 120 9.0 119

Due 2026-2030 6.7 326 6.7 325

Due 2031-2036 6.6 905 6.6 904

Total notes and debentures (b) 6.1% 9,890 5.9% 9,771

Capital lease obligations and other 147 101

Less: current portion (1,362) (753)

Long-term debt $ 8,675 $9,119

(a) Reflects the weighted average stated interest rate as of year-end, including the impact of interest rate swaps.

(b) The estimated fair value of total notes and debentures, excluding swap valuation adjustments, using a discounted cash flow analysis based on

our incremental interest rates for similar types of financial instruments, was $10,058 million at February 3, 2007 and $10,229 million at

January 28, 2006. See Note 21 for the estimated fair value of our interest rate swaps.

35

PART II