Target 2006 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2006 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

|

|

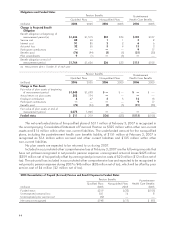

Obligations and Funded Status

Pension Benefits Postretirement

Qualified Plans Nonqualified Plans Health Care Benefits

(millions) 2006 2005 2006 2005 2006 2005

Change in Projected Benefit

Obligation

Benefit obligation at beginning of

measurement period (a) $1,626 $1,515 $33 $34 $105 $107

Service cost 82 66 1132

Interest cost 91 85 2266

Actuarial loss 32 55 5413 3

Participant contributions ————917

Benefits paid (76) (94) (5) (5) (21) (30)

Plan amendments 9(1) —(3) ——

Benefit obligation at end of

measurement period $1,764 $1,626 $36 $33 $115 $105

(a) Measurement date is October 31 of each year.

Pension Benefits Postretirement

Qualified Plans Nonqualified Plans Health Care Benefits

(millions) 2006 2005 2006 2005 2006 2005

Change in Plan Assets

Fair value of plan assets at beginning

of measurement period $1,845 $1,698 $— $— $— $—

Actual return on plan assets 303 174 ————

Employer contribution 367 5512 13

Participant contributions ————917

Benefits paid (76) (94) (5) (5) (21) (30)

Fair value of plan assets at end of

measurement period 2,075 1,845 ————

Funded status $ 311 $ 219 $(36) $(33) $(115) $(105)

The net overfunded status of the qualified plans of $311 million at February 3, 2007 is recognized in

the accompanying Consolidated Statement of Financial Position as $325 million within other non-current

assets and $14 million within other non-current liabilities. The underfunded amount for the nonqualified

plans, including the postretirement health care benefits liability, of $151 million at February 3, 2007 is

recognized as $16 million within accrued and other current liabilities and $135 million within other

non-current liabilities.

No plan assets are expected to be returned to us during 2007.

Included in accumulated other comprehensive loss at February 3, 2007 are the following amounts that

have not yet been recognized in net periodic pension expense: unrecognized actuarial losses $425 million

($259 million net of tax) partially offset by unrecognized prior service costs of $20 million ($12 million net of

tax). The actuarial loss included in accumulated other comprehensive loss and expected to be recognized in

net periodic pension expense during 2007 is $46 million ($28 million net of tax), which will be offset by prior

service cost of $4 million ($2 million net of tax).

2005 Reconciliation of Prepaid (Accrued) Pension and Benefit Expense to Funded Status

Pension Benefits Postretirement

Qualified Plans Nonqualified Plans Health Care Benefits

(millions) 2005 2005 2005

Funded status $219 $(33) $(105)

Unrecognized actuarial loss 561 16 8

Unrecognized prior service cost (32) — —

Net amount recognized $748 $(17) $ (97)

44