Yahoo 2003 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2003 Yahoo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

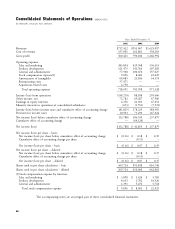

projected discounted cash flow method using a discount In May 2003, the FASB issued SFAS No. 150, ‘‘Account-

rate determined by our management to be commensurate ing for Certain Financial Instruments with Characteristics

with the risk inherent in our business model. Our esti- of Both Liabilities and Equity’’ (‘‘SFAS 150’’). SFAS 150

mates of cash flows require significant judgment based on changes the accounting for certain financial instruments

our historical results and anticipated results and are sub- that under previous guidance issuers could account for as

ject to many factors. equity. It requires that those instruments be classified as

liabilities in balance sheets. The guidance in SFAS 150 is

The Company performed its annual assessment of good- generally effective for all financial instruments entered into

will and other intangible assets in 2002 and 2003, and or modified after May 31, 2003, and otherwise is effective

concluded that there were no additional impairments. on July 1, 2003. The adoption of SFAS 150 did not have

a material impact on the Company’s financial position,

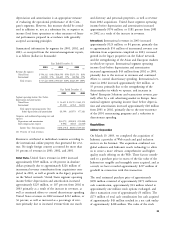

Recent Accounting Pronouncements cash flows or results of operations.

In January 2003, the Financial Accounting Standards Liquidity and Capital Resources

Board (‘‘FASB’’) issued Interpretation No. 46 (‘‘FIN 46’’)

‘‘Consolidation of Variable Interest Entities.’’ Until this In summary, our cash flows were (in thousands):

interpretation, a company generally included another

entity in its consolidated financial statements only if it

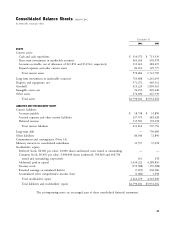

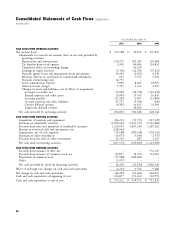

Years Ended December 31,

controlled the entity through voting interests. FIN 46 2001 2002 2003

requires a variable interest entity, as defined, to be consoli-

Net cash provided by operating

dated by a company if that company is subject to a

activities $ 106,850 $ 302,448 $ 428,144

majority of the risk of loss from the variable interest

Net cash used in investing activities (207,173) (345,854) (1,121,589)

entity’s activities or entitled to receive a majority of the

Net cash provided by (used in)

entity’s residual returns. Certain provisions of FIN 46

financing activities 18,290 (21,810) 1,086,326

were deferred until the period ending after March 15,

2004. The adoption of FIN 46 for provisions effective We invest excess cash predominantly in debt instruments

during 2003 did not have a material impact on the Com- that are highly liquid, of high-quality investment grade,

pany’s financial position, cash flows or results of and predominantly have maturities of less than two years

operations. with the intent to make such funds readily available for

operating purposes, including expansion of operations and

In April 2003, the FASB issued SFAS No. 149, ‘‘Amend- potential acquisitions or other transactions. As of Decem-

ment of Statement 133 on Derivative Instruments and ber 31, 2003, we had cash, cash equivalents, and invest-

Hedging Activities’’ (‘‘SFAS 149’’), which amends ments in marketable debt securities totaling approximately

SFAS 133 for certain decisions made by the FASB Deriva- $2.6 billion compared to approximately $1.5 billion as of

tives Implementation Group. In particular, SFAS 149: both December 31, 2002 and 2001.

(1) clarifies under what circumstances a contract with an

initial net investment meets the characteristic of a deriva- Cash provided by operating activities of $428 million for

tive, (2) clarifies when a derivative contains a financing 2003 primarily consists of net income of $238 million

component, (3) amends the definition of an underlying to adjusted for certain non-cash items of $276 million,

conform it to language used in FASB Interpretation including depreciation, amortization, tax benefits from

No. 45 ‘‘Guarantor’s Accounting and Disclosure Require- stock options, cumulative effect of accounting change,

ments for Guarantees, Including Indirect Guarantees of earnings in equity interests, (gains) losses and impairments

Indebtedness of Others,’’ and (4) amends certain other from investments, minority interests in operations of con-

existing pronouncements. This Statement is effective for solidated subsidiaries, restructuring costs, stock compensa-

contracts entered into or modified after June 30, 2003, tion expense and other non-cash items, partially offset by

and for hedging relationships designated after June 30, approximately $86 million of changes in working capital

2003. In addition, most provisions of SFAS 149 are to be and other activities. Working capital changes included an

applied prospectively. The adoption of SFAS 149 did not increase in accounts receivable balances of approximately

have a material impact on the Company’s financial posi- $122 million, reflecting increases in accounts receivable

tion, cash flows or results of operations. related to both our legacy business and to acquisitions

39