Yahoo 2003 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2003 Yahoo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

amortization of capitalized Website development costs, Effective January 1, 2002, the Company adopted State-

and other operating costs. ment of Financial Accounting Standards No. 142

(‘‘SFAS 142’’), ‘‘Goodwill and Other Intangible Assets.’’ In

Internal Use Software and Website Development Costs. The Com- accordance with SFAS 142, the Company ceased amortiz-

pany has capitalized certain internal use software and ing goodwill and performed a transitional test of its good-

Website development costs totaling $11 million and will as of January 1, 2002. See Note 4 – ‘‘Goodwill.’’

$11 million during 2002 and 2003, respectively. The esti- SFAS 142 requires that goodwill be tested for impairment

mated useful life of costs capitalized is evaluated for each at the reporting unit level (operating segment or one level

specific project and ranges from one to three years. Dur- below an operating segment) on an annual basis and

ing 2001, 2002 and 2003, the amortization of capitalized between annual tests in certain circumstances. The per-

costs totaled approximately $5 million, $9 million and formance of the test involves a two-step process. The first

$9 million, respectively. Capitalized internal use software step of the impairment test involves comparing the fair

and Website development costs are included in property value of the Company’s reporting units with the reporting

and equipment, net. unit’s carrying amount, including goodwill. The Company

generally determines the fair value of its reporting units

Advertising Costs. Advertising production costs are recorded using the expected present value of future cash flows, giv-

as expense the first time an advertisement appears. All ing consideration to the market comparable approach. If

other advertising costs are expensed as incurred. Advertis- the carrying amount of the Company’s reporting units

ing expense, including barter advertising, totaled approxi- exceeds the reporting unit’s fair value, the Company per-

mately $113 million, $94 million, and $115 million for forms the second step of the goodwill impairment test to

2001, 2002, and 2003, respectively. determine the amount of impairment loss. The second

step of the goodwill impairment test involves comparing

Benefit Plan. The Company maintains a 401(k) Profit Shar- the implied fair value of the Company’s reporting unit’s

ing Plan (the ‘‘401(k) Plan’’) for its full-time employees. goodwill with the carrying amount of that goodwill.

The 401(k) Plan allows employees of the Company to

contribute up to the Internal Revenue Code prescribed Long-Lived Assets. Long-lived assets and certain identifiable

maximum amount. Each participant in the 401(k) Plan intangible assets to be held and used are reviewed for

may elect to contribute from one percent to 17 percent of impairment whenever events or changes in circumstances

his or her annual compensation to the 401(k) Plan. The indicate that the carrying amount of such assets may not

Company matches employee contributions at a rate of be recoverable. Determination of recoverability is based on

25 percent. Employee contributions are fully vested, an estimate of undiscounted future cash flows resulting

whereas vesting in matching Company contributions from the use of the asset and its eventual disposition.

occurs at a rate of 33 percent per year of employment. Measurement of any impairment loss for long-lived assets

During 2001, 2002, and 2003, the Company’s contribu- and certain identifiable intangible assets that management

tions amounted to approximately $3 million, $3 million, expects to hold and use is based on the amount the carry-

and $5 million, respectively. ing value exceeds the fair value of the asset.

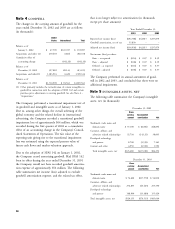

Depreciation and Amortization. Buildings are stated at cost and Other Income, net. Other income, net was as follows (in

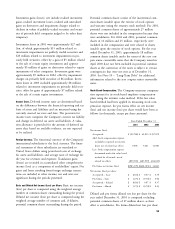

depreciated using the straight-line method over the esti- thousands):

mated useful lives of 25 years. Leasehold improvements,

computers and equipment, and furniture and fixtures are Years Ended December 31,

stated at cost and depreciated using the straight-line 2001 2002 2003

method over the estimated useful lives of the assets, gener- Interest and investment income $ 91,931 $63,200 $47,202

ally two to five years. Investment gains (losses), net (26,623) 2,189 (1,223)

Contract termination fees 9,000 1,661 750

Goodwill and other intangible assets are carried at cost Other (1,526) 2,237 777

less accumulated amortization. Intangible assets are gener-

Total other income, net $ 72,782 $69,287 $47,506

ally amortized on a straight-line basis over the economic

lives of the respective assets, generally three to seven years.

54