Yahoo 2003 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2003 Yahoo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

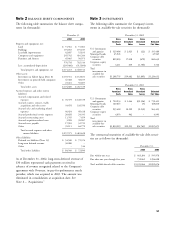

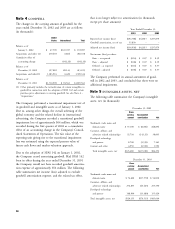

for the year ended December 31, 2002 is computed 2004. The adoption of FIN 46 for provisions effective

excluding potential common shares of 16 million shares, during 2003 did not have a material impact on the Com-

as their effect is anti-dilutive. pany’s financial position, cash flows or results of

operations.

See Note 11 – ‘‘Stockholders’ Equity’’ for the assumptions

and methodology used to determine the fair value of In April 2003, the FASB issued SFAS 149, ‘‘Amendment

stock-based compensation. of Statement 133 on Derivative Instruments and Hedging

Activities’’ (‘‘SFAS 149’’), which amends SFAS 133 for

Use of Estimates. The preparation of consolidated financial certain decisions made by the FASB Derivatives Imple-

statements in conformity with generally accepted account- mentation Group. In particular, SFAS 149: (1) clarifies

ing principles requires management to make estimates and under what circumstances a contract with an initial net

assumptions that affect the reported amounts of assets and investment meets the characteristic of a derivative,

liabilities, disclosure of contingent assets and liabilities at (2) clarifies when a derivative contains a financing compo-

the date of the financial statements, and the reported nent, (3) amends the definition of an underlying to con-

amounts of revenues and expenses during the reported form it to language used in FASB Interpretation No. 45

period. On an on-going basis, the Company evaluates its ‘‘Guarantor’s Accounting and Disclosure Requirements for

estimates, including those related to uncollectible receiv- Guarantees, Including Indirect Guarantees of Indebtedness

ables, investment values, goodwill and intangible assets, of Others,’’ and (4) amends certain other existing pro-

income taxes, restructuring costs and contingencies. The nouncements. This Statement is effective for contracts

Company bases its estimates on historical experience and entered into or modified after June 30, 2003, and for

on various other assumptions that are believed to be rea- hedging relationships designated after June 30, 2003. In

sonable under the circumstances, the results of which addition, most provisions of SFAS 149 are to be applied

form the basis for making judgments about the carrying prospectively. The adoption of SFAS 149 did not have a

values of assets and liabilities that are not readily apparent material impact on the Company’s financial position, cash

from other sources. Actual results may differ from these flows or results of operations.

estimates under different assumptions or conditions.

In May 2003, the FASB issued SFAS No. 150, ‘‘Account-

Comprehensive Income (Loss). Comprehensive income (loss) as ing for Certain Financial Instruments with Characteristics

defined, includes all changes in equity (net assets) during of Both Liabilities and Equity’’ (‘‘SFAS 150’’). SFAS 150

a period from non-owner sources. Accumulated other changes the accounting for certain financial instruments

comprehensive income (loss), as presented on the accom- that under previous guidance issuers could account for as

panying consolidated balance sheets, consists of the net equity. It requires that those instruments be classified as

unrealized gains and losses on available-for-sale securities, liabilities in balance sheets. The guidance in SFAS 150 is

net of tax, and the cumulative foreign currency translation generally effective for all financial instruments entered into

adjustment. or modified after May 31, 2003, and otherwise is effective

on July 1, 2003. The adoption of SFAS 150 did not have

Recent Accounting Pronouncements a material impact on the Company’s financial position,

cash flows or results of operations.

In January 2003, the Financial Accounting Standards

Board (‘‘FASB’’) issued Interpretation No. 46 (‘‘FIN 46’’)

‘‘Consolidation of Variable Interest Entities.’’ Until this

interpretation, a company generally included another

entity in its consolidated financial statements only if it

controlled the entity through voting interests. FIN 46

requires a variable interest entity, as defined, to be consoli-

dated by a company if that company is subject to a

majority of the risk of loss from the variable interest

entity’s activities or entitled to receive a majority of the

entity’s residual returns. Certain provisions of FIN 46

were deferred until the period ending after March 15,

56