Apple 2006 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2006 Apple annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

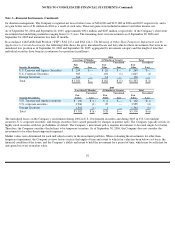

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Note 3—Financial Instruments (Continued)

The following table shows the notional principal, net fair value, and credit risk amounts of the Company’s foreign currency instruments as of

September 30, 2006 and September 24, 2005 (in millions):

The notional principal amounts for derivative instruments provide one measure of the transaction volume outstanding as of year-end, and do

not represent the amount of the Company’s exposure to credit or market loss. The credit risk amounts shown in the table above represents the

Company’

s gross exposure to potential accounting loss on these transactions if all counterparties failed to perform according to the terms of the

contract, based on then-current currency exchange rates at each respective date. The Company’s exposure to credit loss and market risk will

vary over time as a function of currency exchange rates.

The estimates of fair value are based on applicable and commonly used pricing models and prevailing financial market information as of

September 30, 2006 and September 24, 2005. Although the table above reflects the notional principal, fair value, and credit risk amounts of the

Company’s foreign exchange instruments, it does not reflect the gains or losses associated with the exposures and transactions that the foreign

exchange instruments are intended to hedge. The amounts ultimately realized upon settlement of these financial instruments, together with the

gains and losses on the underlying exposures, will depend on actual market conditions during the remaining life of the instruments.

Foreign Exchange Risk Management

The Company may enter into foreign currency forward and option contracts with financial institutions to protect against foreign exchange risk

associated with existing assets and liabilities, certain firmly committed transactions, forecasted future cash flows, and net investments in

foreign subsidiaries. Generally, the Company’s practice is to hedge a majority of its existing material foreign exchange transaction exposures.

However, the Company may not hedge certain foreign exchange transaction exposures due to immateriality, prohibitive economic cost of

hedging particular exposures, or limited availability of appropriate hedging instruments.

To help protect gross margins from fluctuations in foreign currency exchange rates, the Company’s U.S. dollar functional subsidiaries hedge a

portion of forecasted foreign currency revenue, and the Company’s non-U.S. dollar functional subsidiaries selling in local currencies hedge a

portion of forecasted inventory purchases not denominated in the subsidiaries’ functional currency. Other comprehensive income

94

September 30, 2006

September 24, 2005

Notional

Principal

Fair

Value

Credit Risk

Amounts

Notional

Principal

Fair

Value

Creit Risk

Amounts

Foreign exchange instruments qualifying as

accounting hedges:

Spot/Forward contracts

$

351

$

6

$

6

$

662

$

10

$

10

Purchased options

$

1,256

$

9

$

9

$

1,668

$

17

$

17

Sold options

$

80

$

(1

)

$

—

$

1,087

$

(5

)

$

—

Foreign exchange instruments other than

accounting hedges:

Spot/Forward contracts

$

1,103

$

2

$

2

$

833

$

(3

)

$

1

Purchased options

$

167

$

1

$

—

$

115

$

—

$

—

Sold options

$

—

$

—

$

—

$

—

$

—

$

—