Coca Cola 2006 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2006 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

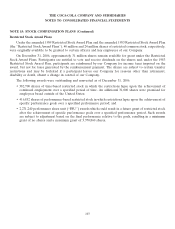

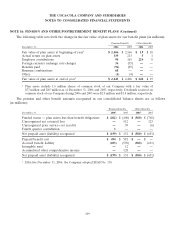

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 16: PENSION AND OTHER POSTRETIREMENT BENEFIT PLANS (Continued)

Effective December 31, 2006, the Company adopted SFAS No. 158, which required the recognition in

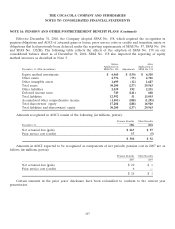

pension obligations and AOCI of actuarial gains or losses, prior service costs or credits and transition assets or

obligations that had previously been deferred under the reporting requirements of SFAS No. 87, SFAS No. 106

and SFAS No. 132(R). The following table reflects the effects of the adoption of SFAS No. 158 on our

consolidated balance sheet as of December 31, 2006. SFAS No. 158 also impacted the reporting of equity

method investees as described in Note 3.

Before After

Application of Application of

December 31, 2006 (in millions) SFAS No. 158 Adjustments SFAS No. 158

Equity method investments $ 6,460 $ (150) $ 6,310

Other assets 2,776 (75) 2,701

Other intangible assets 1,699 (12) 1,687

Total assets 30,200 (237) 29,963

Other liabilities 2,039 192 2,231

Deferred income taxes 749 (141) 608

Total liabilities 12,992 51 13,043

Accumulated other comprehensive income (1,003) (288) (1,291)

Total shareowners’ equity 17,208 (288) 16,920

Total liabilities and shareowners’ equity 30,200 (237) 29,963

Amounts recognized in AOCI consist of the following (in millions, pretax):

Pension Benefits Other Benefits

December 31, 2006 2006

Net actuarial loss (gain) $ 267 $ 97

Prior service cost (credit) 37 (5)

$ 304 $ 92

Amounts in AOCI expected to be recognized as components of net periodic pension cost in 2007 are as

follows (in millions, pretax):

Pension Benefits Other Benefits

2007 2007

Net actuarial loss (gain) $ 20 $ 1

Prior service cost (credit) 6 —

$26 $ 1

Certain amounts in the prior years’ disclosure have been reclassified to conform to the current year

presentation.

107