General Motors 2015 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2015 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

Table of Contents

The pension plans may invest in financial instruments denominated in foreign currencies and may be exposed to risks that the foreign currency exchange

rates might change in a manner that has an adverse effect on the value of the foreign currency denominated assets or liabilities. Forward currency contracts

may be used to manage and mitigate foreign currency risk.

The pension plans may invest in debt securities for which any change in the relevant interest rates for particular securities might result in an investment

manager being unable to secure similar returns upon the maturity or the sale of securities. In addition changes to prevailing interest rates or changes in

expectations of future interest rates might result in an increase or decrease in the fair value of the securities held. Interest rate swaps and other financial

derivative instruments may be used to manage interest rate risk.

Based on our current assumptions, we expect no significant mandatory contributions to our U.S. qualified pension plans for the next five years; however,

we expect mandatory contributions totaling $2.1 billion to our Canada and United Kingdom pension plans over the next five years.

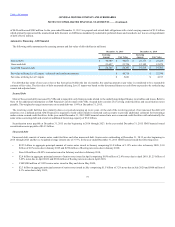

Benefits for most U.S. pension plans and certain non-U.S. pension plans are paid out of plan assets rather than our Cash and cash equivalents. The

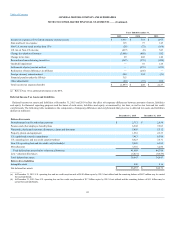

following table summarizes net benefit payments expected to be paid in the future, which include assumptions related to estimated future employee service

(dollars in millions):

2016 $ 5,636

$ 1,464

$ 384

2017 $ 5,383

$ 1,335

$ 376

2018 $ 5,228

$ 1,264

$ 367

2019 $ 5,098

$ 1,258

$ 361

2020 $ 4,979

$ 1,255

$ 357

2021 - 2025 $ 22,874

$ 6,060

$ 1,745

At December 31, 2015 and 2014 our derivative instruments consisted primarily of options and forward contracts primarily related to foreign currency. We

had derivative instruments in asset positions with notional amounts of $7.2 billion and $8.8 billion and liability positions with notional amounts of $264

million and $953 million at December 31, 2015 and 2014. The fair value of these derivative instruments was insignificant. In 2015 we designated certain

foreign currency forward contracts as cash flow hedges. The notional amounts of these designated instruments were insignificant at December 31, 2015.

GM Financial had interest rate swaps and caps and foreign currency swaps in asset positions with notional amounts of $11.9 billion and $5.4 billion and

liability positions with notional amounts of $13.9 billion and $8.5 billion at December 31, 2015 and 2014. The fair value of these derivative financial

instruments was insignificant. In 2015 GM Financial designated certain interest rate swaps as fair value hedges of fixed rate debt with notional amounts of

$1.0 billion at December 31, 2015.

The following table summarizes information related to the liabilities recorded for Commitments and contingencies (dollars in millions):

83