Humana 2003 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2003 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

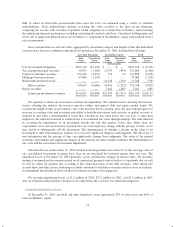

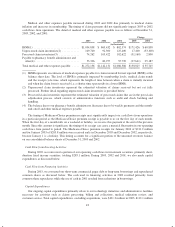

|

|

For all special purpose entities (“SPEs”) created prior to February 1, 2003, public entities must apply either

the provisions of FIN 46 or early adopt the provisions of FIN 46-R at the end of the first interim or annual

reporting period ending after December 15, 2003. If a public entity applies FIN 46 for such period, the provisions

of FIN 46-R must be applied as of the end of the first interim or annual reporting period ending after March 15,

2004. For all non-SPEs created prior to February 1, 2003, public entities will be required to adopt FIN 46-R at

the end of the first interim or annual reporting period ending after March 15, 2004. For all entities (regardless of

whether the entity is an SPE) that were created subsequent to January 31, 2003, public entities were already

required to apply the provisions of FIN 46, and should continue doing so unless they elect to early adopt the

provisions of FIN 46-R as of the first interim or annual reporting period ending after December 15, 2003. If they

do not elect to early adopt FIN 46-R, public entities would be required to apply FIN 46-R to those post-

January 31, 2003 entities as of the end of the first interim or annual reporting period ending after March 15,

2004.

As part of our ongoing business, we do not participate or knowingly seek to participate in transactions that

generate relationships with unconsolidated entities or financial partnerships, such as entities often referred to as

structured finance or SPEs, which would have been established for the purpose of facilitating off-balance sheet

arrangements or other contractually narrow or limited purposes. As of December 31, 2003, we are not involved

in any SPE transactions. The adoption of FIN 46 or FIN 46-R is not expected to have a material impact on our

financial position, results of operations or cash flows.

33