Proctor and Gamble 2008 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2008 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

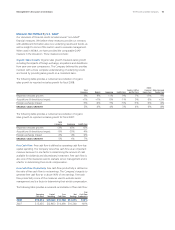

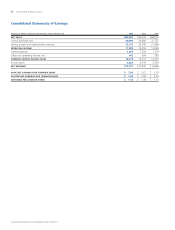

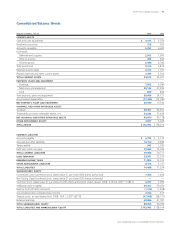

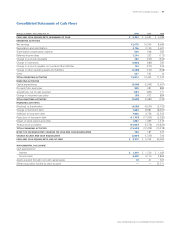

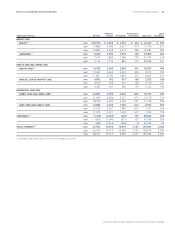

NotestoConsolidatedFinancialStatements TheProcter&GambleCompany 65

Amountsinmillionsofdollarsexceptpershareamountsorasotherwisespecied.

NOT E 5

June30 2007

Currentportionoflong-termdebt $ 2,544

Commercialpaper 9,410

FloatingratenotedueFebruary2009 —

Other 85

12,039

Theweightedaverageshort-terminterestrateswere2.7%and5.0%

asofJune30,2008and2007,respectively,includingtheeffectsof

interestrateswapsdiscussedinNote6.

June30 2007

4.30%USDnotedueAugust2008 $ 500

3.50%USDnotedueDecember2008 650

FloatingratenotedueJuly2009 —

FloatingratenotedueAugust2009 —

6.88%USDnotedueSeptember2009 1,000

4.88%EURnotedueOctober2011 —

3.38%EURnotedueDecember2012 1,882

4.50%EURnotedueMay2014 2,016

4.95%USDnotedueAugust2014 900

4.85%USDnotedueDecember2015 700

5.13%EURnotedueOctober2017 —

4.13%EURnotedueDecember2020 806

9.36%ESOPdebenturesdue2008–2021(1) 968

4.88%EURnotedueMay2027 1,344

6.25%GBPnotedueJanuary2030 1,001

5.50%USDnotedueFebruary2034 500

5.80%USDnotedueAugust2034 600

5.55%USDnotedueMarch2037 1,400

Capitalleaseobligations 628

Allotherlong-termdebt 11,024

Currentportionoflong-termdebt (2,544)

23,375

(1)DebtissuedbytheESOPisguaranteedbytheCompanyandmustberecordedasdebtofthe

CompanyasdiscussedinNote9.

Long-termweightedaverageinterestrateswere4.5%and3.3%as

ofJune30,2008and2007,respectively,includingtheeffectsof

interestrateswapsandnetinvestmenthedgesdiscussedinNote6.

Thefairvalueofthelong-termdebtwas$23,276and$23,122at

June30,2008and2007,respectively.Long-termdebtmaturities

duringthenextveyearsareasfollows:2009–$1,746;2010–$5,508;

2011–$43;2012–$1,643;and2013–$2,240.

NOT E 6

Asamultinationalcompanywithdiverseproductofferings,weare

exposedtomarketrisks,suchaschangesininterestrates,currency

exchangeratesandcommodityprices.Tomanagethevolatility

relatedtotheseexposures,weevaluateexposuresonaconsolidated

basistotakeadvantageoflogicalexposurenettingandcorrelation.

Fortheremainingexposures,weenterintovariousnancialtransactions,

whichweaccountforunderSFAS133,“AccountingforDerivative

InstrumentsandHedgingActivities,”asamendedandinterpreted.

Theutilizationofthesenancialtransactionsisgovernedbyour

policiescoveringacceptablecounterpartyexposure,instrumenttypes

andotherhedgingpractices.Wedonotholdorissuederivative

nancialinstrumentsforspeculativetradingpurposes.

Atinception,weformallydesignateanddocumentqualifyinginstru-

mentsashedgesofunderlyingexposures.Weformallyassess,both

atinceptionandatleastquarterlyonanongoingbasis,whetherthe

nancialinstrumentsusedinhedgingtransactionsareeffectiveat

offsettingchangesineitherthefairvalueorcashowsoftherelated

underlyingexposure.Fluctuationsinthevalueoftheseinstruments

generallyareoffsetbychangesinthefairvalueorcashowsofthe

underlyingexposuresbeinghedged.Thisoffsetisdrivenbythehigh

degreeofeffectivenessbetweentheexposurebeinghedgedandthe

hedginginstrument.Anyineffectiveportionofachangeinthefair

valueofaqualifyinginstrumentisimmediatelyrecognizedinearnings.

Wehavecounterpartycreditguidelinesandnormallyenterinto

transactionswithinvestmentgradenancialinstitutions.Counterparty

exposuresaremonitoreddailyanddowngradesincreditratingare

reviewedonatimelybasis.Creditriskarisingfromtheinabilityofa

counterpartytomeetthetermsofournancialinstrumentcontracts

generallyislimitedtotheamounts,ifany,bywhichthecounterparty’s

obligationsexceedourobligationstothecounterparty.Wehavenot

incurredanddonotexpecttoincurmaterialcreditlossesonourrisk

managementorothernancialinstruments.

Ourpolicyistomanageinterestcostusingamixtureofxed-rateand

variable-ratedebt.Tomanagethisriskinacost-efcientmanner,we

enterintointerestrateswapsinwhichweagreetoexchangewith

thecounterparty,atspeciedintervals,thedifferencebetweenxed

andvariableinterestamountscalculatedbyreferencetoanagreed-

uponnotionalprincipalamount.

InterestrateswapsthatmeetspeciccriteriaunderSFAS133are

accountedforasfairvalueandcashowhedges.Therewerenofair

valuehedginginstrumentsatJune30,2008,orJune30,2007.For

cashowhedges,theeffectiveportionofthechangesinfairvalueof

thehedginginstrumentisreportedinothercomprehensiveincome

(OCI)andreclassiedintointerestexpenseoverthelifeoftheunder-

lyingdebt.Theineffectiveportion,whichisnotmaterialforanyyear