Proctor and Gamble 2011 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2011 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

Management’s Discussion and AnalysisThe Procter & Gamble Company 41

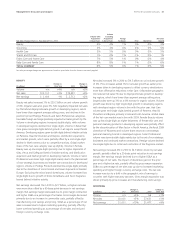

Net Sales Change Drivers vs. Year Ago (011 vs. 2010)

Volume with

Acquisitions

& Divestitures

Volume

Excluding

Acquisitions

& Divestitures

Foreign

Exchange Price Mix/Other

Net Sales

Growth

Beauty 4%4%1%0%-2%3%

Grooming 3%3%0%2%0%5%

Health Care5%5%0%0%0%5%

Snacks and Pet Care1%-2%1%-1%0%1%

Fabric Care and Home Care7%5%-1%0%-2%4%

Baby Care and Family Care8%8%-1%1%-2%6%

TOTAL COMPANY6%5%0%1%-2%5%

Net sales percentage changes are approximations based on quantitative formulas that are consistently applied.

Net sales increased 3% in 2010 to $19.5billion on unit volume growth

of 3%. Price increases added 1% to net sales growth as earlier price

increases taken in developing regions to offset currency devaluations

more than offset price reductions in Hair Care. Unfavorable geographic

mix reduced net sales 1% due to disproportionate growth in develop-

ing regions, which have lower than segment average selling prices.

Organic sales were up 3% on a 4% increase in organic volume. Volume

growth was driven by high single-digit growth in developing regions,

with developed region volume in line with the prior year. Hair Care

volume grew mid-single digits behind growth of Pantene, Head&

Shoulders and Rejoice primarily in Asia and Latin America. Global share

of the hair care market was in line with 2009. Female Beauty volume

was up low single digits as higher shipments of female skin care and

personal cleansing products in developing regions were partially offset

by the discontinuation of Max Factor in North America, the fiscal 2009

divestiture of Noxzema and volume share losses on non-strategic

personal cleansing brands in developed regions. Salon Professional

volume was down double digits mainly due to the exit of non-strategic

businesses and continued market contractions. Prestige volume declined

low single digits due to continued contraction of the fragrance market.

Net earnings increased 2% in 2010 to $2.7billion driven by net sales

growth, partially offset by a 20-basis point reduction in net earnings

margin. Net earnings margin declined due to higher SG&A as a

percentage of net sales, the impact of divestiture gains in the prior

year and a higher tax rate, partially offset by gross margin expansion.

SG&A as a percentage of net sales was up due to increased marketing

spending and higher foreign currency exchange costs. The tax rate

increase was due to a shift in the geographic mix of earnings to

countries with higher statutory tax rates. Gross margin expansion was

driven primarily by price increases and manufacturing costs savings.

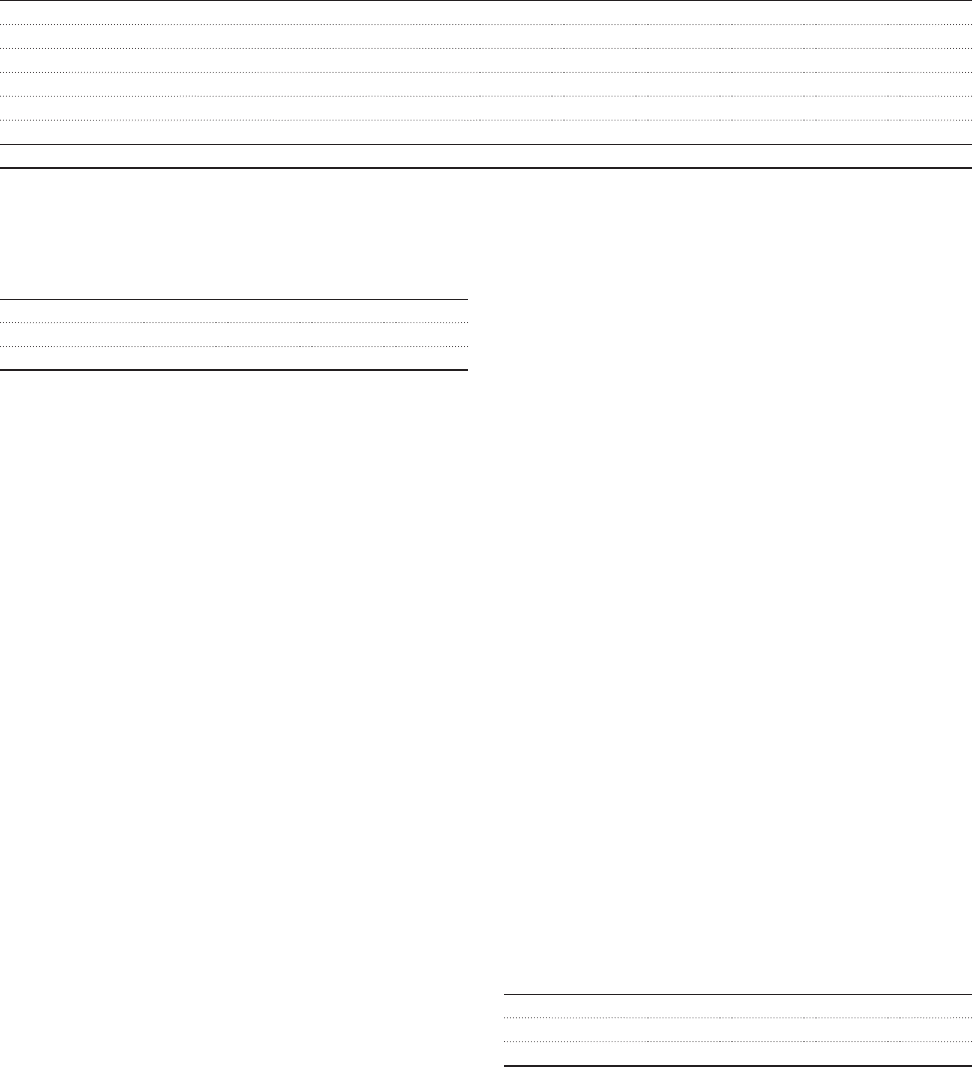

GROOMING

($ millions) 2011

Changevs.

Prior Year 2010

Changevs.

Prior Year

Volume n/a +3% n/a +1%

Net sales $8,025 +5%$7,631 +3%

Net earnings $1,631 +10%$1,477 +9%

BEAUTY

($ millions) 2011

Changevs.

Prior Year 2010

Changevs.

Prior Year

Volume n/a +4% n/a +3%

Net sales $20,157 +3% $19,491 +3%

Net earnings $2,686 -1%$2,712 +2%

Beauty net sales increased 3% to $20.2billion on unit volume growth

of 4%. Organic sales also grew 3%. Mix negatively impacted net sales

by 2% behind disproportionate growth in developing regions, which

have lower than segment average selling prices, and declines in the

premium-priced Prestige Products and Salon Professional categories.

Favorable foreign exchange positively impacted net sales growth by 1%.

Volume in developing regions increased double digits, while volume

in developed regions declined low single digits. Volume in Retail Hair

Care grew mid-single digits behind growth in all regions except North

America. Developing regions grew double digits behind initiative activity

on Pantene, Head & Shoulders and Rejoice, distribution expansions

and market growth, which were partially offset by a mid-single-digit

decline in North America due to competitive activity. Global market

share of the hair care category was up slightly. Volume in Female

Beauty was up low single digits primarily due to higher shipments of

Olay, Venus and Safeguard behind initiative activity, and distribution

expansion and market growth in developing markets. Volume in Salon

Professional was down high single digits mainly due to the planned exit

of non-strategic businesses and market size contractions in developed

regions. Volume in Prestige Products declined low single digits primarily

due to the divestiture ofminor brands and lower shipments in Western

Europe. Excluding the minor brand divestitures, volume increased low

single digits due to growth of Dolce & Gabbana and Gucci fragrance

brands behind initiative activity.

Net earnings decreased 1% in 2011 to $2.7billion, as higher net sales

were more than offset by a 60-basis point decrease in net earnings

margin. Net earnings margin decreased due to gross margin contraction

and higher SG&A as a percentage of net sales. Gross margin decreased

primarily due to an increase in commodity costs, partially offset by

manufacturing cost savings and pricing. SG&A as a percentage of net

sales increased due to higher marketing spending, partially offset by

lower overhead spending as a percentage of net sales and reduced

foreign currency exchange costs.