Proctor and Gamble 2011 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2011 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

44 The Procter & Gamble CompanyManagement’s Discussion and Analysis

mid-single digits, led by high single-digit growth in developing regions

behind initiative activity, increased distribution and market growth.

Global market share of the fabric care category increased slightly.

Home Care volume increased double digits due, in part, to the Ambi

Pur acquisition. Organic volume in Home Care was up high single

digits driven mainly by initiative activity, including launches of Gain

hand dishwashing liquid and Febreze Set& Refresh in North America,

and geographic expansion of dish and air care product lines. Global

market share of the home care category was up nearly 1point.

Batteries volume grew mid-single digits primarily due to price reductions

executed through pack count increases in North America, which were

implemented in January 2010, initiative activity in Western Europe and

market growth and distribution expansion in Asia. Global market share

of the batteries category increased more than half a point.

Net earnings decreased 10% to $3.0billion as net sales growth was

more than offset by a 190-basis point decrease in net earnings margin.

Net earnings margin decreased mainly due to gross margin contraction.

SG&A as a percentage of net sales and the effective tax rate also

increased. Gross margin decreased mainly due to higher commodity

costs and unfavorable product mix behind disproportionate growth

of developing regions and mid-tier products, partially offset by manu-

facturing cost savings. SG&A as a percentage of net sales increased

behind higher overhead spending to support growth. The tax rate

increased due to a shift in the geographic mix of earnings to countries

with higher statutory tax rates.

Net sales increased 3% to $23.8billion in 2010 on a 6% increase in

unit volume. Pricing reduced net sales by 1% as the impact of price

reductions to improve consumer value were partially offset by price

increases taken primarily in developing regions to offset currency

devaluations. Mix lowered net sales by 1% due mainly to unfavorable

geographic mix and a shift toward larger size products, which have

lower than segment average selling prices. Unfavorable foreign

exchange reduced net sales by 1%. Organic sales grew 4%. Volume

increased mid-single digits in both developed and developing regions.

Fabric Care volume grew mid-single digits behind new product

launches, price reductions and incremental merchandising activity.

Global market share of the fabric care category was down about half

a point. Home Care volume was up high single digits mainly due to

new product launches, media spending increases and market size

expansion. Global market share of the home care category was up

about half a point versus 2009. Batteries volume increased mid-single

digits primarily due to growth in Greater China, price reductions to

improve consumer value in North America and higher demand from

business customers.

Net earnings increased 10% to $3.3billion in 2010 due to higher net

sales and a 90-basis point increase in net earnings margin. Net earnings

margin increased due to higher gross margin and a lower tax rate,

partially offset by an increase in SG&A as a percentage of net sales.

Gross margin increased mainly due to lower commodity costs and

manufacturing cost savings, while SG&A as a percentage of net sales

increased due to higher marketing spending. The tax rate declined

due to a shift in the geographic mix of earnings to countries with lower

statutory tax rates.

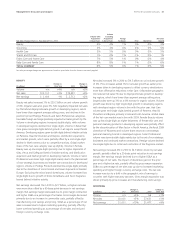

BABY CARE AND FAMILY CARE

($ millions) 2011

Changevs.

Prior Year 2010

Changevs.

Prior Year

Volume n/a +8% n/a +7%

Net sales $15,606 +6%$14,736 +4%

Net earnings $1,978 -3%$2,049 +16%

Baby Care and Family Care net sales increased 6% to $15.6billion on

8% volume growth. Organic sales were up 7%. Mix reduced net sales

by 2% driven mainly by disproportionate growth of mid-tier product

lines, larger package sizes and developing regions, all of which have

lower than segment average selling prices. Pricing added 1% to net

sales growth primarily due to price increases executed in Baby Care

tooffset higher commodity costs and foreign exchange. Unfavorable

foreign exchange negatively impacted net sales by 1%. Volume grew

double digits in developing regions and mid-single digits in developed

regions. Volume in Baby Care was up high single digits primarily due

to double-digit growth in developing regions behind initiative activity,

market size growth and distribution expansion. Global market share

of the baby care category increased over 1point. Volume in Family

Care increased high single digits driven by the continued impact of

initiatives launched in prior periods, with high single-digit growth in

North America. In the U.S., all-outlet share of the family care category

increased half a point.

Net earnings decreased 3% to $2.0billion as sales growth was more

than offset by a 120-basis point reduction in net earnings margin.

Netearnings margin declined mainly due to a lower gross margin,

partially offset by a decrease in SG&A as a percentage of net sales.

The reduction in gross margin was driven by higher commodity costs

and unfavorable product mix, behind disproportionate growth of

mid-tier product lines, larger package sizes and developing regions,

which were only partially offset by the favorable impact of volume

scale leverage and manufacturing cost savings. SG&A as a percentage

of net sales declined due to lower foreign currency exchange costs.

Net sales grew 4% to $14.7billion in 2010 on 7% volume growth.

Pricing was in line with the prior year as the impact of price increases

primarily taken in developing regions to offset local currency devalua-

tions were offset by price reductions to improve consumer value.

Negative mix reduced net sales by 2% driven mainly by disproportionate

growth of mid-tier product lines, large count packs and developing

regions, all of which have lower than segment average selling prices.

Unfavorable foreign exchange reduced net sales by 1%. Organic sales

increased 5%. Volume grew double digits in developing regions and

mid-single digits in developed regions. Volume in Baby Care increased

high single digits behind incremental initiative activity, market size

expansion and price reductions to improve consumer value, primarily

in CEEMEA. Global share of the baby care market was up over half a

point. Volume in Family Care grew high single digits due to increased

merchandising and initiative activity, market growth and price reductions

to improve consumer value.