Target 2008 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2008 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

Critical Accounting Estimates

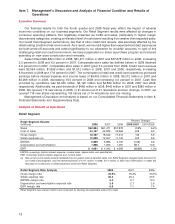

Our analysis of operations and financial condition is based on our consolidated financial statements,

prepared in accordance with U.S. generally accepted accounting principles (GAAP). Preparation of these

consolidated financial statements requires us to make estimates and assumptions affecting the reported

amounts of assets and liabilities at the date of the consolidated financial statements, reported amounts of

revenues and expenses during the reporting period and related disclosures of contingent assets and

liabilities. In the Notes to Consolidated Financial Statements, we describe the significant accounting policies

used in preparing the consolidated financial statements. Our estimates are evaluated on an ongoing basis

and are drawn from historical experience and other assumptions that we believe to be reasonable under the

circumstances. Actual results could differ under different assumptions or conditions. Our senior management

has discussed the development and selection of our critical accounting estimates with the Audit Committee of

our Board of Directors. The following items in our consolidated financial statements require significant

estimation or judgment:

Inventory and cost of sales We use the retail inventory method to account for substantially our entire

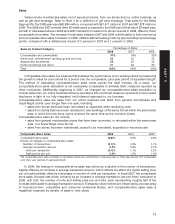

inventory and the related cost of sales. Under this method, inventory is stated at cost using the last-in, first-out

(LIFO) method as determined by applying a cost-to-retail ratio to each merchandise grouping’s ending retail

value. Cost includes the purchase price as adjusted for vendor income. Since inventory value is adjusted

regularly to reflect market conditions, our inventory methodology reflects the lower of cost or market. We

reduce inventory for estimated losses related to shrink and markdowns. Our shrink estimate is based on

historical losses verified by ongoing physical inventory counts. Historically our actual physical inventory count

results have shown our estimates to be reliable. Markdowns designated for clearance activity are recorded

when the salability of the merchandise has diminished. Inventory is at risk of obsolescence if economic

conditions change. Relevant economic conditions include changing consumer demand, changing consumer

credit markets or increasing competition. We believe these risks are largely mitigated because our inventory

typically turns in less than six months. Inventory is further described in Note 11.

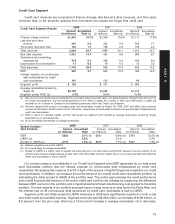

Vendor income receivable Cost of sales and SG&A expenses are partially offset by various forms of

consideration received from our vendors. This ‘‘vendor income’’ is earned for a variety of vendor-sponsored

programs, such as volume rebates, markdown allowances, promotions and advertising, as well as for our

compliance programs. We establish a receivable for the vendor income that is earned but not yet received.

Based on the agreements in place, this receivable is computed by estimating when we have completed our

performance and the amount earned. The majority of all year-end vendor income receivables are collected

within the following fiscal quarter. Vendor income is described further in Note 4.

Allowance for doubtful accounts When receivables are recorded, we recognize an allowance for doubtful

accounts in an amount equal to anticipated future write-offs. This allowance includes provisions for

uncollectible finance charges and other credit-related fees. We estimate future write-offs based on historical

experience of delinquencies, risk scores, aging trends and industry risk trends. Substantially all accounts

continue to accrue finance charges until they are written off. Accounts are automatically written off when they

become 180 days past due. Management believes the allowance for doubtful accounts is adequate to cover

anticipated losses in our credit card accounts receivable under current conditions; however, unexpected,

significant deterioration in any of the factors mentioned above or in general economic conditions could

materially change these expectations. We believe that the allowance recorded at January 31, 2009 is sufficient

to cover currently anticipated losses. Credit card receivables are described in Note 10.

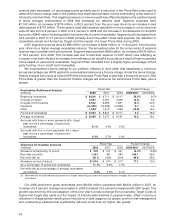

Analysis of long-lived and intangible assets for impairment We review assets at the lowest level for which

there are identifiable cash flows, usually at the store level. An impairment loss on a long-lived and identifiable

intangible asset would be recognized when estimated undiscounted future cash flows from the operation and

disposition of the asset are less than the asset carrying amount. Goodwill is tested for impairment by

comparing its carrying value to a fair value estimated by discounted future cash flows. No material

impairments were recorded in 2008, 2007 or 2006 as a result of the tests performed.

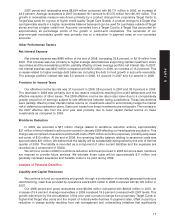

Insurance/self-insurance We retain a substantial portion of the risk related to certain general liability,

workers’ compensation, property loss and team member medical and dental claims. Liabilities associated

with these losses include estimates of both claims filed and losses incurred but not yet reported. We estimate

20