Target 2008 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2008 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

2009. However, in October 2008, the FASB issued Staff Position No. FAS 133-1 and FIN 45-4, which, amongst

other actions, accelerated the effective date of SFAS 161 to be effective for interim and annual periods

beginning after November 15, 2008. Since SFAS 161 requires only additional disclosures concerning

derivatives and hedging activities, the adoption of SFAS 161 did not have any impact on our consolidated net

earnings, cash flows or financial position.

In November 2008, the FASB Staff Position FAS 140-e and FIN 46(R)-e, Disclosures about Transfers of

Financial Assets and Interests in Variable Interest Entities (the FSP) was published with an effective date for

periods ending December 15, 2008. The FSP is intended to enhance currently required disclosures until the

pending amendments to SFAS 140, ‘‘Accounting for Transfers and Servicing of Financial Assets and

Extinguishments of Liabilities,’’ and FASB Interpretation No. 46 (revised December 2003), ‘‘Consolidation of

Variable Interest Entities,’’ are published. Since the FSP requires only additional disclosures related to certain

asset transfers, the adoption of the FSP did not have any impact on our consolidated net earnings, cash flows

or financial position.

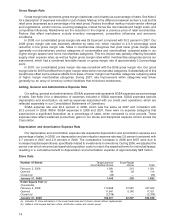

Future Adoptions

In December 2007, the FASB issued SFAS No. 141(R), ‘‘Business Combinations’’ (SFAS 141(R)), which

changes the accounting for business combinations and their effects on the financial statements. SFAS 141(R)

will be effective at the beginning of fiscal 2009. The adoption of this statement is not expected to have a

material impact on our consolidated net earnings, cash flows or financial position.

In December 2007, the FASB issued SFAS No. 160, ‘‘Accounting and Reporting of Noncontrolling

Interests in Consolidated Financial Statements, an amendment of ARB No. 51’’ (SFAS 160). SFAS 160

requires entities to report noncontrolling interests in subsidiaries as equity in their consolidated financial

statements. SFAS 160 will be effective at the beginning of fiscal 2009. The adoption of this statement is not

expected to have a material impact on our consolidated net earnings, cash flows or financial position.

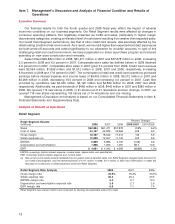

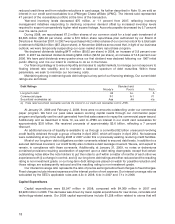

Outlook for Fiscal Year 2009

We anticipate that the challenging economic and consumer environment we experienced in 2008 will

continue into 2009. In the first half of 2009, in our Retail Segment, we expect a continuation of recent sales

trends – specifically mid-single digit declines in overall comparable-store sales with stronger growth in our

lower-margin non-discretionary categories than in our higher-margin home and apparel categories. This sales

performance will likely lead to a moderate decline in our gross margin rate because it is unlikely that we will be

able to offset the impact of the adverse sales mix with rate improvements within categories. Even in light of

continued strong expense control, we expect a moderate de-leveraging in our SG&A expense rate as a result

of our expectation for soft comparable store sales. As a result, we expect to generate EBITDA and EBIT in our

Retail Segment below last year’s levels for the first half of the year.

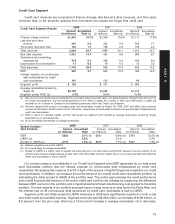

In our Credit Card Segment we expect net write-offs to stabilize in the range of $300 million in each of the

first two quarters of 2009, levels which were anticipated in establishing the allowance for doubtful accounts at

the end of fiscal 2008. We do not anticipate the need to add any meaningful reserves in the foreseeable future,

especially in light of the high likelihood that we will experience modest decreases in gross receivables.

Overall, we expect to generate moderate rates of profit in the Credit Card Segment in the first two quarters of

2009, though it is not likely to be as strong as the profits generated in the first two quarters of 2008.

In light of the current environment, we are being very deliberate in the management and application of

cash resources. This means that we have planned for fewer stores to open in 2009, particularly in our October

cycle, than we would have in a more robust environment. Specifically, we expect to open about 75 stores in

2009, or about 60 stores net of rebuilds and relocations. Based on these store opening expectations, our base

capital investment plan for 2009 envisions investing just over $2 billion, with the possibility that it might be as

high as $2.5 billion if we were to see clear and measurable signs of improvement in the economy that lead us

to approve incremental store openings in 2010 and beyond.

We expect to again generate more than $4 billion in cash from operations in 2009, which, in light of our

current suspension of substantially all share repurchase activity, would provide ample cash from internal

sources to fund our projected capital investments, pay dividends on our common stock and fund the

$1.3 billion of debt that is maturing in 2009, all without the need to access the term debt capital markets during

the year.

Our expectation is for earnings per share (diluted) in the first two quarters of 2009 to be well below 2008

levels, in line with our experience in the fourth quarter of 2008. Whether our performance will improve in the

22