Target 2008 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2008 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

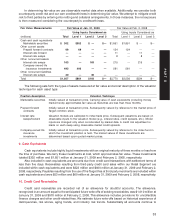

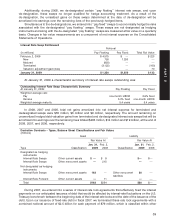

Additionally, during 2008, we de-designated certain ‘‘pay floating’’ interest rate swaps, and upon

de-designation, these swaps no longer qualified for hedge accounting treatment. As a result of the

de-designation, the unrealized gains on these swaps determined at the date of de-designation will be

amortized into earnings over the remaining lives of the previously hedged items.

Simultaneous to the de-designations, we entered into ‘‘pay fixed’’ swaps to economically hedge the risks

associated with the de-designated ‘‘pay floating’’ swaps. These swaps are not designated as hedging

instruments and along with the de-designated ‘‘pay floating’’ swaps are measured at fair value on a quarterly

basis. Changes in fair value measurements are a component of net interest expense on the Consolidated

Statements of Operations.

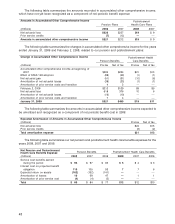

Interest Rate Swap Rollforward

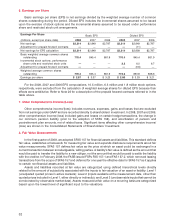

Notional

(in millions) Pay Floating Pay Fixed Total Fair Value

February 2, 2008 $ 4,575 $ — $ 223

New 750 1,250 —

Matured (950) — —

Terminated (3,125) — (160)

Valuation adjustment gain/(loss) — — 70

January 31, 2009 $ 1,250 $1,250 $ 133

At January 31, 2009 a characteristic summary of interest rate swaps outstanding was:

Outstanding Interest Rate Swap Characteristic Summary

At January 31, 2009: Pay Floating Pay Fixed

Weighted average rate:

Pay one-month LIBOR 2.6% fixed

Receive 5.0% fixed one-month LIBOR

Weighted average maturity 5.4 years 5.4 years

In 2008, 2007 and 2006, total net gains amortized into net interest expense for terminated and

dedesignated swaps were $55 million, $6 million and $9 million, respectively. The amount remaining on

unamortized hedged debt valuation gains from terminated and de-designated interest rate swaps that will be

amortized into earnings over the remaining lives totaled $263 million, $14 million and $19 million, at the end of

2008, 2007, and 2006, respectively.

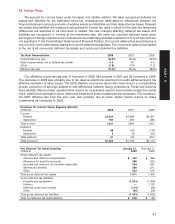

Derivative Contracts – Types, Balance Sheet Classifications and Fair Values

(millions)

Asset Liability

Fair Value At Fair Value At

Jan. 31, Feb. 2, Jan. 31, Feb. 2,

Type Classification 2009 2008 Classification 2009 2008

Designated as hedging

instruments:

Interest Rate Swaps Other current assets $— $8 $— $—

Interest Rate Swaps Other noncurrent assets —215 ——

Not designated as hedging

instruments:

Interest Rate Swaps Other noncurrent assets 163 — Other noncurrent 30 —

liabilities

Interest Rate Forward Other current assets —11 ——

Total $163 $234 $30 $—

During 2007, we entered into a series of interest rate lock agreements that effectively fixed the interest

payments on our anticipated issuance of debt that would be affected by interest-rate fluctuations on the U.S.

Treasury benchmark between the beginning date of the interest rate locks and the date of the issuance of the

debt. Upon our issuance of fixed-rate debt in fiscal 2007, we terminated these rate lock agreements with a

combined notional amount of $2.5 billion for cash payment of $79 million, which is classified within other

39

PART II