Target 2008 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2008 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

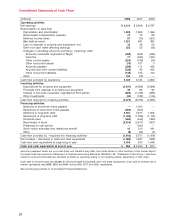

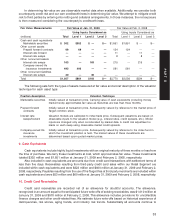

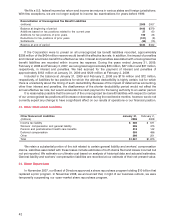

accrue finance charges until they are written off. Total accounts receivable past due ninety days or more and

still accruing finance charges were $393 million at January 31, 2009 and $235 million at February 2, 2008.

Accounts are written off when they become 180 days past due.

As a method of providing funding for our accounts receivable, we sell on an ongoing basis all of our

consumer credit card receivables to Target Receivables Corporation (TRC), a wholly owned, bankruptcy

remote subsidiary. TRC then transfers the receivables to the Target Credit Card Master Trust (the Trust), which

from time to time will sell debt securities to third parties either directly or through a related trust. These debt

securities represent undivided interests in the Trust assets. TRC uses the proceeds from the sale of debt

securities and its share of collections on the receivables to pay the purchase price of the receivables to Target.

We consolidate the receivables within the Trust and any debt securities issued by the Trust, or a related

trust, in our Consolidated Statements of Financial Position based upon the applicable accounting guidance.

The receivables transferred to the Trust are not available to general creditors of Target. The payments to the

holders of the debt securities issued by the Trust or the related trust are made solely from the assets

transferred to the Trust or the related trust, and are nonrecourse to the general assets of Target. Upon

termination of the securitization program and repayment of all debt securities, any remaining assets could be

distributed to Target in a liquidation of TRC.

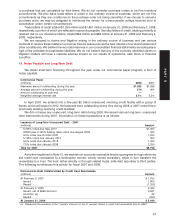

In the second quarter of 2008, we sold an interest in our credit card receivables to a JPMorgan Chase

affiliate (JPMC). The interest sold represented 47 percent of the receivables portfolio at the time of the

transaction. This transaction was accounted for as a secured borrowing, and accordingly, the receivables

within the trust and the note payable issued by the trust are reflected in our Consolidated Statements of

Financial Position. Notwithstanding this accounting treatment, the receivables transferred to the trust are not

available to general creditors of Target, and the payments to JPMC are made solely from the trust assets and

are nonrecourse to the general assets of Target. The accounts receivable assets that collateralize the note

payable supply the cash flow to pay principal and interest to the note holder. Periodic interest payments due

on the note are satisfied provided the cash flows from the trust assets are sufficient. If the cash flows are less

than the periodic interest, the available amount, if any, is paid with respect to interest. Interest shortfalls will be

paid to the extent subsequent cash flows from the assets in the trust are sufficient.

In the event of a decrease in the receivables principal amount such that JPMC’s interest in the entire

portfolio would exceed 47 percent for three consecutive months, TRC (using the cash flows from the assets in

the trust) would pay JPMC a pro rata amount of principal collections such that the interest owned by JPMC

would not exceed 47 percent. Conversely, at the option of the Corporation, JPMC may be required to fund an

increase in the portfolio to maintain their 47 percent interest up to a maximum JPMC principal balance of

$4.2 billion. If a three month average of monthly finance charge excess (JPMC’s prorata share of finance

charge collections less write-offs and specified expenses) is less than 2 percent of the outstanding principal

balance of JPMC’s interest, the Corporation must implement mutually agreed upon underwriting strategies. If

the three month average finance charge excess falls below 1 percent of the outstanding principal balance of

JPMC’s interest, JPMC may compel the Corporation to implement underwriting and collections activities,

provided those activities are compatible with the Corporation’s systems, as well as consistent with similar

credit card receivable portfolios managed by JPMC. If the Corporation fails to implement the activities, JPMC

may cause the accelerated repayment of the note payable issued in the transaction.

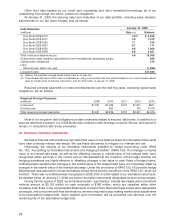

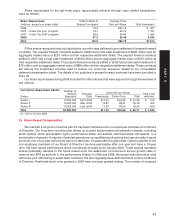

Substantially all of our inventory and the related cost of sales are accounted for under the retail inventory

accounting method (RIM) using the last-in, first-out (LIFO) method. Inventory is stated at the lower of LIFO cost

or market. Cost includes purchase price as adjusted for vendor income. Inventory is also reduced for

estimated losses related to shrink and markdowns. The LIFO provision is calculated based on inventory

levels, markup rates and internally measured retail price indices.

Under RIM, inventory cost and the resulting gross margins are calculated by applying a cost-to-retail ratio

to the retail value inventory. RIM is an averaging method that has been widely used in the retail industry due to

its practicality. The use of RIM will result in inventory being valued at the lower of cost or market since

permanent markdowns are currently taken as a reduction of the retail value of inventory.

We routinely enter into arrangements with certain vendors whereby we do not purchase or pay for

merchandise until the merchandise is ultimately sold to a guest. Revenues under this program are included in

sales in the Consolidated Statements of Operations, but the merchandise received under the program is not

included in inventory in our Consolidated Statements of Financial Position because of the virtually

34

11. Inventory