Target 2008 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2008 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

last two quarters of 2009 will depend on the extent to which economic conditions improve, and in turn to what

extent our Retail Segment sales improve, and to a lesser degree when, and to what extent, we begin to

experience clear and measurable benefits of recent risk management efforts in the Credit Card Segment.

This report contains forward-looking statements, which are based on our current assumptions and

expectations. These statements are typically accompanied by the words ‘‘expect,’’ ‘‘may,’’ ‘‘could,’’ ‘‘believe,’’

‘‘would,’’ ‘‘might,’’ ‘‘anticipates,’’ or words of similar import. The principal forward-looking statements in this

report include: The expected earnings per share (diluted) for the first two quarters of 2009; for our Retail

Segment, our outlook for sales trends, gross margin rates, SG&A expense rate, and EBITDA and EBIT; for our

Credit Card Segment, our outlook for future write-offs of current receivables, profit, and the allowance for

doubtful accounts; the expected cash generated from operations in 2009; our expected capital expenditures

and the number of stores to be opened in 2009; the expected compliance with debt covenants; and the

adequacy of our reserves for general liability, workers’ compensation, property loss, team member medical

and dental claims, workforce reduction costs, the expected outcome of claims and litigation and the

resolution of tax uncertainties.

All such forward-looking statements are intended to enjoy the protection of the safe harbor for forward-

looking statements contained in the Private Securities Litigation Reform Act of 1995, as amended. Although

we believe there is a reasonable basis for the forward-looking statements, our actual results could be

materially different. The most important factors which could cause our actual results to differ from our forward-

looking statements are set forth on our description of risk factors in Item 1A to this Form 10-K, which should be

read in conjunction with the forward-looking statements in this report. Forward-looking statements speak only

as of the date they are made, and we do not undertake any obligation to update any forward-looking

statement.

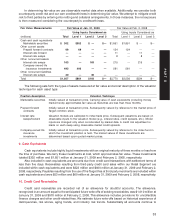

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

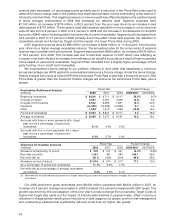

Our exposure to market risk results primarily from interest rate changes on our debt obligations, some of

which are at a LIBOR-plus floating rate, and on our credit card receivables, the majority of which are assessed

finance charges at a prime-based floating rate. To manage our net interest margin, we generally maintain

levels of floating-rate debt to generate similar changes in net interest expense as finance charge revenues

fluctuate. Our degree of floating asset and liability matching may vary over time and vary in different interest

rate environments. At January 31, 2009, our level of floating-rate credit card assets exceeded our level of net

floating-rate debt obligations by approximately $1.3 billion. As a result, based on our balance sheet position at

January 31, 2009, the annualized effect of a half percentage point decrease in floating interest rates on our

floating rate debt obligations, net of our floating rate credit card assets and marketable securities, would be to

decrease earnings before income taxes by approximately $7 million. See further description in Note 20.

We record our general liability and workers’ compensation liabilities at net present value; therefore, these

liabilities fluctuate with changes in interest rates. Periodically and in certain interest rate environments, we

economically hedge a portion of our exposure to these interest rate changes by entering into interest rate

forward contracts that partially mitigate the effects of interest rate changes. Based on our balance sheet

position at January 31, 2009, the annualized effect of a one percentage point decrease in interest rates would

be to decrease earnings before income taxes by approximately $19 million.

In addition, we are exposed to market return fluctuations on our qualified defined benefit pension plans.

The annualized effect of a one percentage point decrease in the return on pension plan assets would

decrease plan assets by $18 million at January 31, 2009. The resulting impact on net pension expense would

be calculated consistent with the provisions of SFAS No. 87, ‘‘Employers’ Accounting for Pensions.’’ The

value of our pension liabilities is inversely related to changes in interest rates. To protect against declines in

interest rates we hold high-quality, long-duration bonds and interest rate swaps in our pension plan trust. At

year end, we had hedged approximately 50 percent of the interest rate exposure of our funded status.

As more fully described in Note 14 and Note 26, we are exposed to market returns on accumulated team

member balances in our nonqualified, unfunded deferred compensation plans. We control our risk of offering

the nonqualified plans by making investments in life insurance contracts and prepaid forward contracts on our

own common stock that offset a substantial portion of our economic exposure to the returns on these plans.

The annualized effect of a one percentage point change in market returns on our nonqualified defined

contribution plans (inclusive of the effect of the investment vehicles used to manage our economic exposure)

would not be significant.

We do not have significant direct exposure to foreign currency rates as all of our stores are located in the

United States, and the vast majority of imported merchandise is purchased in U.S. dollars.

Overall, there have been no material changes in our primary risk exposures or management of market

risks since the prior year.

23

PART II

Forward-Looking Statements