Verizon Wireless 2009 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2009 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

25

movements in foreign exchange rates versus the U.S. dollar. The decline

in long distance revenue is driven by a 2.2% decline in MOUs compared

to 2008, due to continuing global economic conditions and competi-

tive rate pressures, which adversely impact our business customers.

Traditional circuit based services such as frame relay, private line and

ATM services declined compared to the similar period last year as our

customer base continues its migration to next generation IP services.

Customer premises equipment revenue decreased approximately 6.0%

compared to 2008 reflecting cautious investment decisions in the mar-

ketplace in response to the uncertain economic environment. Partially

offsetting these declines was an increase of 11.0% in IP and security

solutions revenues. Strategic services continues to be Global Enterprise’s

fastest growing suite of offerings, reflecting a 4.3% increase in revenue for

2009, compared to 2008.

Global Enterprise revenues in 2008 increased by $69 million, or 0.4%, com-

pared to 2007. The revenue increase was due to increases in customer

premise equipment revenue and security solutions revenue, partially

offset by revenue decline due to certain customers moving traffic off of

our network and lower long distance and traditional circuit based data

revenues combined with the negative effects of movements in foreign

exchange rates versus the U.S. dollar. The IP and service suite of products

continue to be Global Enterprise’s fastest growing and includes private IP,

IP, VPN, Managed Services, Web Hosting and VOIP.

Global Wholesale

Global Wholesale revenues are primarily earned from long distance and

other carriers who use our facilities to provide services to their customers.

Switched access revenues are generated from fixed and usage-based

charges paid by carriers for access to our local network, interexchange

wholesale traffic sold in the U.S., as well as internationally destined traffic

that originates in the U.S. Special access revenues are generated from car-

riers that buy dedicated local exchange capacity to support their private

networks. Wholesale services also include local wholesale revenues from

unbundled network elements and interconnection revenues from com-

petitive local exchange carriers and wireless carriers. A portion of Global

Wholesale revenues are generated by a few large telecommunication

companies, many of whom compete directly with us.

Global Wholesale revenues during 2009 decreased by $723 million, or

7.0%, compared to 2008, primarily due to decreased MOUs in traditional

voice products, and continued rate compression due to competition in

the marketplace. Switched access and interexchange wholesale MOUs

declined primarily as a result of wireless substitution and access line

losses. Wholesale lines declined by 19.7% in 2009 due to the continued

impact of competitors deemphasizing their local market initiatives

coupled with the impact of technology substitution as well as the con-

tinued level of economic pressure, as compared to an 18.8% decline in

2008. Changes in foreign exchange rates resulted in a revenue decline

of approximately 1.0% in 2009, compared to 2008. Continuing demand

for high-capacity, high-speed digital services was partially offset by lower

demand for older, low-speed data products and services. As of December

31, 2009, customer demand, as measured in DS1 and DS3 circuits, for

high-capacity and digital data services increased 2.2% compared to an

increase of 5.1% in 2008.

Global Wholesale revenues in 2008 decreased by $390 million, or 3.6%,

compared to 2007 due to declines in switched access revenues in tradi-

tional voice products and local wholesale revenues and continued rate

compression in the marketplace, partially offset by increases in special

access revenues. Switched MOUs declined in 2008, reflecting the impact

of access line losses and wireless substitution. Wholesale lines decreased

by 18.8% in 2008 due to the continued impact of competitors deempha-

sizing their local market initiatives coupled with the impact of technology

substitution compared to a 16.1% decline in 2007. Special access revenue

growth reflects continuing demand for high-capacity, high-speed dig-

ital services, partially offset by lower demand for older, low-speed data

products and services. As of December 31, 2008, customer demand, as

measured in DS1 and DS3 circuits, for high-capacity and digital data ser-

vices increased 5.1% compared to an increase of 8.2% in 2007.

The FCC regulates the rates charged to customers for interstate access

services. See “Other Factors That May Affect Future Results – Regulatory

and Competitive Trends – FCC Regulation” for additional information on

FCC rulemaking concerning federal access rates, universal service and

certain broadband services.

Other Revenues

Other revenues include such services as local exchange and long

distance services from former MCI mass market customers, operator ser-

vices, pay phone, card services and supply sales, as well as dial around

services including 10-10-987, 10-10-220, 1-800-COLLECT and prepaid

cards. Revenues from other services during 2009 decreased $576 million,

or 25.3%, compared to 2008, mainly due to the discontinuation of non-

strategic product lines and reduced business volumes, including former

MCI mass market customer losses.

Other revenues decreased by $823 million, or 26.6% in 2008, mainly due

to the discontinuation of non-strategic product lines and reduced busi-

ness volumes.

Management’s Discussion and Analysis

of Financial Condition and Results of Operations continued

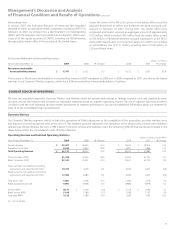

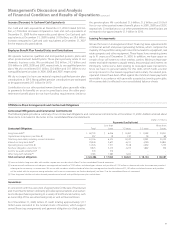

Operating Expenses (dollars in millions)

Years Ended December 31, 2009 2008 % Change 2008 2007 % Change

Cost of services and sales $ 24,144 $ 24,274 (0.5) $ 24,274 $ 24,181 0.4

Selling, general and administrative expense 10,833 11,047 (1.9) 11,047 11,527 (4.2)

Depreciation and amortization expense 9,122 9,031 1.0 9,031 8,927 1.2

Total Operating Expenses $ 44,099 $ 44,352 (0.6) $ 44,352 $ 44,635 (0.6)

Cost of Services and Sales

Cost of services and sales includes costs directly attributable to a ser-

vice or product, including salaries and wages, benefits, materials and

supplies, contracted services, network access and transport costs, cus-

tomer provisioning costs, computer systems support, costs to support

our outsourcing contracts and technical facilities, contributions to the

universal service fund, and cost of products sold. Aggregate customer

care costs, which include billing and service provisioning, are allocated

between Cost of services and sales and Selling, general and administra-

tive expense.

Cost of services and sales in 2009 decreased by $130 million, or 0.5%,

compared to 2008. The decreases were primarily due to lower costs asso-

ciated with compensation, installation, repair and maintenance expenses

as a result of fewer access lines, lower headcount and productivity

improvements. Also contributing to the decreases were lower long dis-

tance MOUs and customer premise equipment costs, as well as favorable

foreign exchange movements. Partially offsetting these decreases were

higher content and customer acquisition costs associated with continued

subscriber growth. Our FiOS TV and FiOS Internet cost of acquisition per

addition also decreased in 2009, compared to 2008.