Verizon Wireless 2009 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2009 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

30

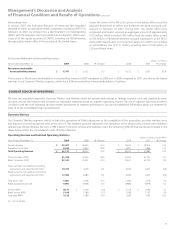

Credit Ratings

The amount of cash that we need to service our debt substantially

increased with the acquisition of Alltel. Our ability to make payments on

our debt will depend largely upon our cash balances and future oper-

ating performance. The debt securities of Verizon Communications and

its subsidiaries continue to be accorded high ratings by the three primary

rating agencies.

Standard & Poor’s (S&P) assigns an ‘A’ Corporate Credit Rating and an ‘A-1’

short-term rating to Verizon Communications. The outlook is Negative.

In May 2009 S&P affirmed these ratings and placed Verizon subsidiaries

North, Northwest and West Virginia on CreditWatch with Negative impli-

cations in connection with the Frontier transaction. S&P assigns an ‘A’

Corporate Credit Rating to Cellco Partnership with a Negative outlook.

Moody’s Investors Service (Moody’s) assigns an ‘A3’ long-term debt rating

and a ‘P-2’ short-term rating to Verizon Communications. In October 2009

Moody’s affirmed these ratings and changed the outlook from Negative

to Stable. In May 2009 Moody’s placed Verizon subsidiaries North,

Northwest and West Virginia on review for possible downgrade in con-

nection with the Frontier transaction. Moody’s assigns an ‘A2’ long-term

debt rating to Cellco Partnership. In October 2009 Moody’s changed the

Cellco Partnership outlook from Negative to Stable.

Fitch Ratings (Fitch) assigns an ‘A’ long-term Issuer Default Rating and a

‘F-1’ short-term rating to Verizon Communications. The outlook is Stable.

In May 2009, Fitch affirmed this rating and placed Verizon subsidiaries

North, Northwest and West Virginia on Rating Watch Negative in con-

nection with the Frontier transaction. Fitch assigns an ‘A’ long-term Issuer

Default Rating to Cellco Partnership with a Stable outlook.

While we do not anticipate a ratings downgrade, the three primary rating

agencies have identified factors which they believe could result in a rat-

ings downgrade for Verizon Communications and/or Cellco Partnership in

the future including sustained leverage levels at Verizon Communications

and/or Cellco Partnership resulting from: (i) diminished wireless operating

performance as a result of a weakening economy and competitive pres-

sures; (ii) failure to achieve significant synergies in the Alltel integration;

(iii) accelerated wireline losses; (iv) the absence of material improvement

in the status of underfunded pension balances; or (v) an acquisition or

sale of operations that causes a material deterioration in its credit metrics.

A ratings downgrade may increase the cost of refinancing existing debt

and might constrain Verizon Communications’ access to certain short-

term debt markets. Securities ratings assigned by rating organizations are

expressions of opinion and are not recommendations to buy, sell, or hold

securities. A securities rating is subject to revision or withdrawal at any

time by the assigning rating organization. Each rating should be evalu-

ated independently of any other rating.

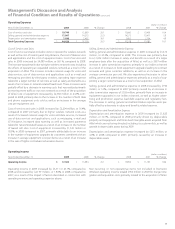

Covenants

Our credit agreements contain covenants that are typical for large,

investment grade companies. These covenants include requirements to

pay interest and principal in a timely fashion, to pay taxes, to maintain

insurance with responsible and reputable insurance companies, to pre-

serve our corporate existence, to keep appropriate books and records of

financial transactions, to maintain our properties, to provide financial and

other reports to our lenders, to limit pledging and disposition of assets

and mergers and consolidations, and other similar covenants.

In addition, Verizon Wireless is required to maintain on the last day of any

period of four fiscal quarters a leverage ratio of debt to earnings before

interest, taxes, depreciation, amortization and other adjustments, as

defined in the related credit agreement, not in excess of 3.25 times based

on the preceding twelve months. At December 31, 2009, the leverage

ratio was 1.1 times.

As of December 31, 2009, we and our consolidated subsidiaries were in

compliance with all of our debt covenants.

Our total debt was reduced by $5.2 billion in 2007. We repaid approxi-

mately $1.7 billion of Wireline debt, including the early repayment of

previously guaranteed $0.3 billion 7.0% debentures issued by Verizon

South Inc. and $0.5 billion 7.0% debentures issued by Verizon New

England Inc., as well as approximately $1.6 billion of other borrowings.

Also, we redeemed $1.6 billion principal of our outstanding floating rate

notes, which were called on January 8, 2007, and the $0.5 billion 7.9%

debentures issued by GTE Corporation. Partially offsetting the reduction

in total debt were cash proceeds of $3.4 billion in connection with fixed

and floating rate debt issued during 2007.

Credit Facility and Shelf Registration

On April 15, 2009, we terminated all commitments under our previous

$6.0 billion three-year credit facility with a syndicate of lenders that was

scheduled to mature in September 2009 and entered into a new $5.3 bil-

lion 364-day credit facility with a group of major financial institutions. As

of December 31, 2009, the unused borrowing capacity under the 364-day

credit facility was approximately $5.2 billion. Approximately $0.1 billion of

stand-by letters of credit are outstanding under the new credit facility.

The $5.3 billion 364-day credit facility does not require us to comply with

financial covenants or maintain specified credit ratings, and it permits us

to borrow even if our business has incurred a material adverse change.

The credit facility contains provisions that permit us to convert any bor-

rowings that are outstanding at maturity to a term loan with a maturity

date of one year from the original maturity date of the credit facility. We

use the credit facility to support the issuance of commercial paper, for

the issuance of letters of credit and for general corporate purposes.

We have a shelf registration available for the issuance of up to $4.0 billion

of additional unsecured debt or equity securities.

Verizon’s ratio of debt to debt combined with Verizon’s equity was 59.9%

at December 31, 2009 compared to 55.5% at December 31, 2008.

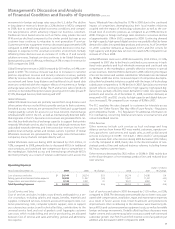

Dividends Paid

During 2009, we paid $5.3 billion in dividends as compared to $5.0

billion in 2008 and $4.8 billion in 2007. As in prior periods, dividend pay-

ments were a significant use of capital resources. The Board of Directors

of Verizon determines the appropriateness of the level of our dividend

payments on a periodic basis by considering such factors as long-term

growth opportunities, internal cash requirements and the expectations

of our shareowners. During the third quarter of 2009, the Board increased

our quarterly dividend payments 3.3% to $.475 per share from $.460 per

share. During the third quarter of 2008 and 2007, the Board increased our

dividend payments 7.0% and 6.2%, respectively.

Common Stock

Common stock has been used from time to time to satisfy some of the

funding requirements of employee and shareowner plans. On February 7,

2008, the Board of Directors replaced the current share buy back program

with a new program for the repurchase of up to 100 million common

shares terminating no later than the close of business on February 28,

2011. The Board also determined that no additional shares were to be

purchased under the prior program. During the first quarter of 2009,

we entered into a privately negotiated prepaid forward agreement for

14 million shares of Verizon common stock. During the fourth quarter of

2009, we terminated the prepaid forward agreement with respect to 5

million shares of Verizon common stock, which resulted in the delivery

of those shares to Verizon. There were no repurchases of common stock

during 2009. During 2008 and 2007, we repurchased $1.4 billion and $2.8

billion of our common stock, respectively.

Management’s Discussion and Analysis

of Financial Condition and Results of Operations continued