Verizon Wireless 2009 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2009 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

|

|

Notes to Consolidated Financial Statements continued

65

in asset backed securities such as collateralized mortgage obligations,

mortgage backed securities and interest rate swaps. The fair value of

fixed income securities are based on observable prices for identical or

comparable assets, adjusted using benchmark curves, sector grouping,

matrix pricing, broker/dealer quotes and issuer spreads, and are generally

classified within Level 1 or Level 2 in the fair value hierarchy.

Real estate investments include those in limited partnerships that invest

in various commercial and residential real estate projects both domesti-

cally and internationally. The fair values of real estate assets are typically

determined by using income and/or cost approaches or comparable sales

approach, taking into consideration discount and capitalization rates,

financial conditions, local market conditions and the status of the capital

markets, and thus are classified within Level 3 in the fair value hierarchy.

Private equity investments include those in limited partnerships that invest

in operating companies that are not publicly traded on a stock exchange.

Investment strategies in private equity include leveraged buyouts, ven-

ture capital, distressed investments and investments in natural resources.

These investments are valued using inputs such as trading multiples of

comparable public securities, merger and acquisition activity and pricing

data from the most recent equity financing taking into consideration illi-

quidity, and thus are classified within Level 3 in the fair value hierarchy.

Hedge fund investments include those seeking to maximize absolute

returns using a broad range of strategies to enhance returns and provide

additional diversification. The fair values of hedge funds are estimated

using net asset value per share (NAV) of the investments. Verizon has the

ability to redeem these investments at NAV within the near term and

thus are classified within Level 2 of the fair value hierarchy.

Cash Flows

In 2009, we contributed $213 million to our qualified pension plans, $124

million to our nonqualified pension plans and $1,638 million to our other

postretirement benefit plans. We have no material required qualified pen-

sion plan contributions in 2010. We also anticipate approximately $140

million in contributions to our non-qualified pension plans and $1,890

million to our other postretirement benefit plans in 2010.

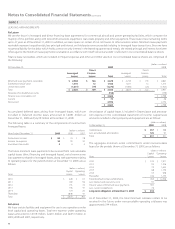

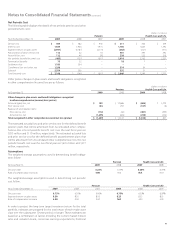

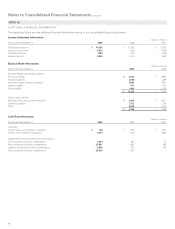

Estimated Future Benefit Payments

The benefit payments to retirees are expected to be paid as follows:

(dollars in millions)

Year

Pension

Benefits

Health Care and Life

Prior to Medicare

Prescription

Drug Subsidy

Expected

Medicare Prescription

Drug Subsidy

2010 $ 5,599 $ 2,076 $99

2011 3,796 2,158 108

2012 2,134 2,169 120

2013 2,206 2,182 130

2014 2,173 2,175 140

2015 – 2019 10,723 10,379 857

Savings Plan and Employee Stock Ownership Plans

We maintain four leveraged employee stock ownership plans (ESOP).

Only one plan currently has unallocated shares. We match a certain per-

centage of eligible employee contributions to the savings plans with

shares of our common stock from this ESOP. At December 31, 2009, the

number of unallocated and allocated shares of common stock in this

ESOP were 3 million and 68 million, respectively. All leveraged ESOP

shares are included in earnings per share computations.

Total savings plan costs were $725 million, $683 million and $712 million

in 2009, 2008 and 2007, respectively.

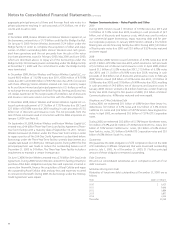

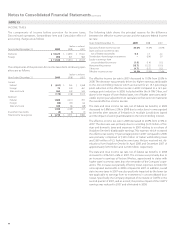

Severance Benefits

The following table provides an analysis of our severance liability recorded

in accordance with the accounting standard regarding employers’

accounting for postemployment benefits:

(dollars in millions)

Year

Beginning

of Year

Charged to

Expense Payments Other End of Year

2007 $ 644 $ 743 $ (363) $ –$ 1,024

2008 1,024 570 (509) 19 1,104

2009 1,104 1,034 (522) 22 1,638

The remaining severance liability is actuarially determined and includes

the impact of the activities described below. The 2009 expense

includes charges for the involuntary separation of approximately 17,600

employees and related charges; 4,200 of whom were separated in late

2009, with the remainder expected to occur in 2010. The 2008 expense

includes charges for the involuntary separation of approximately 8,600

employees, including approximately 3,500 of whom were separated in

the second half of 2008 and the remainder in 2009. The 2007 expense

includes charges for the involuntary separation of 9,000 employees as

described below.

Severance, Pension and Benefit Charges

During 2009, we recorded net pretax severance, pension and benefits

charges of $4,046 million ($2,487 million after-tax). Included in the

charges were net pretax settlement losses of $1,183 million ($719 mil-

lion after-tax) related to employees that received lump-sum distributions,

primarily resulting from our previous separation plans, as prescribed

payment thresholds were reached. Additionally, we recorded net pretax

pension and postretirement curtailment losses of $1,810 million ($1,100

million after-tax) as workforce reductions caused the elimination of a sig-

nificant amount of future service requiring us to recognize a portion of

the prior service costs and actuarial losses. These charges also included

$1,053 million ($668 million after-tax) for planned workforce reductions of

approximately 17,600 employees, 4,200 of which occurred in late 2009.

During 2008, we recorded net pretax severance, pension and benefits

charges of $950 million ($588 million after-tax). These charges primarily

included $586 million ($363 million after-tax) for workforce reductions in

connection with the separation of approximately 8,600 employees and

related charges; 3,500 of whom were separated in the second half of 2008

and the remainder in 2009. Also included are net pretax pension settle-

ments losses of $364 million ($225 million after-tax) related to employees

that received lump-sum distributions, primarily resulting from our separa-

tion plans in which prescribed payment thresholds have been reached.

During the fourth quarter of 2007, we recorded charges of $772 million

($477 million after-tax) primarily in connection with workforce reductions

of 9,000 employees and related charges, 4,000 of whom were separated

in the fourth quarter of 2007 with the remaining reductions occurring

throughout 2008. In addition, we adjusted our actuarial assumptions for

severance to align with future expectations.