American Airlines 2010 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2010 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

72

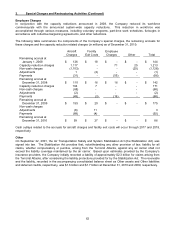

8. Income Taxes (Continued)

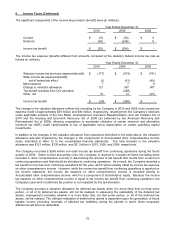

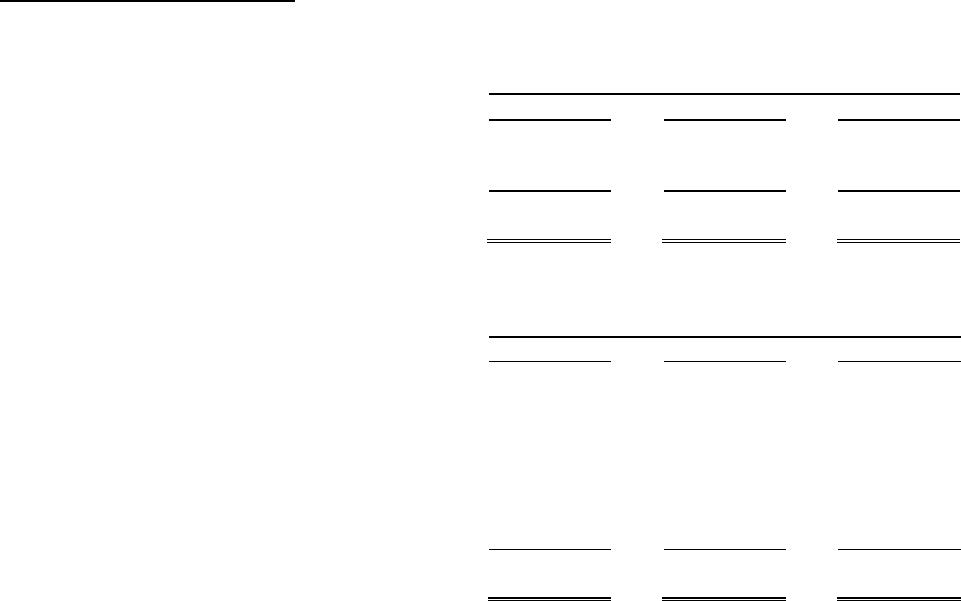

The significant components of the income tax provision (benefit) were (in millions);

Year Ended December 31,

2010

2009

2008

Current

$ (5)

$ (36)

$ 0

Deferred

(30)

(248)

0

Income tax benefit

$ (35)

$ (284)

$ -

The income tax expense (benefit) differed from amounts computed at the statutory federal income tax rate as

follows (in millions):

Year Ended December 31,

2010

2009

2008

Statutory income tax provision expense/(benefit)

$ (177)

$ (613)

$ (741)

State income tax expense/(benefit),

net of federal tax effect

(1)

(41)

(49)

Meal expense

7

7

8

Change in valuation allowance

121

597

807

Tax benefit resulting from OCI allocation

(248)

-

Other, net

15

14

(25)

Income tax benefit

$ (35)

$ (284)

$ -

The change in the valuation allowance reflects the recording by the Company in 2010 and 2009 of an income tax

expense credit of approximately $30 million and $36 million, respectively, resulting from the Company’s elections

under applicable sections of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of

2010 and the Housing and Economic Recovery Act of 2008 (as extended by the American Recovery and

Reinvestment Act of 2009), allowing corporations to accelerate utilization of certain research and alternative

minimum tax (AMT) credit carryforwards in lieu of applicable bonus depreciation on certain qualifying capital

investments.

In addition to the changes in the valuation allowance from operations described in the table above, the valuation

allowance was also impacted by the changes in the components of Accumulated other comprehensive income

(loss), described in Note 12 to the consolidated financial statements. The total increase in the valuation

allowance was $121 million, $135 million, and $2.1 billion in 2010, 2009, and 2008, respectively.

The Company recorded a $248 million non-cash income tax benefit from continuing operations during the fourth

quarter of 2009. Under current accounting rules, the Company is required to consider all items (including items

recorded in other comprehensive income) in determining the amount of tax benefit that results from a loss from

continuing operations and that should be allocated to continuing operations. As a result, the Company recorded a

tax benefit on the loss from continuing operations for the year, which will be exactly offset by income tax expense

on other comprehensive income. However, while the income tax benefit from continuing operations is reported on

the income statement, the income tax expense on other comprehensive income is recorded directly to

Accumulated other comprehensive income, which is a component of stockholders' equity. Because the income

tax expense on other comprehensive income is equal to the income tax benefit from continuing operations, the

Company's year-end net deferred tax position is not impacted by this tax allocation.

The Company provides a valuation allowance for deferred tax assets when it is more likely than not that some

portion, or all of its deferred tax assets, will not be realized. In assessing the realizability of the deferred tax

assets, management considers whether it is more likely than not that some portion, or all of the deferred tax

assets, will be realized. The ultimate realization of deferred tax assets is dependent upon the generation of future

taxable income (including reversals of deferred tax liabilities) during the periods in which those temporary

differences will become deductible.