American Airlines 2010 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2010 American Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

84

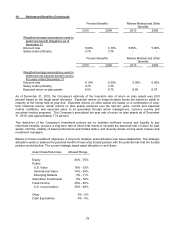

10. Retirement Benefits (Continued)

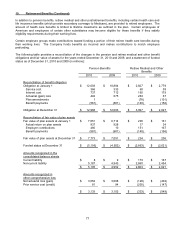

2010

2009

Assumed health care trend rates at

December 31

Health care cost trend rate assumed for

next year

8.0%

7.0%

Rate to which the cost trend rate is

assumed to decline (the ultimate

trend rate)

4.5%

4.5%

Year that the rate reaches the ultimate

trend rate

2018

2015

A one percentage point change in the assumed health care cost trend rates would have the following effects (in

millions):

One Percent

Increase

One Percent

Decrease

Impact on 2010 service and interest cost

22

(22)

Impact on postretirement benefit obligation

as of December 31, 2010

235

(231)

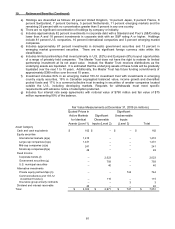

The Company is required to make minimum contributions to its defined benefit pension plans under the minimum

funding requirements of ERISA, the Pension Funding Equity Act of 2004 and the Pension Protection Act of 2006.

The Company estimates its 2011 required contribution to its defined benefit pension plans to be approximately

$520 million under the provisions of these acts which reflects the Preservation of Access to Care for Medical

Beneficiaries and Pension Relief Act of 2010 (the Relief Act), H.R. 3962. The Relief Act provides for temporary,

targeted funding relief (subject to certain terms and conditions) for single employer and multiemployer pension

plans that suffered significant losses in asset value due to the steep market slide in 2008. Under the Relief Act,

the Company’s 2010 minimum required contribution to its defined benefit pension plans was reduced from $525

million to approximately $460 million

The following benefit payments, which reflect expected future service as appropriate, are expected to be paid:

Pension

Retiree Medical

and Other

2011

574

173

2012

602

170

2013

665

169

2014

729

170

2015

785

173

2016 – 2020

4,959

989

During 2008, AMR recorded a settlement charge totaling $103 million related to lump sum distributions from the

Company’s defined benefit pension plans to pilots who retired. Pursuant to U.S. GAAP, the use of settlement

accounting is required if, for a given year, the cost of all settlements exceeds, or is expected to exceed, the sum

of the service cost and interest cost components of net periodic pension expense for a plan. Under settlement

accounting, unrecognized plan gains or losses must be recognized immediately in proportion to the percentage

reduction of the plan's projected benefit obligation.