American Express 2004 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2004 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

The above table reflects only those TRS guarantees that

are within the scope of FIN 45. Expenses relating to

actual claims under these guarantees for 2004 and 2003

were approximately $20 million and $30 million,

respectively. It is not an exhaustive list of all cardmem-

ber guarantee programs, many of which are outside the

scope of FIN 45 as they primarily represent insurance

products issued by Amex Assurance, a wholly-owned

subsidiary of AEFC, and as such are accounted for

under SFAS No. 60, “Accounting and Reporting by

Insurance Enterprises.”

The Company generally has no collateral or other

recourse provisions related to these guarantees. With

respect to merchant protection, the Company’s loss

exposure is mitigated by the Company’s ability to offset

amounts reimbursed to its cardholders against other

amounts due to the Company’s merchants. The

Company may also hold cash back from a merchant.

During the third quarter of 2004, the Company reduced

its merchant-related reserves by approximately

$60 million reflecting changes made to mitigate loss

exposure and ongoing favorable credit experience

with merchants.

The Company, through its AEB operating segment,

provides various guarantees to its customers in the

ordinary course of business that are also within the

scope of FIN 45, including financial letters of credit,

performance guarantees and financial guarantees.

Generally, guarantees range in term from three months

to one year. AEB receives a fee related to these guar-

antees, many of which help to facilitate customer cross-

border transactions. At December 31, 2004, AEB held

$788 million of collateral supporting these guarantees.

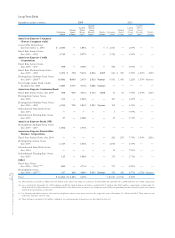

The following table provides information related to

such guarantees as of December 31:

(Millions) 2004 2003

Type of Guarantee

Maximum

amount of

undiscounted

future payments

Amount of

related liability at

December 31, 2004

Maximum

amount of

undiscounted

future payments

Amount of

related liability at

December 31, 2003

Financial letters of credit $ 295 $ 0.4 $ 207 $ 1.1

Performance guarantees 92 1.1 119 0.4

Financial guarantees 554 2.0 629 0.5

Total $ 941 $ 3.5 $ 955 $ 2.0

In addition, the Company had the following other

commitments as of December 31:

(Millions) 2004 2003

Loan commitments and

other lines of credit $662 $770

Bank letters of credit and

other bank guarantees

out of scope of FIN 45 $646 $544

The Company issues commercial and other letters of

credit to facilitate the short-term trade-related needs of

its banking clients, which typically mature within six

months. At December 31, 2004 and 2003, the Company

held $147 million and $114 million, respectively,

of collateral supporting commercial and other letters

of credit.

The Company also has commitments aggregating $176

billion and $156 billion related to its card business in

2004 and 2003, respectively, primarily related to

commitments to extend credit to certain cardmembers

as part of established lending product agreements.

Many of these are not expected to be drawn; therefore,

total unused credit available to cardmembers does not

represent future cash requirements. The Company’s

charge card products have no preset spending limit

and are not reflected in unused credit available

to cardmembers.

During the fourth quarter of 2004, the Company

announced that it signed agreements with Delta Air

Lines to extend its co-brand, Membership Rewards and

merchant partnerships. The agreements will extend

these partnerships into the next decade. As part of the

agreements, the Company committed to prepay $500

million for the future purchase of Delta SkyMiles

rewards points. The prepayment has a three-year term,

is fully collateralized by a pool of assets and is subject

to certain conditions. As of December 31, 2004, the

Company prepaid $250 million of Delta SkyMiles

rewards points, which is reported in other loans on the

Company’s Consolidated Balance Sheet. Under the

terms of the agreements, the Company will prepay the

remaining $250 million of Delta SkyMiles rewards

points in the first quarter of 2005.

In addition, the Company has certain contingent obli-

gations for worldwide business arrangements that

relate to contractual agreements with partners entered

into as part of the ongoing operation of the TRS

AXP

AR.04

106

Notes to Consolidated Financial Statements