American Express 2004 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2004 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

primarily due to merit increases and higher employee

benefit and management incentive costs, partially offset

by the benefits of reengineering efforts.

Total other operating expenses of $5.3 billion increased

6 percent during 2004 primarily due to increases in pro-

fessional fees and occupancy and equipment expenses,

partially offset by the $117 million net gain in connec-

tion with the sale of the equipment leasing product line

noted earlier. The increase in professional fees primarily

reflects the impact of higher business volume-related

technology outsourcing costs. Occupancy and equip-

ment expenses increased primarily due to outsourced

data processing services and increased depreciation of

data processing equipment as well as the impact of the

fourth quarter restructuring charges noted earlier. In

2003, total other operating expenses rose 8 percent to

$4.9 billion due to the impact of greater business and

service volume-related costs, including outsourcing

activities, partially offset by the benefits of reengineer-

ing initiatives and other cost containment efforts.

The effective tax rate was 31 percent in 2004 versus 32

percent in 2003. The effective tax rate was lower in 2004

as compared to 2003 primarily as a result of one-time and

ongoing benefits related to the changes in international

funding strategy during 2004, favorable variances

between estimates of foreign tax expense and returns

actually filed and favorable tax audit experience. The

shifts in international funding strategy, which diversify

funding sources and increase liquidity, are expected also

to benefit TRS’ effective tax rate and net income in future

periods despite somewhat higher related funding costs.

Airline Industry Matters

Historically, the Company has not experienced signifi-

cant revenue declines resulting from a particular air-

line’s scaling-back or closure of operations due to

bankruptcy or other financial challenges because the

volumes generated from the airline are typically shifted

to other participants in the industry that accept the Com-

pany’s card products. Nonetheless, the Company is

exposed to business and credit risk in the airline indus-

try primarily through business arrangements where the

Company has remitted payment to the airline for a card-

member purchase of tickets that have not yet been used

or “flown”. This creates a potential exposure for the

Company in the event that the cardmember is not able

to use the ticket and the Company, based on the facts

and circumstances, credits the cardmember for the

unused ticket. Historically, this type of exposure has not

generated any significant losses for the Company

because of the need for an airline that is operating under

bankruptcy protection to continue accepting credit and

charge cards and honoring requests for credits and

refunds in the ordinary course in furtherance of its reor-

ganization and its formal assumption, with bankruptcy

court approval, of its card acceptance agreement,

including approval of the Company’s right to hold cash

to cover these potential exposures to provide credits to

cardmembers. Typically, as an airline’s financial situa-

tion deteriorates the Company increases cash held to

protect itself in the event of an ultimate liquidation of

the airline. The Company’s goal in these distressed situ-

ations is to hold sufficient cash over time to ensure that

upon liquidation the cash held is equivalent to the credit

exposure related to any unused tickets.

Liquidity and Capital Resources

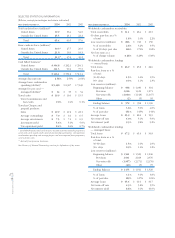

SELECTED BALANCE SHEET INFORMATION (GAAP BASIS)

December 31, (Billions, except percentages) 2004 2003

Accounts receivable, net $ 31.8 $ 30.2

Travelers Cheque investments $ 8.4 $ 7.7

Cardmember loans $ 26.9 $ 25.8

Total assets $ 87.8 $ 79.3

Travelers Cheques outstanding $ 7.3 $ 6.8

Short-term debt $ 17.2 $ 21.8

Long-term debt $ 28.3 $ 16.6

Total liabilities $ 79.0 $ 71.4

Total shareholder’s equity $ 8.8 $ 7.9

Return on average total

shareholder’s equity 33.4% 31.3%

Return on average total assets 3.5% 3.4%

See Glossary of Selected Terminology section for definitions of key terms.

Net accounts receivable and worldwide cardmember

loans increased as compared to December 31, 2003, pri-

marily as a result of higher average cardmember spend-

ing and an increase in the number of cards-in-force.

Total debt increased compared to December 31, 2003

primarily as a result of increased funding requirements

due to the noted increases in cardmember receivable

and loan balances as well as the contingent liquidity

program discussed below. New long-term borrowing

activity during 2004 is described below.

Financing Activities

TRS funds its cardmember receivables and loans using

various funding sources, such as short- and long-term

debt, medium-term notes, and sales of cardmember

receivables and loans in securitizations. In 2004 and

2003, TRS had uninterrupted access to the money and

capital markets to fund its business operations.

TRS funds its receivables and loans primarily through

five entities. Credco finances the vast majority of card-

member receivables, while Centurion Bank and FSB

AXP

AR.04

51

Financial Review