American Express 2004 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2004 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

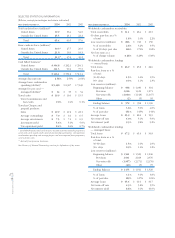

TRAVEL RELATED SERVICES

Results of Operations

STATEMENTS OF INCOME

Years Ended December 31, (Millions) 2004 2003 2002

Net revenues:

Discount revenue $ 10,249 $ 8,781 $ 7,931

Lending:

Finance charge revenue 2,795 2,525 2,338

Interest expense 571 483 510

Net finance charge

revenue 2,224 2,042 1,828

Net card fees 1,909 1,835 1,726

Travel commissions

and fees 1,795 1,507 1,408

Other commissions

and fees 2,230 1,901 1,833

Travelers Cheque

investment income 378 367 375

Securitization income, net 1,132 1,105 1,049

Other 1,661 1,651 1,571

Total net revenues 21,578 19,189 17,721

Expenses:

Marketing, promotion,

rewards and

cardmember services 4,944 3,814 3,027

Provision for losses

and claims:

Charge card 833 853 960

Lending 1,130 1,218 1,369

Other 176 127 149

Total 2,139 2,198 2,478

Charge card interest

expense 713 786 1,001

Human resources 4,389 3,822 3,503

Other operating expenses:

Professional services 2,101 1,958 1,693

Occupancy and

equipment 1,300 1,199 1,102

Communications 465 452 443

Other 1,410 1,389 1,394

Total other operating

expenses 5,276 4,998 4,632

Total expenses 17,461 15,618 14,641

Pretax income 4,117 3,571 3,080

Income tax provision 1,265 1,141 945

Net income $ 2,852 $ 2,430 $ 2,135

See Glossary of Selected Terminology section for definitions of key terms.

TRS reported net income of $2.9 billion in 2004, a 17

percent increase from $2.4 billion in 2003, which

increased 14 percent from 2002.

The quality of TRS’ card customer base, the breadth of

its product portfolio, the benefits of its reward-based,

spend oriented business model and its improved

revolving credit capabilities combined to create a com-

petitive advantage that was leveraged effectively to

deliver strong TRS results. The Company’s continued

investments in growth initiatives over the past several

years have resulted in strong growth in cardmember

spending in the retail and everyday spending catego-

ries and continued improvement in the travel and

entertainment sector, significant increases in cards-in-

force from expansion of both proprietary and network

card businesses, and quality lending balance growth.

See Executive Overview for a general discussion of

TRS’ businesses and operations.

TRS’ owned portfolio is primarily comprised of card-

member receivables generated by the Company’s

charge card products, unsecuritized U.S. cardmember

loans and international cardmember loans.

As discussed more fully in the TRS Liquidity and Capital

Resources section below, the Company securitizes

U.S. cardmember loans as part of its financing strat-

egy; consequently, the level of unsecuritized U.S.

cardmember loans is primarily a function of the

Company’s financing requirements. As a portfolio,

unsecuritized U.S. cardmember loans tend to be less

seasoned than securitized loans, primarily because of

the lead time required to designate and securitize

each loan. The Company does not currently securitize

international loans. Delinquency, reserve coverage

and net write-off rates have historically been broadly

comparable between the Company’s owned and man-

aged portfolios.

The following management discussion includes infor-

mation on both a GAAP basis and managed basis. The

Company presents TRS information on a managed

basis because that is the way the Company’s manage-

ment views and manages the business. It differs from

the accompanying financial statements, which are pre-

pared in accordance with GAAP, as managed basis pre-

sentation assumes there have been no securitization

transactions, i.e., as if all securitized cardmember loans

and related income effects are reflected in the Compa-

ny’s balance sheet and income statement, respectively.

Management believes that the trends in the Company’s

cardmember lending business are more accurately por-

trayed by evaluating the performance of both securi-

tized and non-securitized cardmember loans. Asset

securitization is just one of several ways the Company

funds cardmember loans. Use of a managed basis pre-

sentation, including non-securitized and securitized

cardmember loans, presents a more accurate picture of

the key dynamics of the cardmember lending business,

avoiding distortions due to the mix of funding sources

AXP

AR.04

45

Financial Review