American Express 2004 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2004 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

help ensure the availability of financing in unexpected

periods of stress, and to be concurrently integrated into

the asset-liability management of interest rate exposures.

Liquidity refers to the Company’s ability to meet its cur-

rent and future cash needs. In addition to its funding plan

described below, the Company’s contingent funding

strategy is designed to allow for the continued funding

of business operations through difficult economic, finan-

cial market and business conditions when access to its

regular funding sources could become diminished

or interrupted.

TRS is the primary asset generating business with sig-

nificant assets in both domestic and international card-

member receivable and lending activities. As such, the

Company’s most significant borrowing and liquidity

needs are associated with TRS’ card businesses. TRS

pays merchants for card transactions and bills card-

members accordingly. TRS funds merchant payments

during the period cardmember loans and receivables

are outstanding. AEFA’s borrowing needs are less sig-

nificant as it generates funds through its operations, pri-

marily by the sale of insurance, annuity or certificate

products. AEB also has limited borrowing needs as its

principal funding source is customer deposits. See the

Liquidity and Capital Resources section for TRS, AEFA

and AEB for further discussion regarding each operat-

ing segment’s funding activities and liquidity manage-

ment practices.

The following discussion includes information on both

a GAAP and managed basis. The managed basis presen-

tation includes debt issued in connection with the

Company’s lending securitization activities, which are

off-balance sheet. The Company’s management views

and manages funding requirements on a managed basis

because asset securitization is just one of several ways

for the Company to fund cardmember loans. Use of a

managed basis presentation, including both on- and off-

balance sheet debt, avoids distortions due to the mix of

funding sources at any particular point in time.

Funding Strategy

The Company’s funding sources are well-diversified

and include commercial paper, retail and institutional

customer deposits, bank notes, medium-term notes,

senior debt, asset securitizations and other borrowed

funds. Diversity of funding sources by debt instrument

and by investor base provides additional insulation

from unforeseen events in the short-term debt market.

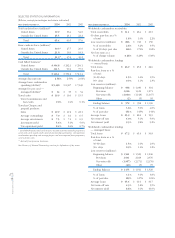

The Company had the following consolidated debt, on

both a GAAP and managed basis, and customer depos-

its outstanding at December 31, 2004 and 2003:

December 31, (Billions) 2004 2003

Short-term debt $ 14.2 $ 19.0

Long-term debt 33.0 20.7

Total debt (GAAP basis) $ 47.2 $ 39.7

Off-balance sheet securitizations

(a)

20.3 19.5

Total debt (managed basis) $ 67.5 $ 59.2

Customer deposits $ 21.1 $ 21.3

(a) Includes securitized equipment leasing receivables of $0.1 billion at

December 31, 2003.

In addition to deposits and debt, the Company uses off-

balance sheet arrangements, principally through the

sales of consumer cardmember loans in securitizations.

In 2004, the Company securitized $3.9 billion in loans

from its consumer loans portfolio while $3.0 billion

of investor interests matured. As of December 31, 2004

and 2003, the Company, through a lending securitiza-

tion trust, held total assets of $24.7 billion and $26.8

billion, respectively, of which $20.3 billion and $19.4

billion, respectively, had been sold.

Additionally, the Company had securitized cardmem-

ber receivables of $7.4 billion at December 31, 2004

of which $1.9 billion had been sold. All securitized

cardmember receivables remain on the Consolidated

Balance Sheet.

In 2004, the Company continued to reduce its reliance

on short-term debt. Term debt offerings of $15.2 billion

in 2004 were issued to refinance maturing long-term

obligations, fund business growth and decrease short-

term debt obligations.

December 31, ($ in billions) 2004 2003

Short-term debt $14.2 $19.0

Short-term debt percentage

of total debt (GAAP basis) 30.0% 48.0%

Short-term debt percentage

of total debt (managed basis) 21.0% 32.2%

In 2004, medium- and long-term debt with maturities

ranging from 2 to 5 years was issued. The Company’s

2004 term offerings, which include those made by the

Parent Company; American Express Credit Corpora-

tion (Credco), American Express Centurion Bank (Cen-

turion Bank), and American Express Bank, FSB (FSB),

all wholly-owned subsidiaries of TRS; and the Ameri-

can Express Credit Account Master Trust, are presented

in the following table on a managed basis:

AXP

AR.04

38

Financial Review