American Express 2004 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2004 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

at any particular point in time. For example, irrespec-

tive of the mix, it is important for management and

investors to see metrics, such as changes in delinquen-

cies and write-off rates, for the entire cardmember

lending portfolio because it is more representative of

the economics of the aggregate cardmember relation-

ships and ongoing business performance and trends

over time. It is also important for investors to see the

overall growth of cardmember loans and related rev-

enue and changes in market share, which are signifi-

cant metrics in evaluating the Company’s performance

and which can only be properly assessed when all

non-securitized and securitized cardmember loans are

viewed together on a managed basis. Asset securitiza-

tion activity of the Company is discussed in detail in the

TRS Liquidity and Capital Resources section.

On a GAAP basis, results reflect finance charge revenue

on the owned loan portfolio as well as finance charge

revenue on the retained seller’s interest from securiti-

zation activity. GAAP basis results also include invest-

ment income on the Company’s investments in other

subordinated retained interests from loan securitiza-

tion issuances.

Additionally, on a GAAP basis, results reflect net secu-

ritization income, which is comprised of the non-credit

provision components of the net gains and charges

from securitization activities, excess spread related to

securitized loans, net finance charge revenue on

retained interests in securitized loans, and servicing

income, net of related discounts or fees. Excess spread,

which is the net positive cash flow from interest and fee

collections allocated to the investor’s interests after

deducting the interest paid on investor certificates,

credit losses, contractual servicing fees and other

expenses is recognized in securitization income as it is

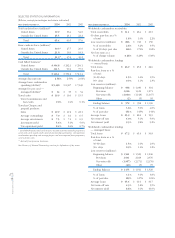

earned. Net securitization income of $1.1 billion

increased slightly in 2004 compared to 2003 as the

impact of higher average securitized loan balances was

partially offset by lower net gains from securitization

activities. Net securitization income increased 5

percent to $1.1 billion in 2003 primarily as a result of

a higher average balance of cardmember lending secu-

ritizations. See Selected Statistical Information below

for data relating to TRS’ owned loan portfolio.

During the years ended December 31, 2004, 2003 and

2002, TRS recognized net gains of $26 million ($17 mil-

lion after-tax), $124 million ($81 million after-tax) and

$136 million ($88 million after-tax), respectively, from

net securitization activities. For the year ended

December 31, 2004, the net gains consist of $230 mil-

lion of income from the sale of $1.4 billion of certain

subordinated retained interests and the securitization

of $3.9 billion of cardmember loans, including the

impact of the related credit reserves on the sold loans.

This amount is partially offset by $204 million of

charges related to the maturity of $3.0 billion of previ-

ously outstanding issuances, changes in interest-only

strip assumptions and a current year reconciliation

adjustment to lending receivable accounts. For the year

ended December 31, 2003, $3.5 billion of U.S. lending

receivables were securitized and $1.0 billion of securi-

tization transactions matured.

Management views any net gains from securitizations

as discretionary benefits to be used for card acquisition

expenses, which are reflected in both marketing, pro-

motion, rewards and cardmember services and other

operating expenses. Consequently, the managed basis

presentation for the years ended December 31, 2004,

2003 and 2002 assumes that the impact of this net activ-

ity was offset by higher marketing, promotion, rewards

and cardmember services expenses of $16 million,

$74 million and $81 million, respectively, and other

operating expenses of $10 million, $50 million and

$55 million, respectively. Accordingly, the incremental

expenses, as well as the impact of this net activity, have

been eliminated.

The following tables reconcile the GAAP basis for cer-

tain TRS income statement line items to the managed

basis information, where different.

AXP

AR.04

46

Financial Review