American Express 2004 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2004 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

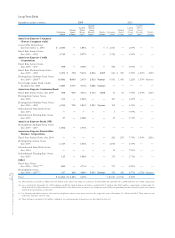

Note 4 SECURITIZED LOANS

The Company periodically securitizes pools of its card-

member loans through the American Express Credit

Account Master Trust (the Lending Trust), which in turn

sells securities collateralized by the transferred card-

member loans to third-party investors. Such securities

represent undivided interests in the transferred card-

member loans. The Company is required to maintain

an undivided interest in the transferred cardmember

loans, which is referred to as seller’s interest and is

reported as loans on the Company’s Consolidated Bal-

ance Sheets. Any billed finance charges related to the

transferred cardmember loans are reported as other

receivables on the Company’s Consolidated Balance

Sheets. The Company retains servicing responsibilities

for the transferred assets and earns a related fee. Pur-

suant to SFAS No. 140, no servicing asset or liability is

recognized at the time of a securitization, as manage-

ment believes that the Company receives adequate

compensation relative to current market servicing fees.

As of December 31, 2004 and 2003, the Lending Trust

held total assets of $24.7 billion and $26.8 billion,

respectively, of which $20.3 billion and $19.4 billion

had been sold.

The Company also retains subordinated interests in the

securitized cardmember loans. Such subordinated

retained interests include one or more investments in

tranches of the securitization and an interest-only strip.

The investments in the tranches of the securitization are

accounted for at fair value as Available-for-Sale invest-

ment securities in accordance with SFAS No. 115 and

are reported in investments on the Company’s Consoli-

dated Balance Sheets. As of December 31, 2004 and

2003, the ending fair value of these subordinated

retained interests was $0.1 billion and $1.8 billion,

respectively, reflecting the sale of $1.4 billion of sub-

ordinated retained interests to third parties during

2004. The interest-only strip is also accounted for at fair

value consistent with a SFAS No. 115 Available-for-Sale

investment but is reported in other assets on the Com-

pany’s Consolidated Balance Sheets. The fair value of

the interest-only strip is the present value of estimated

future excess spread expected to be generated by the

securitized loans over the estimated life of those loans.

Excess spread, which is the net positive cash flow from

interest and fee collections allocated to the investors’

interests after deducting the interest paid on investor

certificates, credit losses, contractual servicing fees and

other expenses, is recognized in securitization income

as it is earned. As of December 31, 2004 and 2003, the

fair value of the interest-only strip was $207 million and

$225 million, respectively.

At the time of a cardmember loan securitization, the

Company typically records a gain on sale, which is cal-

culated as the difference between the proceeds from

the sale and the book basis of the cardmember loans

sold. That book basis on sold cardmember loans is

determined by allocating the carrying amount of the

cardmember loans, net of applicable credit reserves,

between the cardmember loans sold and the interests

retained based on their relative fair values. Such fair

values are based on market prices at date of transfer for

the sold cardmember loans and on the estimated

present value of future cash flows for retained interests.

Gains on sale from securitizations are reported in secu-

ritization income on the Company’s Consolidated

Statements of Income, except for the component

resulting from the release of credit reserves upon sale,

which is reported as a reduction of provision for losses

from cardmember lending. Securitization transaction

costs are offset against the gains on sales at the time of

the transaction.

During 2004, 2003 and 2002, the Company sold $3.9

billion, $3.5 billion and $4.6 billion, respectively, of

cardmember loans, or $3.9 billion, $3.1 billion and

$4.2 billion, respectively, net of the Company’s invest-

ments in subordinated retained interests. Additionally,

during 2004, 2003 and 2002, $3.0 billion, $1.0 billion

and $2.0 billion, respectively, of securities issued to

investors from the Lending Trust matured. The pretax

net gains on sale from securitizations, including the sale

of subordinated retained interests, net of the impact of

maturities, the effect of changes in interest-only strip

valuation factors and a reconciliation adjustment

charge were $26 million, $124 million and $136 million,

respectively, for 2004, 2003 and 2002.

AXP

AR.04

97

Notes to Consolidated Financial Statements