American Express 2004 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2004 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

principally fund cardmember loans originated from

the Company’s lending activities. In addition, two trusts

are used by the Company in connection with the

securitization and sale of receivables and loans gener-

ated in the ordinary course of TRS’ card businesses. The

assets securitized consist principally of U.S. consumer

cardmember receivables and loans arising from TRS’

charge card and lending activities.

TRS’ funding needs are met primarily through the fol-

lowing sources:

©Commercial paper,

©Bank notes, institutional CDs and Fed Funds,

©Medium-term notes and senior unsecured debentures,

©Asset securitizations, and

©Long-term committed bank borrowing facilities in

selected non-U.S. markets.

TRS’ debt offerings are placed either directly, as in the

case of its commercial paper program through Credco,

or through securities brokers or underwriters. In certain

international markets, bank borrowings are used to par-

tially fund cardmember receivables and loans. During

2004, TRS diversified its funding base by borrowing

under committed bank credit facilities as part of a

change in local funding strategies in select international

markets.

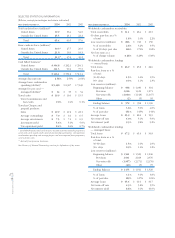

The following table highlights TRS’ outstanding debt

(including intercompany balances) and off-balance

sheet securitizations as of December 31, 2004 and 2003:

December 31, (Billions) 2004 2003

Short-term debt $17.2 $21.8

Long-term debt 28.3 16.6

Total debt (GAAP basis) $45.5 $38.4

Off-balance sheet securitizations

(a)

20.3 19.5

Total debt (managed basis) $65.8 $57.9

(a) Includes securitized equipment leasing receivables of $0.1 billion at

December 31, 2003.

Short-term debt is defined as any debt with an original

maturity of 12 months or less. The commercial paper

market represents the primary source of short-term fund-

ing for the Company. Credco’s commercial paper is a

widely recognized name among short-term investors

and is a principal source of debt for the Company. At

December 31, 2004, Credco had $3.8 billion of commer-

cial paper outstanding, net of certain short-term invest-

ments. The outstanding amount, net of certain short-term

investments, declined $5.0 billion or 57 percent from a

year ago primarily as a result of a change in Credco’s

funding strategy in certain international markets. Average

commercial paper outstanding, net of certain short-term

investments, was $5.7 billion and $7.7 billion in 2004 and

2003, respectively. TRS currently manages the level of

commercial paper outstanding, net of certain short-term

investments, such that the ratio of its committed bank

credit facility to total short-term debt, which consists

mainly of commercial paper, is not less than 100%.

Centurion Bank and FSB raise short-term debt through

various instruments. Bank notes issued and Fed Funds

purchased by Centurion Bank and FSB totaled approxi-

mately $5.2 billion as of December 31, 2004. Centurion

Bank and FSB also raise customer deposits through the

issuance of certificates of deposits to retail and institu-

tional customers. As of December 31, 2004, Centurion

Bank and FSB held $4.5 billion in customer deposits.

Centurion Bank and FSB maintain $320 million and

$300 million, respectively, of committed bank credit

lines as a backup to short-term funding programs. Long-

term funding needs are met principally through the sale

of cardmember loans in securitization transactions. The

Asset/Liability Committees of Centurion Bank and FSB

provide management oversight with respect to formu-

lating and ratifying funding strategy and to ensuring that

all funding policies and requirements are met.

Medium- and long-term debt is raised through the offer-

ing of debt securities in the U.S. and international capital

markets. Medium-term debt is generally defined as any

debt with an original maturity greater than 12 months

but less than 36 months. Long-term debt is generally

defined as any debt with an original maturity greater

than 36 months. At December 31, 2004, TRS and its sub-

sidiaries had the following amounts of medium- and

long-term debt outstanding (including intercompany

balances):

December 31, 2004

(Billions)

Medium-term

Debt

Long-term

Debt

Total Medium-

and Long-term,

Debt

Credco $12.2 $6.4 $18.6

Centurion Bank 3.0 1.4 4.4

FSB 1.6 — 1.6

Other Subsidiaries 1.7 2.0 3.7

Total TRS $18.5 $9.8 $28.3

In 2005, TRS along with its subsidiaries, Credco, Centu-

rion Bank and FSB, as well as through its securitization

trusts, expects to issue approximately $13 billion in

medium- and long-term debt to fund business growth

and refinance a portion of maturing medium- and long-

term debt. The Company expects that its planned fund-

ing during the next year will be met through a combi-

nation of sources similar to those on which it currently

relies. However, the Company continues to assess its

AXP

AR.04

52

Financial Review