Cabela's 2010 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2010 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

36

more stringent capital, liquidity, and leverage ratio requirements, increase FDIC deposit insurance premiums,

or otherwise adversely affect WFB’s business. These changes may also require WFB to invest significant

management attention and resources to evaluate and make necessary changes.

As a result of the recent accounting guidance on consolidations and the accounting for transfers of financial

assets and the criteria for determining whether to consolidate a variable interest entity, there was uncertainty

over FDIC guidance regarding the safe-harbor for legal isolation of transferred assets provided by FDIC Rule 12

C.F.R. 360.6 “Treatment by the Federal Deposit Insurance Corporation as Conservator or Receiver of Financial

Assets Transferred by an Insured Depository Institution in Connection With a Securitization or Participation.”

In March 2010, the FDIC announced an interim amendment of this regulation. Under the interim amendment, the

legal isolation of property transferred in a securitization transaction prior to September 30, 2010, was preserved,

regardless of whether the transfer qualified for sale accounting treatment under new accounting standards if the

transfer otherwise complied with the FDIC’s regulation. On September 27, 2010, the FDIC approved a final rule

that, subject to certain conditions, preserves the safe-harbor treatment applicable to certain grandfathered revolving

trusts and master trusts that had issued at least one series of asset-backed securities as of such date, which we

believe includes the Trust. The final rule imposes significant new conditions on the availability of the safe-harbor

with respect to securitizations that are not grandfathered.

Several rules and regulations have recently been proposed or adopted that may substantially affect issuers

of asset-backed securities. On April 7, 2010, the SEC issued proposed rules that will significantly change the

offering process, disclosure, and reporting for asset-backed securities. Pursuant to the provisions of the Reform

Act, on January 20, 2011, the SEC adopted rules that require issuers of asset-backed securities to disclose demand,

repurchase, and replacement information through the periodic filing of a new form with the SEC. These rules

also require rating agencies to disclose in any report accompanying a credit rating for an asset-backed security the

representations, warranties, and enforcement mechanisms available to investors and how they differ from those in

similar securities. Also pursuant to the provisions of the Reform Act, on January 20, 2011, the SEC issued rules that

require issuers of registered asset-backed securities to perform a review of the assets underlying the securities and

to publicly disclose information relating to the review. These rules also require issuers of asset-backed securities to

make publicly available the findings and conclusions of any third-party due diligence report obtained by the issuer.

It remains to be seen whether and to what extent the January 20, 2011, rules or any other final rules adopted by the

SEC will impact WFB and its ability and willingness to continue to rely on the securitization market for funding.

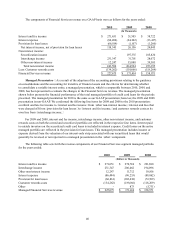

Impact of New Accounting Pronouncements – The accounting guidance on consolidations and accounting

for transfers of financial assets and the criteria for determining whether to consolidate a variable interest entity

resulted in the consolidation of the Trust effective January 3, 2010. Consequently, there was a material impact on

our total assets, total liabilities, retained earnings and other comprehensive income, statement of cash flows, and

the components of our Financial Services revenue. The consolidation of the Trust eliminated retained interests

in securitized loans and required the establishment of an allowance for loan losses on the securitized credit card

loans. The credit card loans of the Trust are recorded as restricted credit card loans and the liabilities of the Trust

are recorded as secured borrowings. The secured borrowings still contain the legal isolation requirements which

would protect the assets pledged as collateral for the securitization investors as well as protecting Cabela’s and

WFB from any liability from default on the notes. The Trust was consolidated on January 3, 2010, resulting in an

increase in total assets and liabilities of $2.15 billion and $2.25 billion, respectively, and retained earnings and

other comprehensive income decreasing $93 million, after tax.

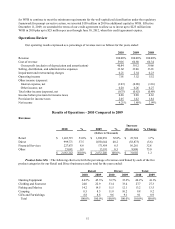

In 2010, we began reporting the results of operations of our Financial Services business in a manner similar

to our historical managed presentation for financial performance of the total managed portfolio of credit card loans,

excluding income derived from the changes in the valuation of our interest-only strip, cash reserve accounts, and

cash accounts associated with the securitized loans.

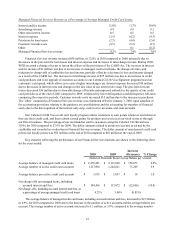

At the beginning of 2010, WFB’s required capital was increased under regulatory capital requirements of the

applicable federal agencies as a result of new accounting standards which required the consolidation of the assets

and liabilities of the Trust on WFB’s balance sheet. As of December 31, 2010, the most recent notification from the

FDIC categorized WFB as well-capitalized under the regulatory framework for prompt corrective action. In order