Cabela's 2010 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2010 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

63

Recent Accounting Standards and Pronouncements

In January 2010, the Financial Accounting Standards Board (“FASB”) issued ASU No. 2010-06, Fair

Value Measurements and Disclosures (Topic 820): Improving Disclosures about Fair Value Measurements. This

guidance revises two disclosure requirements concerning fair value measurements and clarifies two others. This

statement requires separate presentation of significant transfers into and out of Levels 1 and 2 of the fair value

hierarchy and disclosure of the reasons for such transfers. It will also require the presentation of purchases, sales,

issuances, and settlements within Level 3 on a gross basis rather than a net basis. The amendments also clarify that

disclosures should be disaggregated by class of asset or liability and that disclosures about inputs and valuation

techniques should be provided for both recurring and non-recurring fair value measurements. The new disclosures

about fair value measurements are presented in Note 25 to our consolidated financial statements, except for the

requirement concerning gross presentation of Level 3 activity, which is effective for fiscal years beginning after

December 15, 2010. The adoption of this statement had no effect on our financial position or results of operations.

In July 2010, the FASB issued ASU No. 2010-20, Disclosures about the Credit Quality of Financing

Receivables and the Allowance for Credit Losses. This guidance enhances the existing disclosure requirements

providing more transparency of the allowance for loan losses and credit quality of financing receivables. The new

disclosures that relate to information as of the end of a reporting period are effective for our fiscal 2010 year-end

reporting and are presented in Notes 1 and 4 to our consolidated financial statements. The new disclosures that

relate to activity occurring during the reporting period will be effective beginning with our first quarter of fiscal

2011.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We are exposed to interest rate risk through WFB’s operations and, to a lesser extent, through our

merchandising operations. We also are exposed to foreign currency risk through our merchandising operations.

Financial Services Interest Rate Risk

Interest rate risk refers to changes in earnings due to interest rate changes. To the extent that interest income

collected on credit card loans and interest expense on certificates of deposit and secured borrowings do not respond

equally to changes in interest rates, or that rates do not change uniformly, earnings could be affected. The variable

rate credit card loans are indexed to the one month London Interbank Offered Rate (“LIBOR”) and the credit card

portfolio is segmented into risk-based pricing tiers each with a different interest margin. Variable rate secured

borrowings are indexed to LIBOR-based rates of interest and are periodically repriced. Certificates of deposit and

fixed rate secured borrowings are priced at the current prevailing market rate at the time of issuance. We manage

and mitigate our interest rate sensitivity through several techniques, but primarily by indexing the customer rates

to the same index as our cost of funds. Additional techniques we use include managing the maturity, repricing, and

mix of fixed and variable assets and liabilities by issuing fixed rate secured borrowings or certificates of deposit

and entering into interest rate swaps.

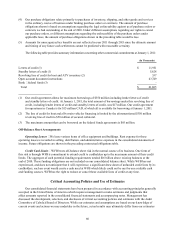

The table below shows the mix of our credit card account balances at the years ended:

2010 2009 2008

As a percentage of total balances outstanding:

Balances carrying an interest rate based upon various

interest rate indices 61.9%65.2%66.1%

Balances carrying an interest rate of 9.99% 3.9 2.5 1.9

Balances carrying an interest rate of 0.00% 0.2 0.6 1.3

Balances not carrying interest because their previous

month’s balance was paid in full 34.0 31.7 30.7

100.0%100.0%100.0%