Cabela's 2010 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2010 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

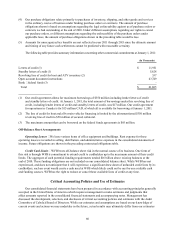

50

estimates the gross amount of principal that will be charged off over of the next twelve months, net of recoveries.

This estimate is used to derive an estimated allowance. In addition to these methods of measurement, management

also considers other factors such as general economic and business conditions affecting key lending areas, credit

concentration, changes in origination and portfolio management, and credit quality trends. Since the evaluation

of the inherent loss with respect to these factors is subject to a high degree of uncertainty, the measurement of

the overall allowance is subject to estimation risk, and the amount of actual losses can vary significantly from the

estimated amounts.

Charge-offs consist of the uncollectible principal, interest, and fees on a customer’s account. Recoveries are

the amounts collected on previously charged-off accounts. Most bankcard issuers charge off accounts at 180 days.

We charge off credit card loans on a daily basis after an account becomes at a minimum 130 days contractually

delinquent to allow us to manage the collection process more efficiently. Accounts relating to cardholder

bankruptcies, cardholder deaths, and fraudulent transactions are charged off earlier. WFB records charged-off

cardholder fees and accrued interest receivable directly against interest and fee income included in Financial

Services revenue.

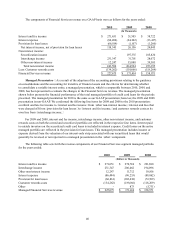

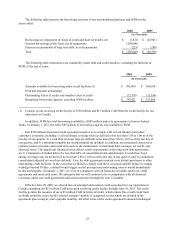

The following chart shows the activity in our allowance for loan losses and charge off activity for the

years ended:

2010 2009 2008

(Dollars in Thousands)

Balance, beginning of period $ 1,374 $1,507 $1,197

Change in allowance for loan losses upon consolidation

of the Trust 114,573 - -

115,947 1,507 1,197

Provision for loan losses 66,814 1,107 1,260

Charge-offs (108,111)(1,429)(1,193)

Recoveries 16,250 189 243

Net charge-offs (91,861)(1,240)(950)

Balance, end of period $ 90,900 $1,374 $1,507

Net charge-offs on securitized credit card loans $ - $ (99,876) $ (50,786)

Net charge-offs on credit card loans (91,861)(1,240)(950)

Charge-offs of accrued interest and fees (recorded as a

reduction in interest and fee income) (12,555)(15,956)(9,712)

Total net charge-offs including accrued interest and fees $ (104,416) $ (117,072) $ (61,448)

Net charge-offs including accrued interest and fees as a

percentage of average managed credit card loans 4.23%5.06%2.95%

For 2010, net charge-offs as a percentage of average managed credit card loans decreased to 4.23%, down 83

basis points compared to 5.06% for 2009. We believe our charge-off levels remain well below industry averages.

Our net charge-off rates and allowance for loan losses have decreased due to improved outlooks in the quality

of our credit card portfolio evidenced by lower delinquencies and delinquency roll-rates and favorable charge-

off trends.

Aging of Credit Cards Loans Outstanding

The quality of our managed credit card loan portfolio at any time reflects, among other factors: 1) the

creditworthiness of cardholders, 2) general economic conditions, 3) the success of our account management

and collection activities, and 4) the life-cycle stage of the portfolio. During periods of economic weakness,

delinquencies and net charge-offs are more likely to increase. We have mitigated periods of economic weakness by

selecting a customer base that is very creditworthy. The median FICO scores of our credit cardholders were 790 at

the end of 2010 compared to 787 at the end of 2009.