Cabela's 2010 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2010 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

81

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

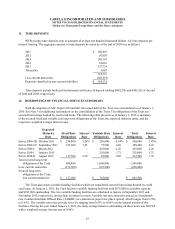

The following table presents the components of the consolidated assets and liabilities of the Trust at

January 1, 2011:

Consolidated assets:

Restricted credit card loans, net of allowance of $90,100 $ 2,685,668

Restricted cash 18,575

Total $2,704,243

Consolidated liabilities:

Secured variable funding obligations $ 393,000

Secured long-term obligations 1,590,900

Interest due to third party investors 2,336

Total $1,986,236

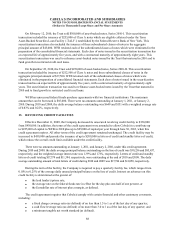

4. CREDIT CARD LOANS AND ALLOWANCE FOR LOAN LOSSES

WFB grants individual credit card loans to its customers and is diversified in its lending with borrowers

throughout the United States. With the adoption of ASC Topics 810 and 860, the securitized credit card loans of the

Trust were consolidated as restricted credit card loans as of January 3, 2010. See Note 3 for additional information

on the consolidation of the Trust and a summary of the credit card loans as of January 2, 2010. The following table

reflects the credit card loans at January 1, 2011:

Credit card loans:

Restricted credit card loans of the Trust (1) $ 2,775,768

Unrestricted credit card loans 24,444

Total credit card loans 2,800,212

Allowance for loan losses (90,900)

Credit card loans, net $ 2,709,312

(1) Restricted credit card loans are restricted for repayment of secured borrowings of the Trust.

The allowance for loan losses is intended to cover losses inherent in WFB’s loan portfolio as of the reporting

date. The following table reflects the activity in the allowance for loan losses for the years ended:

2010 2009 2008

Balance, beginning of year $ 1,374 $1,507 $1,197

Change in allowance upon adoption of ASC Topics 810 and 860 114,573 - -

115,947 1,507 1,197

Provision for loan losses 66,814 1,107 1,260

Charge-offs (108,111)(1,429)(1,193)

Recoveries 16,250 189 243

Net charge-offs (91,861)(1,240)(950)

Balance, end of year $ 90,900 $1,374 $1,507

WFB segments the loan portfolio into loans that have been restructured and other credit card loans in order to

facilitate the estimation of the losses inherent in the portfolio as of the reporting date. WFB uses the scores of Fair

Isaac Corporation (“FICO”), a widely-used tool for assessing an individual’s credit rating, as the primary credit