Cabela's 2010 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2010 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

82

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

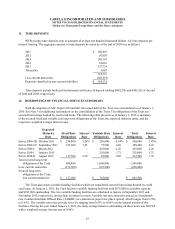

quality indicator. The FICO score is an indicator of quality, with the risk of loss increasing as an individual’s FICO

score decreases. The credit card loan segment was disaggregated into the following classes based upon the loan’s

current related FICO score: 679 and below, 680-749, and 750 and above. WFB considers a loan to be delinquent

if the minimum payment is not received by the payment due date. The aging method is based on the number of

completed billing cycles during which a customer has failed to make a required payment.

The table below provides a summary of loans by class using the fourth quarter FICO score at January 1, 2011:

FICO Score of Credit Card Loans Segment

Restructured

Credit Card

Loans

Segment (1) Total679 and Below 680-749 750 and Above

Credit card loan status:

Current $353,937 $864,791 $1,445,446 $69,521 $2,733,695

30-59 days past due 13,645 8,267 7,127 7,740 36,779

60-89 days past due 5,775 1,044 240 4,111 11,170

90 or more days past due 11,504 460 53 6,551 18,568

Total past due 30,924 9,771 7,420 18,402 66,517

Total credit card loans $ 384,861 $874,562 $1,452,866 $87,923 $2,800,212

90 days or more past due and

still accruing $ 11,504 $460 $53 $6,160 $18,177

Non-accrual - - - 6,629 6,629

(1) Specific allowance for loan losses of $38,913 is included in total allowance for loan losses.

5. CREDIT CARD LOANS AND SECURITIZATION PRIOR TO CONSOLIDATION OF THE TRUST

Prior to the adoption of ASC Topics 810 and 860 and the consolidation of the Trust on January 3, 2010, the

securitizations qualified as sales under GAAP; therefore, the Trust was excluded from the consolidated financial

statements in accordance with GAAP. Accordingly, the credit card loans equal to the investor interest and the

securitization notes were excluded from the consolidated financial statements. As of January 3, 2010, the Trust was

included in the consolidated financial statements. See Note 3 for additional information on the consolidation of the Trust.

Prior to the consolidation of the Trust, the Company’s consolidated balance sheet reflected retained interests

in credit card asset securitizations, which included a transferor’s interest, asset-backed securities, accrued interest

receivable on securitized credit card receivables, cash accounts, servicing rights, the interest-only strip, cash

reserve accounts, and other retained interests. WFB’s retained interests were subject to credit, payment, and

interest rate risks on the transferred credit card receivables. The transferor’s interest was represented by security

certificates and was reported in credit card loans held for sale. WFB’s transferor’s interest ranked pari passu with

investors’ interests in the Trust. The remaining retained interests were subordinate to certain investors’ interests

and, as such, may not have been realized by WFB if needed to absorb deficiencies in cash flows that were allocated

to the investors of the Trust. As contractually required, WFB established certain cash accounts to be used as

collateral for the benefit of investors. There were no amounts in the cash accounts at January 2, 2010, and none

were required. In addition, WFB owned asset-backed securities from some of its securitizations, which may have

been subordinated to other notes issued. WFB maintained responsibility for servicing the securitized loans and

received a servicing fee based on the average outstanding loans in the Trust. Servicing fees were paid monthly and

were reflected in other non-interest income in Financial Services revenue.