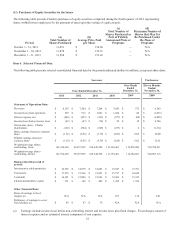

Charter 2013 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2013 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

25

Our cable system franchises are non-exclusive. Accordingly, local and state franchising authorities can grant additional

franchises and create competition in market areas where none existed previously, resulting in overbuilds, which could adversely

affect results of operations.

Our cable system franchises are non-exclusive. Consequently, local and state franchising authorities can grant additional franchises

to competitors in the same geographic area or operate their own cable systems. In some cases, local government entities and

municipal utilities may legally compete with us without obtaining a franchise from the local franchising authority. As a result,

competing operators may build systems in areas in which we hold franchises.

The FCC has adopted rules that streamline entry for new competitors (particularly those affiliated with telephone companies) and

reduce franchising burdens for these new entrants. At the same time, a substantial number of states have adopted new franchising

laws, principally designed to streamline entry for new competitors, and often provide advantages for these new entrants that are

not immediately available to existing operators.

Local franchise authorities have the ability to impose additional regulatory constraints on our business, which could further

increase our expenses.

In addition to the franchise agreement, cable authorities in some jurisdictions have adopted cable regulatory ordinances that further

regulate the operation of cable systems. This additional regulation increases the cost of operating our business. Local franchising

authorities may impose new and more restrictive requirements. Local franchising authorities who are certified to regulate rates

in the communities where they operate generally have the power to reduce rates and order refunds on the rates charged for basic

service and equipment.

Tax legislation and administrative initiatives or challenges to our tax positions could adversely affect our results of operations

and financial condition.

We operate cable systems in locations throughout the United States and, as a result, we are subject to the tax laws and regulations

of federal, state and local governments. From time to time, various legislative and/or administrative initiatives may be proposed

that could adversely affect our tax positions. There can be no assurance that our effective tax rate or tax payments will not be

adversely affected by these initiatives. As a result of state and local budget shortfalls due primarily to the recession as well as other

considerations, certain states and localities have imposed or are considering imposing new or additional taxes or fees on our

services or changing the methodologies or base on which certain fees and taxes are computed. Such potential changes include

additional taxes or fees on our services which could impact our customers, combined reporting and other changes to general

business taxes, central/unit-level assessment of property taxes and other matters that could increase our income, franchise, sales,

use and/or property tax liabilities. In addition, federal, state and local tax laws and regulations are extremely complex and subject

to varying interpretations. There can be no assurance that our tax positions will not be challenged by relevant tax authorities or

that we would be successful in any such challenge.

Further regulation of the cable industry could impair our ability to raise rates to cover our increasing costs, resulting in

increased losses.

Currently, rate regulation of cable systems is strictly limited to the basic service tier and associated equipment and installation

activities. However, the FCC and Congress continue to be concerned that cable rate increases are exceeding inflation. It is possible

that either the FCC or Congress will further restrict the ability of cable system operators to implement rate increases for our video

services or even for our high-speed Internet and voice services. Should this occur, it would impede our ability to raise our rates.

If we are unable to raise our rates in response to increasing costs, our losses would increase.

There has been legislative and regulatory interest in requiring cable operators to offer historically combined programming services

on an á la carte basis. While any new regulation or legislation designed to enable cable operators to purchase programming on

a wholesale basis could be beneficial to Charter, any such new regulation or legislation that limits how we sell programming could

adversely affect our business.

Actions by pole owners might subject us to significantly increased pole attachment costs.

Pole attachments are cable wires that are attached to utility poles. Cable system attachments to investor-owned public utility poles

historically have been regulated at the federal or state level, generally resulting in favorable pole attachment rates for attachments

used to provide cable service. In contrast, utility poles owned by municipalities or cooperatives are not subject to federal regulation

and are generally exempt from state regulation. In 2011, the FCC amended its pole attachment rules to promote broadband

deployment. The order overall strengthens the cable industry's ability to access investor-owned utility poles on reasonable rates,