Charter 2013 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2013 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

57

Due to repayment of variable rate credit facility debt without a LIBOR floor, certain interest rate derivative instruments were de-

designated as cash flow hedges during the three months ended March 31, 2013, as they no longer met the criteria for cash flow

hedging specified by GAAP. In addition, on March 31, 2013, the remaining interest rate derivative instruments that continued to

be highly effective cash flow hedges for GAAP purposes were electively de-designated. On the date of de-designation, we

completed a final measurement test for each interest rate derivative instrument to determine any ineffectiveness and such amount

was reclassified from accumulated other comprehensive loss into gain on derivative instruments, net in our consolidated statements

of operations. For the year ended December 31, 2013, a loss of $27 million related to the reclassification from accumulated other

comprehensive loss into earnings as a result of cash flow hedge discontinuance was recorded in gain on derivative instruments,

net. While these interest rate derivative instruments are no longer designated as cash flow hedges for accounting purposes,

management continues to believe such instruments are closely correlated with the respective debt, thus managing associated risk.

Interest rate derivative instruments not designated as hedges are marked to fair value, with the impact recorded as a gain or loss

on derivative instruments, net in our consolidated statements of operations. For the year ended December 31, 2013, gains of $38

million related to the change in fair value of interest rate derivative instruments not designated as cash flow hedges was recorded

in gain on derivative instruments, net. The balance that remains in accumulated other comprehensive loss for these interest rate

derivative instruments will be amortized over the respective lives of the contracts and recorded as a loss within gain on derivative

instruments, net in our consolidated statements of operations. The net amount of existing losses that are reported in accumulated

other comprehensive loss as of December 31, 2013 that is expected to be reclassified into earnings within the next twelve months

is approximately $19 million.

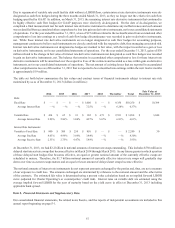

The table set forth below summarizes the fair values and contract terms of financial instruments subject to interest rate risk

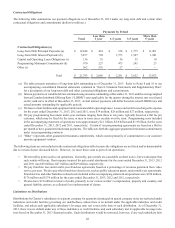

maintained by us as of December 31, 2013 (dollars in millions):

2014 2015 2016 2017 2018 Thereafter Total

Fair Value at

December 31, 2013

Debt:

Fixed Rate $ — $ — $ — $ 1,000 $ — $ 9,350 $10,350 $ 10,384

Average Interest Rate —% —% —% 7.25% —% 6.28% 6.37%

Variable Rate $ 414 $ 65 $ 93 $ 102 $ 673 $ 2,551 $ 3,898 $ 3,848

Average Interest Rate 2.80% 2.86% 3.84% 4.97% 5.67% 6.83% 6.01%

Interest Rate Instruments:

Variable to Fixed Rate $ 800 $ 300 $ 250 $ 850 $ — $ — $ 2,200 $ 30

Average Pay Rate 4.65% 4.99% 3.89% 3.84% —% —% 4.30%

Average Receive Rate 2.55% 2.75% 4.47% 5.48% —% —% 3.93%

At December 31, 2013, we had $2.2 billion in notional amounts of interest rate swaps outstanding. This includes $550 million in

delayed start interest rate swaps that become effective in March 2014 through March 2015. In any future quarter in which a portion

of these delayed start hedges first becomes effective, an equal or greater notional amount of the currently effective swaps are

scheduled to mature. Therefore, the $1.7 billion notional amount of currently effective interest rate swaps will gradually step

down over time as current swaps mature and an equal or lesser amount of delayed start swaps become effective.

The notional amounts of interest rate instruments do not represent amounts exchanged by the parties and, thus, are not a measure

of our exposure to credit loss. The amounts exchanged are determined by reference to the notional amount and the other terms

of the contracts. The estimated fair value is determined using a present value calculation based on an implied forward LIBOR

curve (adjusted for Charter Operating’s or counterparties’ credit risk). Interest rates on variable debt are estimated using the

average implied forward LIBOR for the year of maturity based on the yield curve in effect at December 31, 2013 including

applicable bank spread.

Item 8. Financial Statements and Supplementary Data.

Our consolidated financial statements, the related notes thereto, and the reports of independent accountants are included in this

annual report beginning on page F-1.