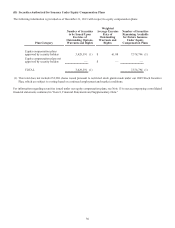

Charter 2013 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2013 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

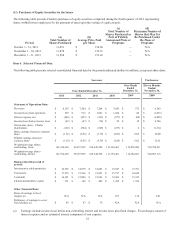

34

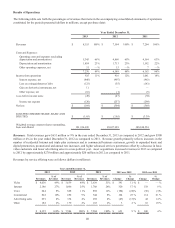

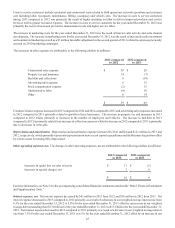

2013, 2012 and 2011, adjusted earnings (loss) before interest expense, income taxes, depreciation and amortization (“Adjusted

EBITDA”) was $2.9 billion, $2.7 billion and $2.7 billion, respectively. See “—Use of Adjusted EBITDA and Free Cash Flow”

for further information on Adjusted EBITDA and free cash flow. Adjusted EBITDA increased 6% for the year ended December

31, 2013 compared to the corresponding period in 2012 as a result of the Bresnan Acquisition, which contributed $90 million, and

an increase in residential and commercial revenues offset by increases in programming costs, costs to service customers and

marketing costs. Costs to service customers primarily increased from higher labor to deliver improved products and service levels

and greater reconnect expense. Adjusted EBITDA remained flat for the year ended December 31, 2012 compared to the

corresponding period in 2011 as a result of an increase in Internet, commercial and advertising revenues offset by higher

programming costs, expenses associated with driving higher growth and investments in the customer experience. For the years

ended December 31, 2013, 2012 and 2011, our income from operations was $925 million, $916 million and $1.0 billion, respectively.

In addition to the factors discussed above, income from operations was affected by increases in depreciation and amortization

primarily due to the Bresnan Acquisition.

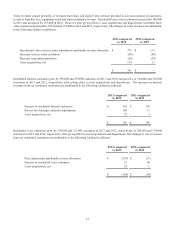

We believe that continued competition and the prolonged recovery of economic conditions in the United States, including mixed

recovery in the housing market and relatively high unemployment levels, have adversely affected consumer demand for our

services, particularly video. Historically, our primary video competitors have often offered more HD channels and have typically

only offered digital services which have a better picture quality compared to our legacy analog product. In response, Charter has

promoted its digital product and initiated a transition from analog to digital transmission of all channels we distribute, which will

result in substantially more HD channels and higher Internet speeds. In the current economic environment, customers have been

more willing to consider our competitors' products, partially because of increased marketing highlighting perceived differences

between competitive video products, especially when those competitors are often offering significant incentives to switch providers.

We also believe some customers have chosen to receive video over the Internet rather than through our OnDemand and premium

video services, thereby reducing our video revenues. We believe competition from wireless service operators and economic factors

have contributed to an increase in the number of homes that replace their traditional telephone service with wireless service thereby

impacting the growth of our telephone business.

If the economic and competitive conditions discussed above do not improve, we believe our business and results of operations

will be adversely affected, which may contribute to future impairments of our franchises and goodwill.

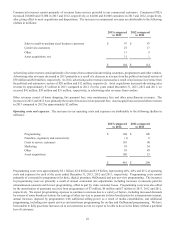

Approximately 89% and 87% of our revenues for years ended December 31, 2013 and 2012, respectively, are attributable to

monthly subscription fees charged to customers for our video, Internet, voice, and commercial services provided by our cable

systems. Generally, these customer subscriptions may be discontinued by the customer at any time subject to a fee for certain

commercial customers and certain residential customers acquired before July 1, 2012. The remaining 11% and 13% of revenue

for fiscal years 2013 and 2012, respectively, is derived primarily from advertising revenues, franchise and other regulatory fee

revenues (which are collected by us but then paid to local authorities), pay-per-view and OnDemand programming, installation,

processing fees or reconnection fees charged to customers to commence or reinstate service, and commissions related to the sale

of merchandise by home shopping services.

Our expenses primarily consist of operating costs, depreciation and amortization expense and interest expense. Operating costs

primarily include programming costs, connectivity, franchise and other regulatory costs, the cost to service our customers such as

field, network and customer operations costs and marketing costs.

We have a history of net losses. Our net losses are principally attributable to insufficient revenue to cover the combination of

operating expenses, interest expenses that we incur because of our debt, depreciation expenses resulting from the capital investments

we have made and continue to make in our cable properties, amortization expenses related to our customer relationship intangibles

and non-cash taxes resulting from increases in our deferred tax liabilities.

Critical Accounting Policies and Estimates

Certain of our accounting policies require our management to make difficult, subjective and/or complex judgments. Management

has discussed these policies with the Audit Committee of Charter’s board of directors, and the Audit Committee has reviewed the

following disclosure. We consider the following policies to be the most critical in understanding the estimates, assumptions and

judgments that are involved in preparing our financial statements, and the uncertainties that could affect our results of operations,

financial condition and cash flows:

• Property, plant and equipment

• Capitalization of labor and overhead costs

• Valuation and impairment of property, plant and equipment