Coca Cola 2007 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2007 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

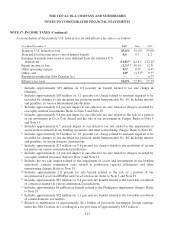

NOTE 17: INCOME TAXES (Continued)

Undistributed earnings of the Company’s foreign subsidiaries amounted to approximately $11.9 billion at

December 31, 2007. Those earnings are considered to be indefinitely reinvested and, accordingly, no U.S. federal and

state income taxes have been provided thereon. Upon distribution of those earnings in the form of dividends or

otherwise, the Company would be subject to both U.S. income taxes (subject to an adjustment for foreign tax credits)

and withholding taxes payable to the various foreign countries. Determination of the amount of unrecognized deferred

U.S. income tax liability is not practical because of the complexities associated with its hypothetical calculation;

however, unrecognized foreign tax credits would be available to reduce a portion of the U.S. tax liability.

As discussed in Note 1, the Jobs Creation Act was enacted in October 2004. One of the provisions provides a

one-time benefit related to foreign tax credits generated by equity investments in prior years. The Company recorded

an income tax benefit of approximately $50 million as a result of this law change in 2004. The Jobs Creation Act also

included a temporary incentive for U.S. multinationals to repatriate foreign earnings at an approximate 5.25 percent

effective tax rate. During the first quarter of 2005, the Company decided to repatriate approximately $2.5 billion in

previously unremitted foreign earnings. Therefore, the Company recorded a provision for taxes on such previously

unremitted foreign earnings of approximately $152 million in the first quarter of 2005. During 2005, the United States

Internal Revenue Service and the United States Department of Treasury issued additional guidance related to the Jobs

Creation Act. As a result of this guidance, the Company reduced the accrued taxes previously provided on such

unremitted earnings by $25 million in the second quarter of 2005. During the fourth quarter of 2005, the Company

repatriated an additional $3.6 billion, with an associated tax liability of approximately $188 million. Therefore, the total

previously unremitted earnings that were repatriated during the full year of 2005 was $6.1 billion with an associated tax

liability of approximately $315 million. This liability was recorded in 2005 as federal and state and local tax expenses

in the amount of $301 million and $14 million, respectively.

115