Coca Cola 2007 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2007 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

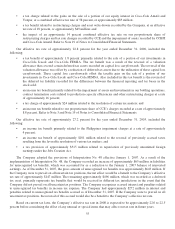

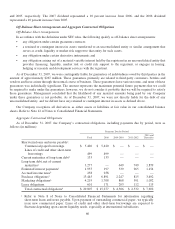

2Refer to Note 9 of Notes to Consolidated Financial Statements for information regarding long-term

debt. We will consider several alternatives to settle this long-term debt, including the use of cash

flows from operating activities, issuance of commercial paper or issuance of other long-term debt.

3We calculated estimated interest payments for long-term debt as follows: for fixed-rate debt, we

calculated interest based on the applicable rates and payment dates; for variable-rate debt, we

estimated interest rates and payment dates based on our determination of the most likely scenarios

for each relevant debt instrument. We typically expect to settle such interest payments with cash

flows from operating activities and/or short-term borrowings.

4Refer to Note 17 of Notes to Consolidated Financial Statements for information regarding income

taxes. As of December 31, 2007, the noncurrent portion of our income tax liability, including

accrued interest and penalties related to unrecognized tax benefits, was approximately

$883 million, which was not included in the total above. At this time, the settlement period for the

noncurrent portion of our income tax liability cannot be determined. In addition, any payments

related to unrecognized tax benefits would be partially offset by reductions in payments in other

jurisdictions.

5The purchase obligations include agreements to purchase goods or services that are enforceable

and legally binding and that specify all significant terms, including long-term contractual

obligations, open purchase orders, accounts payable and certain accrued liabilities. We expect to

fund these obligations with cash flows from operating activities.

6We expect to fund these marketing obligations with cash flows from operating activities.

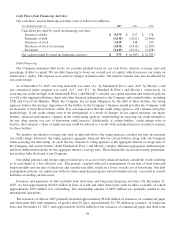

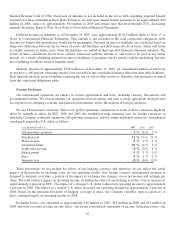

In accordance with SFAS No. 87, “Employers’ Accounting for Pensions,” and SFAS No. 106, “Employers’

Accounting for Postretirement Benefits Other Than Pensions,” as amended by SFAS No. 158, “Employers’ Accounting

for Defined Benefit Pension and Other Postretirement Plans—an amendment of FASB Statements No. 87, 88, 106, and

132(R),” the total accrued benefit liability for pension and other postretirement benefit plans recognized as of

December 31, 2007 was $873 million. Refer to Note 16 of Notes to Consolidated Financial Statements. This amount is

impacted by, among other items, pension expense, funding levels, plan amendments, changes in plan demographics and

assumptions, investment return on plan assets, and the application of SFAS No. 158. Because the accrued liability does

not represent expected liquidity needs, we did not include this amount in the contractual obligations table.

The Pension Protection Act of 2006 (“PPA”) was enacted in August 2006 and established, among other things,

new standards for funding of U.S. defined benefit pension plans. One of the primary objectives of the PPA is to

improve the financial integrity of underfunded plans through the requirement of additional contributions. The

requirements of the PPA will not have a significant impact on our financial condition because, under the provisions of

the PPA, required contributions for the primary funded U.S. plan are projected to be zero through 2017 as a result of

contributions we have made to the plan since 2001. Therefore, we did not include any amounts as a contractual

obligation in the above table. We may, however, decide to make additional discretionary contributions to our pension

and other benefit plans in future years. In addition, as a result of contributions totaling approximately $224 million in

2006 to fund a portion of our U.S. postretirement healthcare obligation, including a contribution of $216 million to a

VEBA trust, we do not expect to contribute to our U.S. postretirement healthcare plan in 2008. We generally expect to

fund all future contributions with cash flows from operating activities.

Our international pension plans are funded in accordance with local laws and income tax regulations. We do not

expect contributions to these plans to be material in 2008 or thereafter. Therefore, no amounts have been included in

the table above.

As of December 31, 2007, the projected benefit obligation of the U.S. qualified pension plans was $1,725 million,

and the fair value of plan assets was approximately $2,255 million. As of December 31, 2007, the projected benefit

obligation of all pension plans other than the U.S. qualified pension plans was approximately $1,792 million, and the

fair value of all other pension plan assets was approximately $1,173 million. The majority of this underfunding is

attributable to an international pension plan for certain non-U.S. employees that is unfunded due to tax law restrictions,

as well as our unfunded U.S. nonqualified pension plans. These U.S. nonqualified pension plans provide, for certain

associates, benefits that are not permitted to be funded through a qualified plan because of limits imposed by the

61