Coca Cola 2007 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2007 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

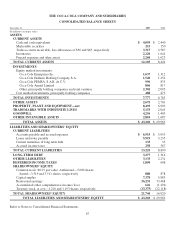

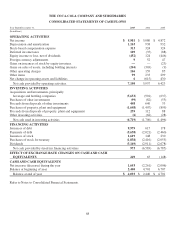

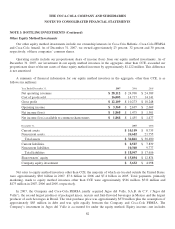

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1: BUSINESS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

No. 160 also establishes disclosure requirements that clearly identify and distinguish between the controlling and

noncontrolling interests and requires the separate disclosure of income attributable to controlling and noncontrolling

interests. SFAS No. 160 is effective for fiscal years beginning after December 15, 2008. The Company is currently

evaluating the impact that the adoption of SFAS No. 160 will have on our consolidated financial statements.

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial

Liabilities—Including an amendment of FASB Statement No. 115.” SFAS No. 159 permits entities to choose to

measure many financial instruments and certain other items at fair value. Unrealized gains and losses on items for

which the fair value option has been elected will be recognized in earnings at each subsequent reporting date. SFAS

No. 159 was effective for our Company on January 1, 2008. The adoption of SFAS No. 159 did not have a material

impact on our consolidated financial statements.

In September 2006, the SEC staff published SAB No. 108, “Considering the Effects of Prior Year Misstatements

when Quantifying Misstatements in Current Year Financial Statements.” SAB No. 108 addresses quantifying the

financial statement effects of misstatements, specifically, how the effects of prior year uncorrected errors must be

considered in quantifying misstatements in the current year financial statements. SAB No. 108 was effective for fiscal

years ending after November 15, 2006. The adoption of SAB No. 108 by our Company in the fourth quarter of 2006

did not have a material impact on our consolidated financial statements.

As previously discussed, our Company adopted SFAS No. 158 related to defined benefit pension and other

postretirement plans. Refer to Note 16.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements.” SFAS No. 157 defines fair

value, establishes a framework for measuring fair value and expands disclosure requirements about fair value

measurements. SFAS No. 157 was effective for our Company on January 1, 2008. However, in February 2008, the

FASB released a FASB Staff Position (FSP FAS 157-2—Effective Date of FASB Statement No. 157 ) which delayed

the effective date of SFAS No. 157 for all nonfinancial assets and nonfinancial liabilities, except those that are

recognized or disclosed at fair value in the financial statements on a recurring basis (at least annually). The adoption of

SFAS No. 157 for our financial assets and liabilities did not have a material impact upon adoption. We do not believe

the adoption of SFAS No. 157 for our non-financial assets and liabilities, effective January 1, 2009, will have a

material impact on our consolidated financial statements.

In July 2006, the FASB issued Interpretation No. 48 which clarifies the accounting for uncertainty in income taxes

recognized in an enterprise’s financial statements in accordance with SFAS No. 109, “Accounting for Income Taxes.”

Interpretation No. 48 prescribes a recognition threshold and measurement attribute for the financial statement

recognition and measurement of a tax position taken or expected to be taken in a tax return. Interpretation No. 48 also

provides guidance on derecognition, classification, interest and penalties, accounting in interim periods, disclosure and

transition. For our Company, Interpretation No. 48 was effective January 1, 2007. As a result of the adoption of

Interpretation No. 48, we recorded an approximate $65 million increase in accrued income taxes in our consolidated

balance sheet for unrecognized tax benefits, which was accounted for as a cumulative effect adjustment to the

January 1, 2007 balance of reinvested earnings. Refer to Note 17.

In May 2005, the FASB issued SFAS No. 154, “Accounting Changes and Error Corrections, a replacement of

Accounting Principles Board (“APB”) Opinion No. 20 and FASB Statement No. 3.” SFAS No. 154 requires

retrospective application to prior periods’ financial statements of a voluntary change in accounting principle unless it is

impracticable. APB Opinion No. 20, “Accounting Changes,” previously required that most voluntary changes in

77