Coca Cola 2007 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2007 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

THE COCA-COLA COMPANY AND SUBSIDIARIES

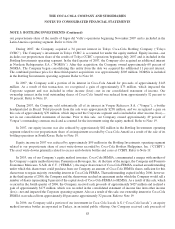

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1: BUSINESS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

fair value in our consolidated balance sheets, with fair values of foreign currency derivatives estimated based on quoted

market prices or pricing models using current market rates. Cash flows from derivative instruments designated as net

investment hedges are classified as investing activities. Cash flows from other derivative instruments used to manage

interest, commodity or currency exposures are classified as operating activities. Refer to Note 12.

Retirement-Related Benefits

Using appropriate actuarial methods and assumptions, our Company accounts for defined benefit pension plans in

accordance with SFAS No. 87, “Employers’ Accounting for Pensions,” and we account for our nonpension

postretirement benefits in accordance with SFAS No. 106, “Employers’ Accounting for Postretirement Benefits Other

Than Pensions,” as amended by SFAS No. 158, “Employers’ Accounting for Defined Benefit Pension and Other

Postretirement Plans—an amendment of FASB Statements No. 87, 88, 106, and 132(R).” Effective December 31, 2006

for our Company, SFAS No. 158 required that previously unrecognized actuarial gains or losses, prior service costs or

credits and transition obligations or assets be recognized generally through adjustments to accumulated other

comprehensive income and credits to prepaid benefit cost or accrued benefit liability. As a result of these adjustments,

the current funded status of defined benefit pension plans and other postretirement benefit plans is reflected in the

Company’s consolidated balance sheets as of December 31, 2007 and 2006. Refer to Note 16.

Our equity method investees also adopted SFAS No. 158 effective December 31, 2006. Refer to Note 3 for the

impact on our consolidated balance sheet resulting from the adoption of SFAS No. 158 by our equity method investees.

Contingencies

Our Company is involved in various legal proceedings and tax matters. Due to their nature, such legal proceedings

and tax matters involve inherent uncertainties including, but not limited to, court rulings, negotiations between affected

parties and governmental actions. Management assesses the probability of loss for such contingencies and accrues a

liability and/or discloses the relevant circumstances, as appropriate. Refer to Note 13.

Business Combinations

In accordance with SFAS No. 141, “Business Combinations,” we account for all business combinations by the

purchase method. Furthermore, we recognize intangible assets apart from goodwill if they arise from contractual or

legal rights or if they are separable from goodwill.

Recent Accounting Standards and Pronouncements

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations.” SFAS No. 141(R)

amends the principles and requirements for how an acquirer recognizes and measures in its financial statements the

identifiable assets acquired, the liabilities assumed, any noncontrolling interest in the acquiree and the goodwill

acquired. SFAS No. 141(R) also establishes disclosure requirements to enable the evaluation of the nature and financial

effects of the business combination. SFAS No. 141(R) is effective for our Company on January 1, 2009, and the

Company will apply prospectively to all business combinations subsequent to the effective date.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial

Statements—an amendment of Accounting Research Bulletin No. 51.” SFAS No. 160 establishes accounting and

reporting standards for the noncontrolling interest in a subsidiary and for the deconsolidation of a subsidiary. SFAS

76