Coca Cola 2007 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2007 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

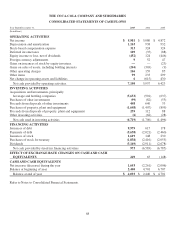

|

|

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1: BUSINESS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

accounting principle be recognized by including in net income of the period of the change the cumulative effect of

changing to the new accounting principle. SFAS No. 154 became effective for our Company on January 1, 2006. The

adoption of SFAS No. 154 did not have a material impact on our consolidated financial statements.

In December 2004, the FASB issued SFAS No. 153, “Exchanges of Nonmonetary Assets, an amendment of APB

Opinion No. 29.” SFAS No. 153 is based on the principle that exchanges of nonmonetary assets should be measured

based on the fair value of the assets exchanged. APB Opinion No. 29, “Accounting for Nonmonetary Transactions,”

provided an exception to its basic measurement principle (fair value) for exchanges of similar productive assets. Under

APB Opinion No. 29, an exchange of a productive asset for a similar productive asset was based on the recorded

amount of the asset relinquished. SFAS No. 153 eliminates this exception and replaces it with an exception for

exchanges of nonmonetary assets that do not have commercial substance. SFAS No. 153 became effective for our

Company as of July 2, 2005, and did not have a material impact on our consolidated financial statements.

As previously discussed, our Company adopted SFAS No. 123(R) related to share based payments effective

January 1, 2006. Refer to Note 15.

In November 2004, the FASB issued SFAS No. 151, “Inventory Costs, an amendment of Accounting Research

Bulletin No. 43, Chapter 4.” SFAS No. 151 requires that abnormal amounts of idle facility expense, freight, handling

costs and wasted materials (spoilage) be recorded as current period charges and that the allocation of fixed production

overheads to inventory be based on the normal capacity of the production facilities. The Company adopted SFAS

No. 151 on January 1, 2006. The adoption of SFAS No. 151 did not have a material impact on our consolidated

financial statements.

In October 2004, the American Jobs Creation Act of 2004 (the “Jobs Creation Act”) was signed into law. The Jobs

Creation Act included a temporary incentive for U.S. multinationals to repatriate foreign earnings at an approximate

5.25 percent effective tax rate. Issued in December 2004, FASB Staff Position 109-2, “Accounting and Disclosure

Guidance for the Foreign Earnings Repatriation Provision within the American Jobs Creation Act of 2004” indicated

that the lack of clarification of certain provisions within the Jobs Creation Act and the timing of the enactment

necessitated a practical exception to the SFAS No. 109, “Accounting for Income Taxes,” requirement to reflect in the

period of enactment the effect of a new tax law. Accordingly, enterprises were allowed time beyond 2004 to evaluate

the effect of the Jobs Creation Act on their plans for reinvestment or repatriation of foreign earnings for purposes of

applying SFAS No. 109. Accordingly, in 2005, the Company repatriated $6.1 billion of its previously unremitted

earnings and recorded an associated tax expense of approximately $315 million. Refer to Note 17.

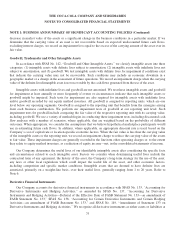

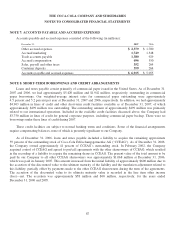

NOTE 2: INVENTORIES

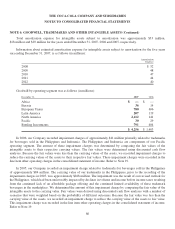

Inventories consisted of the following (in millions):

December 31, 2007 2006

Raw materials and packaging $ 1,199 $ 923

Finished goods 789 548

Other 232 170

Inventories $ 2,220 $ 1,641

78