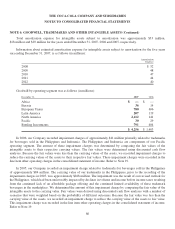

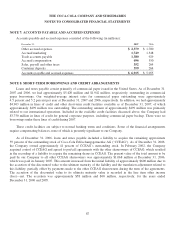

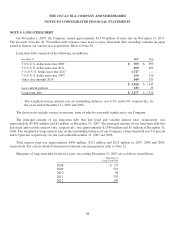

Coca Cola 2007 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2007 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

THE COCA-COLA COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 13: COMMITMENTS AND CONTINGENCIES (Continued)

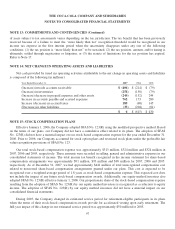

During the period from 1970 to 1981, our Company owned Aqua-Chem, Inc., now known as Cleaver-Brooks, Inc.

(“Aqua-Chem”). A division of Aqua-Chem manufactured certain boilers that contained gaskets that Aqua-Chem

purchased from outside suppliers. Several years after our Company sold this entity, Aqua-Chem received its first

lawsuit relating to asbestos, a component of some of the gaskets. In September 2002, Aqua-Chem notified our

Company that it believed we were obligated for certain costs and expenses associated with its asbestos litigations.

Aqua-Chem demanded that our Company reimburse it for approximately $10 million for out-of-pocket

litigation-related expenses. Aqua-Chem also demanded that the Company acknowledge a continuing obligation to

Aqua-Chem for any future liabilities and expenses that are excluded from coverage under the applicable insurance or

for which there is no insurance. Our Company disputes Aqua-Chem’s claims, and we believe we have no obligation to

Aqua-Chem for any of its past, present or future liabilities, costs or expenses. Furthermore, we believe we have

substantial legal and factual defenses to Aqua-Chem’s claims. The parties entered into litigation in Georgia to resolve

this dispute, which was stayed by agreement of the parties pending the outcome of litigation filed in Wisconsin by

certain insurers of Aqua-Chem. In that case, five plaintiff insurance companies filed a declaratory judgment action

against Aqua-Chem, the Company and 16 defendant insurance companies seeking a determination of the parties’ rights

and liabilities under policies issued by the insurers and reimbursement for amounts paid by plaintiffs in excess of their

obligations. During the course of the Wisconsin coverage litigation, Aqua-Chem and the Company reached settlements

with several of the insurers, including plaintiffs, who have or will pay funds into an escrow account for payment of

costs arising from the asbestos claims against Aqua-Chem. On July 24, 2007, the Wisconsin trial court entered a final

declaratory judgment regarding the rights and obligations of the parties under the insurance policies issued by the

remaining defendant insurers, which judgment was not appealed. The judgment directs, among other things, that each

insurer whose policy is triggered is jointly and severally liable for one-hundred percent of Aqua-Chem’s losses up to

policy limits. The Georgia litigation remains subject to the stay agreement.

The Company has had discussions with the Competition Directorate of the European Commission (the “European

Commission”) about issues relating to parallel trade within the European Union arising out of comments received by

the European Commission from third parties. The Company has fully cooperated with the European Commission and

has provided information on these issues and the measures taken and to be taken to address them. The Company is

unable to predict at this time with any reasonable degree of certainty what action, if any, the European Commission

will take with respect to these issues.

At the time we acquire or divest our interest in an entity, we sometimes agree to indemnify the seller or buyer for

specific contingent liabilities. Management believes that any liability to the Company that may arise as a result of any

such indemnification agreements will not have a material adverse effect on the financial condition of the Company

taken as a whole.

The Company is involved in various tax matters, with respect to some of which the outcome is uncertain. We

establish reserves to remove some or all of the tax benefit of any of our tax positions at the time we determine that it

becomes uncertain based upon one of the following conditions: (1) the tax position is not “more likely than not” to be

sustained, (2) the tax position is “more likely than not” to be sustained, but for a lesser amount, or (3) the tax position is

“more likely than not” to be sustained, but not in the financial period in which the tax position was originally taken. For

purposes of evaluating whether or not a tax position is uncertain, (1) we presume the tax position will be examined by

the relevant taxing authority that has full knowledge of all relevant information, (2) the technical merits of a tax

position are derived from authorities such as legislation and statutes, legislative intent, regulations, rulings and case law

and their applicability to the facts and circumstances of the tax position, and (3) each tax position is evaluated without

consideration of the possibility of offset or aggregation with other tax positions taken. A number of years may elapse

before a particular uncertain tax position is audited and finally resolved or when a tax assessment is raised. The number

96