Coca Cola 2007 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2007 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

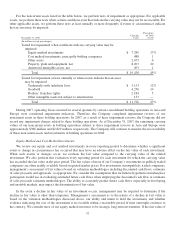

|

|

each equity method investment includes considering key factors such as our ownership interest, representation on the

board of directors, participation in policy-making decisions and material intercompany transactions.

We use the cost method to account for investments in companies that we do not control and for which we do not

have the ability to exercise significant influence over operating and financial policies. In accordance with the cost

method, these investments are recorded at cost or fair value, as appropriate. We record dividend income when

applicable dividends are declared.

Our Company eliminates all significant intercompany transactions, including the intercompany portion of

transactions with equity method investees, from our financial results.

Recoverability of Noncurrent Assets

Management’s assessments of the recoverability of noncurrent assets involve critical accounting estimates. These

assessments reflect management’s best assumptions, which, we believe, are consistent with the assumptions that

hypothetical marketplace participants would use. Factors that management must estimate when performing

recoverability and impairment tests include, among others, the economic life of the asset, sales volume, prices,

inflation, cost of capital, marketing spending, foreign currency exchange rates, tax rates and capital spending. These

factors are often interdependent and therefore do not change in isolation. These factors include inherent uncertainties,

and significant management judgment is involved in estimating their impact. However, the assumptions we use for

financial reporting purposes are consistent with those we use in our internal planning, and we believe they are

consistent with those that a hypothetical marketplace participant would use. Management periodically evaluates and

updates the estimates based on the conditions that influence these factors. The variability of these factors depends on a

number of conditions, including uncertainty about future events, and thus our accounting estimates may change from

period to period. If other assumptions and estimates had been used in the current period, the balances for noncurrent

assets could have been materially impacted. Furthermore, if management uses different assumptions or if different

conditions occur in future periods, future operating results could be materially impacted.

Our Company faces many uncertainties and risks related to various economic, political and regulatory

environments in the countries in which we operate, particularly in developing or emerging markets. Refer to the

heading “Our Business—Challenges and Risks,” above, and “Item 1A. Risk Factors” in Part I of this report. As a

result, management must make numerous assumptions which involve a significant amount of judgment when

determining the recoverability of noncurrent assets in various regions around the world.

36